Goldman Sachs Slaps Sell on Super Micro: AI Server King's Margins Crumble to 9%

January 13, 2026 · by Fintool Agent

Super Micro Computer dropped 5% on Tuesday after Goldman Sachs initiated coverage with a Sell rating and a $26 price target—the first major Wall Street firm to turn explicitly bearish on the AI server maker since it narrowly avoided delisting last year.

The call lands at a critical inflection point. Analyst Katherine Murphy's 49-page note doesn't dispute Super Micro's role in the AI buildout—it argues the company is winning orders at the cost of its profitability, with gross margins collapsing to levels not seen since before the generative AI boom began.

The Margin Problem Is Getting Worse

The numbers tell a stark story. Super Micro's gross margin in Q1 2026 fell to 9.3%, down from 15.5% just eighteen months earlier. Operating margins have compressed even more dramatically—from 10.1% in Q2 2024 to just 3.6% in the most recent quarter.

| Metric | Q2 2024 | Q3 2024 | Q4 2024 | Q1 2025 | Q2 2025 | Q3 2025 | Q4 2025 | Q1 2026 |

|---|---|---|---|---|---|---|---|---|

| Gross Margin % | 15.4% | 15.5% | 10.2%* | 13.1%* | 11.8% | 9.6%* | 9.5%* | 9.3%* |

| Operating Margin % | 10.1%* | 9.8%* | 5.4%* | 8.6%* | 6.5%* | 3.2%* | 4.0%* | 3.6%* |

| Revenue ($B) | $3.7 | $3.9 | $5.4* | $5.9* | $5.7 | $4.6 | $5.8 | $5.0 |

*Values retrieved from S&P Global

Management has explicitly acknowledged the trade-off. On the Q3 2025 earnings call, CFO David Weigand attributed the margin compression to "our strategy to offer competitive pricing to gain market share, change in product and customer mix, and higher manufacturing related expenses."

The Dell Price War

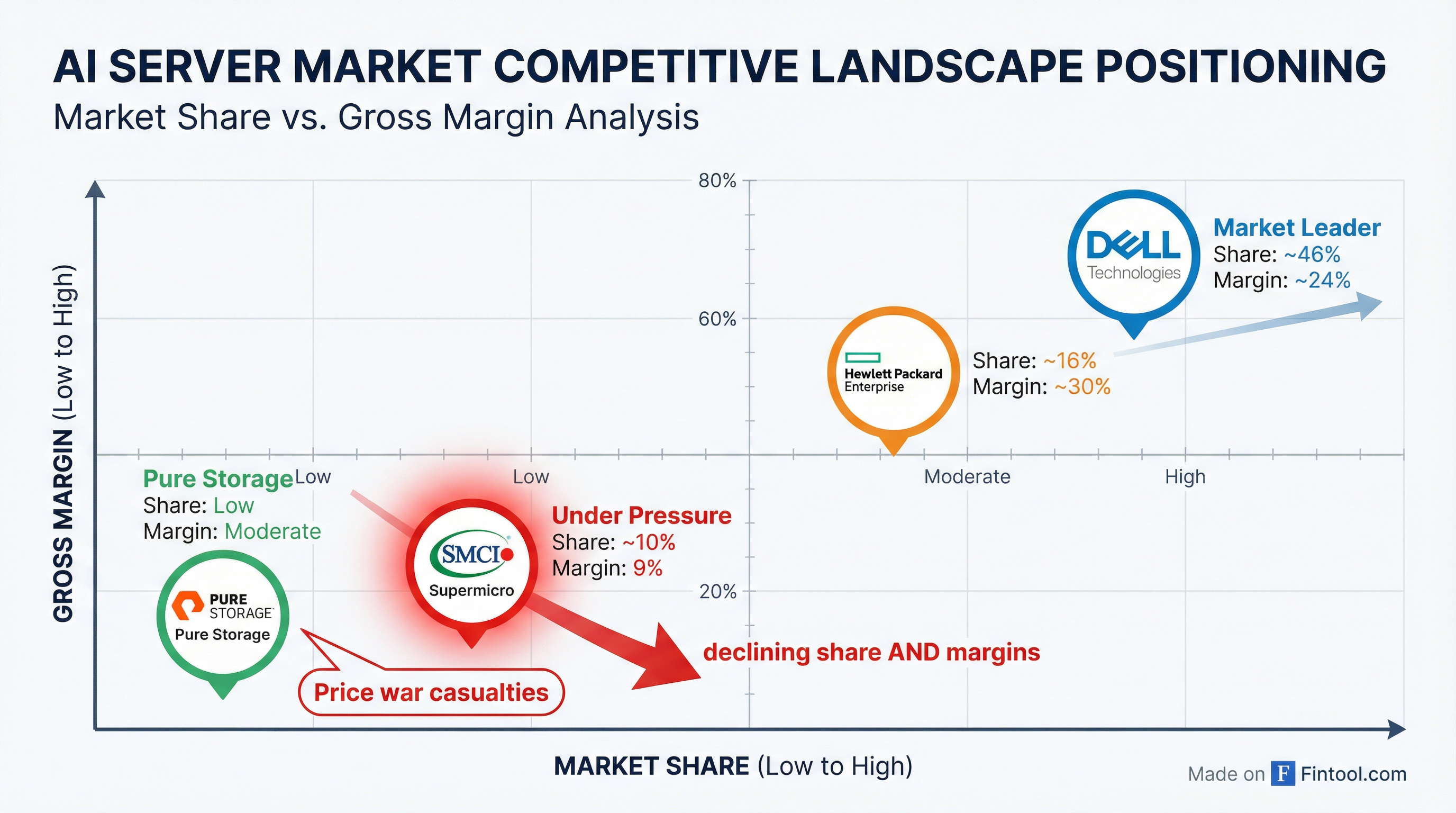

Goldman's bearish thesis centers on one uncomfortable truth: Dell Technologies has the balance sheet to win a price war, and it's using it.

Dell commands roughly 46% of the broader server hardware market versus Super Micro's 10%, and it has weaponized that scale advantage in AI infrastructure. As one analyst noted, Dell "has used its deep pockets to undercut prices" while maintaining margins in the low-20% range—more than double Super Micro's current levels.

Super Micro's market share in AI servers has plummeted from approximately 80% in 2022 to between 40-50% by late 2024, with the erosion continuing into 2025 and 2026.

The company's 10-K filing acknowledges this reality directly: "Both legacy competitors as well as new entrants, predominantly Asia-based competitors, have intensified market competition in recent years leading to pricing pressure."

Concentration Risks Stack Up

Goldman's note highlights two structural vulnerabilities that compound the margin problem:

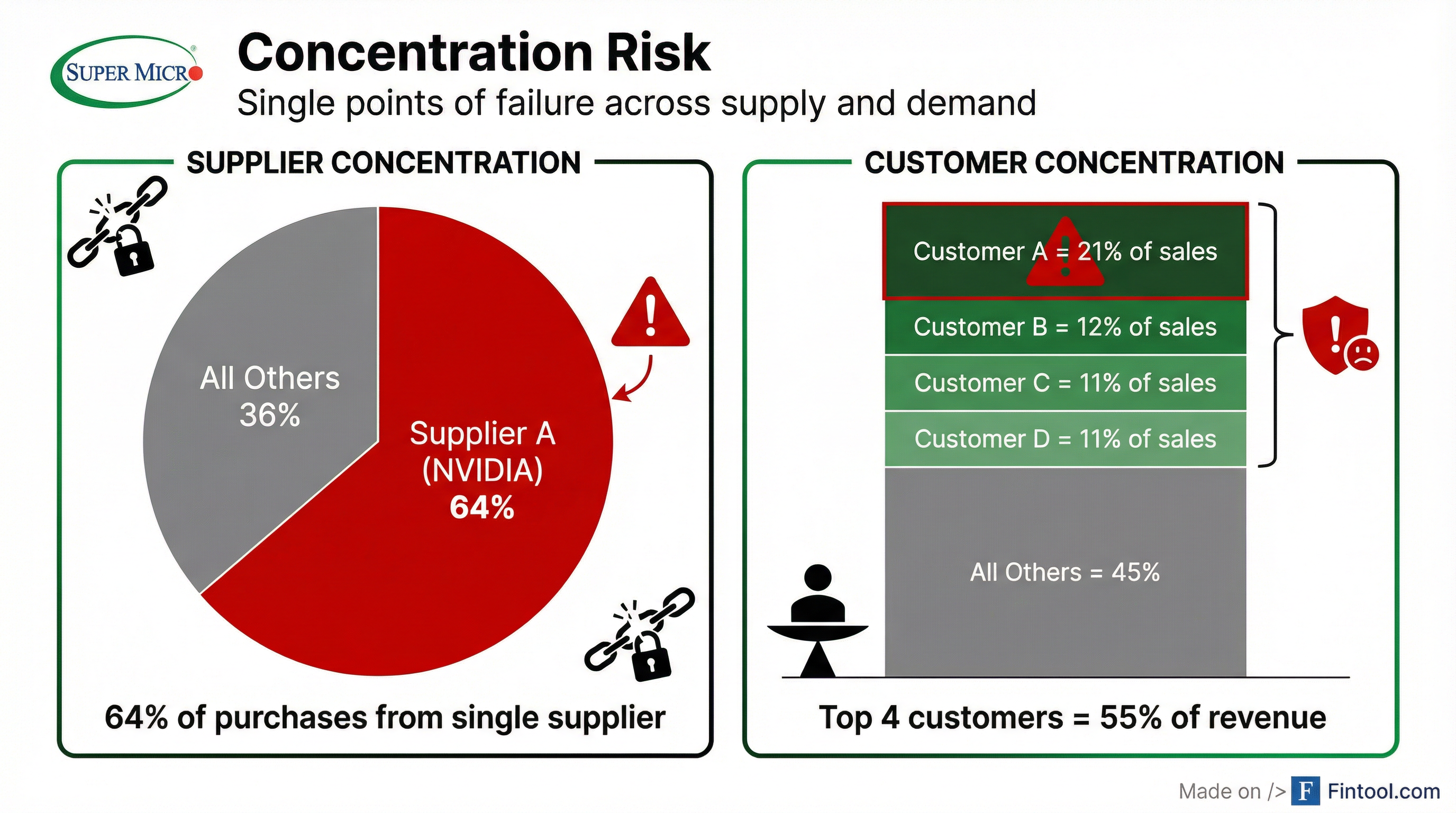

Supplier Concentration: One supplier—almost certainly NVIDIA—accounted for 64.4% of Super Micro's total purchases in fiscal 2025, up from 30.7% just two years earlier. This dependency limits Super Micro's negotiating power and exposes it to supply chain disruptions.

Customer Concentration: Four customers now represent 55% of total revenue. The 10-K explicitly warns that large orders "are generally subject to intense competition and pricing pressure which can have an adverse impact on our margins and results of operations."

The Bull Case: Volume Over Margins

Super Micro isn't playing defense—it's executing a deliberate strategy to trade profitability for market position. The company expects Q2 fiscal 2026 revenue to nearly double to $10-11 billion, suggesting massive backlog conversion.

CEO Charles Liang frames this as a land grab: "We gain more and more order for Blackwell and expect strong growth starting from now." The logic is that once Super Micro's liquid-cooled racks are installed in data centers, switching costs make those relationships sticky.

The company maintains real competitive advantages:

- Speed to market: Super Micro typically ships new NVIDIA platforms in 3-6 months versus 6-12 months for traditional OEMs

- Liquid cooling leadership: DLC-2 technology claims 40% power savings versus air-cooled systems

- Modular architecture: Building Block Solutions enable faster customization cycles

But Goldman's Murphy questions whether these advantages justify giving up 600+ basis points of gross margin. The firm flagged that software represents less than 2% of revenue, limiting SMCI's ability to layer higher-margin services on top of hardware sales.

What to Watch

The stock closed at $28.60 on volume of 52 million shares—nearly double the average—with 15% short interest suggesting significant bearish positioning remains.

| Metric | Value |

|---|---|

| Stock Price | $28.60 |

| Goldman Target | $26.00 (-9%) |

| 52-Week Range | $25.71 - $66.44 |

| Market Cap | $17.0B |

| Forward P/E | 15x |

| Short Interest | 15% |

Three catalysts will determine whether Goldman's call proves prescient:

- Q2 results (expected late January): Can management deliver on the $10-11B revenue guide without margins compressing further?

- Blackwell ramp: Higher volumes on NVIDIA's newest platform could improve mix, but so far new generations have coincided with deeper discounting

- Dell's counter-move: If Dell accelerates its AI server push, Super Micro's "volume over margin" strategy becomes a race to the bottom

The governance cloud that nearly killed the stock in 2024-2025 has lifted—Super Micro filed its delayed 10-K and retained new auditor BDO. But Goldman's initiation suggests a new overhang has taken its place: the question of whether Super Micro can be an AI winner and a profitable company at the same time.

Related: Super Micro Computer · Dell Technologies · Nvidia · Hewlett Packard Enterprise