Keysight's Record Q1: AI Data Center Demand Powers 23% Revenue Surge, Stock Jumps 15%

February 23, 2026 · by Fintool Agent

Keysight Technologies delivered a blowout quarter that underscores why the company has become one of the clearest "picks and shovels" plays on the AI infrastructure buildout. Record revenue of $1.60 billion crushed estimates by $60 million, orders surged 30% year-over-year, and management raised its full-year outlook to above 20% growth—a remarkable acceleration for a company with a long-term target of 5-7%.

The stock responded accordingly: KEYS jumped approximately 15% in after-hours trading to $281.25, adding roughly $6 billion in market capitalization.

The Numbers

| Metric | Q1 2026 | Q1 2025 | YoY Change |

|---|---|---|---|

| Revenue | $1.60B | $1.30B | +23% |

| Orders | $1.645B | $1.27B | +30% |

| GAAP Net Income | $281M | $169M | +66% |

| GAAP EPS | $1.63 | $0.97 | +68% |

| Non-GAAP EPS | $2.17 | $1.82 | +19% |

| Gross Margin | 66.7% | 65.8% | +90 bps |

| Operating Margin | 27.4% | 27.2% | +20 bps |

| Free Cash Flow | $407M | $346M | +18% |

Both revenue ($1.60B vs. $1.54B expected) and EPS ($2.17 vs. $2.00) significantly exceeded Wall Street estimates.

Why This Matters: The AI Infrastructure Picks-and-Shovels Play

Keysight's results illuminate a critical but often overlooked dimension of the AI buildout: before hyperscalers can deploy AI clusters, someone has to test the chips, transceivers, switches, and interconnects that make them work. That someone is increasingly Keysight.

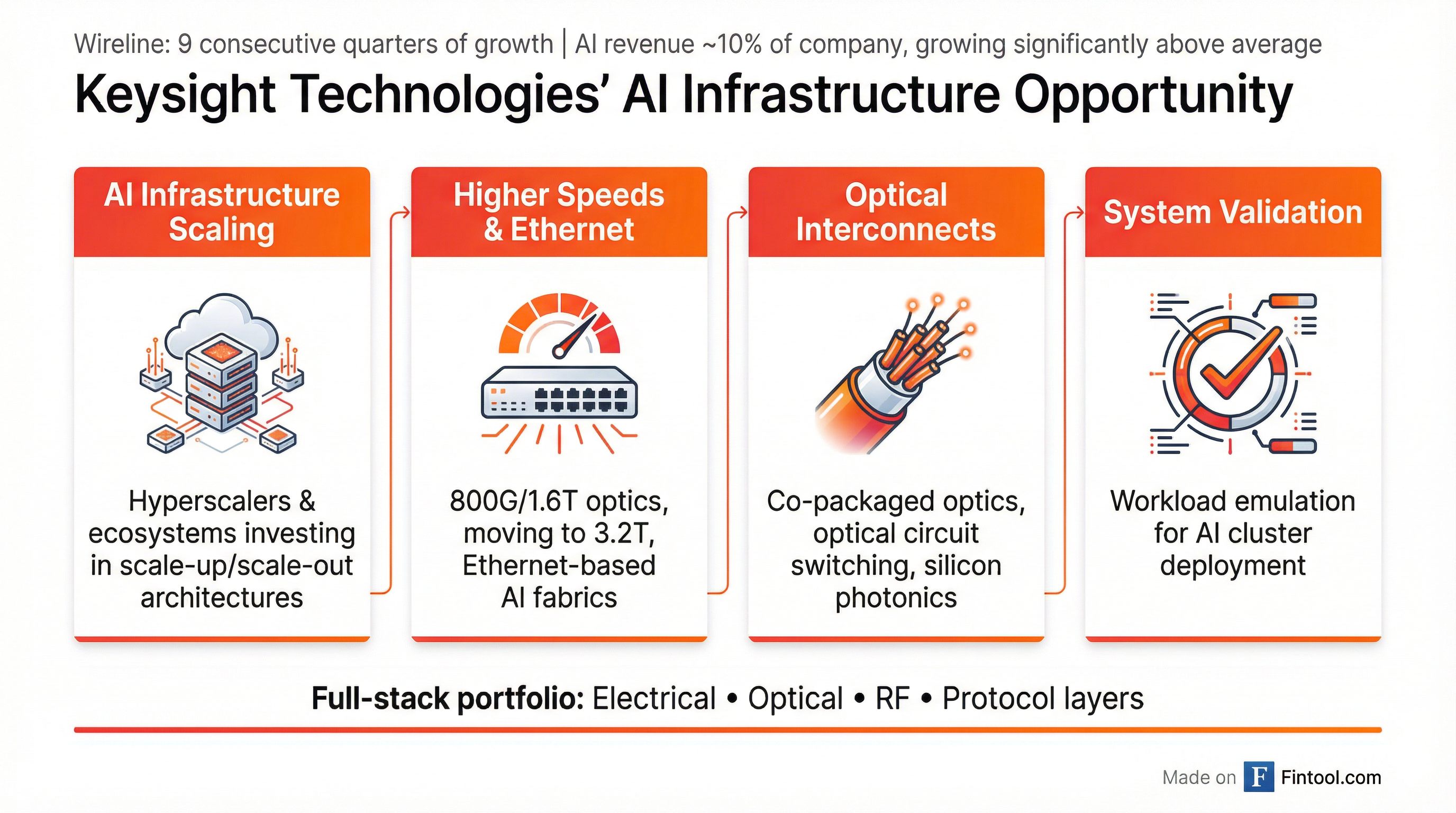

CEO Satish Dhanasekaran laid out four structural drivers powering the company's wireline business—which surpassed wireless revenue for the first time:

1. AI Infrastructure Scaling: Hyperscalers and their ecosystems are investing heavily in scale-up and scale-out architectures. Keysight's full-stack portfolio—spanning electrical, optical, RF, and protocol technologies—enables end-to-end validation from early design through deployment.

2. Higher Speeds and Ethernet-Based Networking: AI workloads are driving rapid data center buildouts with 800G and 1.6T optics, alongside accelerated development of 3.2T. The move to Ethernet-based AI fabrics creates more test opportunities.

3. Optical Interconnects: Rising bandwidth and power demands are accelerating adoption of optical interconnects. Keysight is assisting module suppliers with 800G and 1.6T development, while customers design around co-packaged optics and silicon photonics.

4. System-Level Validation: As AI clusters scale, Keysight's workload emulation solutions help customers solve deployment challenges by emulating real AI stress conditions before going live.

"AI infrastructure is rapidly scaling. Hyperscalers and their respective ecosystems are investing in designing and deploying scale-up and scale-out architectures. As these systems grow larger and more complex, there is an increasing need to validate performance across the entire infrastructure stack," Dhanasekaran said.

Segment Performance

Communications Solutions Group (CSG): Revenue of $1.124 billion, up 27% YoY

- Commercial Communications: $758 million, +33% YoY

- Aerospace, Defense & Government: $366 million, +18% YoY (record Q1 orders)

Electronic Industrial Solutions Group (EISG): Revenue of $476 million, up 15% YoY

- Double-digit growth across general electronics, semiconductors, and automotive

- High-bandwidth memory and AI-driven capacity expansion drove wafer-level test demand

The defense business benefited from "heightened global focus on deterrence and defense modernization priorities," with particularly strong activity in Europe as governments boost spending amid elevated security concerns.

Guidance: Acceleration Continues

The outlook was arguably even more impressive than the quarter itself:

| Metric | Q2 2026 Guidance | YoY Growth |

|---|---|---|

| Revenue | $1.69B - $1.71B | 30% |

| Non-GAAP EPS | $2.27 - $2.33 | 35% |

Management raised its full-year outlook: "With the visibility we currently have, our base case for fiscal 2026 has increased, as we now expect total annual revenue and earnings growth just above 20%."

This represents a significant upgrade from the company's prior long-term model of 5-7% growth. CFO Neil Dougherty noted the guidance excludes potential impacts from the recent Supreme Court tariff ruling, which the company is still assessing.

The AI Exposure Story

A key question for investors: how much AI exposure does Keysight actually have?

Management provided color on the call:

- AI-related revenue is approximately 10% of company revenue

- AI order growth was "significantly above company average" (which was 30%)

- Customer count has doubled in the AI segment

- Top 2 customers are still non-AI, reflecting "broadening of demand"

"The name of the game is really about broadening of demand across our customer base," Dhanasekaran explained. "We've doubled the number of customers that are present at that demand."

SVP of Global Sales Steve Yoon added context on the pipeline: "In my 36 years with the company, this is one of the strongest funnels I've ever seen across the four dimensions that I track—short-term funnel, long-term funnel, funnel intake, and funnel velocity. Both our total funnel and new funnel intake are at all-time highs."

Historical Context: Revenue Trajectory

| Quarter | Revenue | YoY Change |

|---|---|---|

| Q2 2024 | $1.216B | — |

| Q3 2024 | $1.217B | — |

| Q4 2024 | $1.287B | — |

| Q1 2025 | $1.298B | — |

| Q2 2025 | $1.306B | +7.4% |

| Q3 2025 | $1.352B | +11.1% |

| Q4 2025 | $1.419B | +10.3% |

| Q1 2026 | $1.600B | +23.3% |

The acceleration is unmistakable: after hovering near $1.2-1.3 billion for much of FY24, Keysight has seen growth compound as AI infrastructure spending intensified.

Balance Sheet and Capital Allocation

Keysight ended Q1 with $2.2 billion in cash and generated $441 million in operating cash flow. The company repurchased approximately 420,000 shares at an average price of $207 for $87 million.

The board has authorized a $1.5 billion stock buyback program. Management's priorities remain organic investment first, followed by M&A and shareholder returns. Three recent acquisitions (Spirent, ESI, and optical design businesses) are tracking to plan with $375 million expected acquisition revenue for FY26.

What to Watch

Near-term catalysts:

- DesignCon and OFC conferences (next few weeks) will showcase AI infrastructure solutions

- Mobile World Congress 2026 in Barcelona for wireless ecosystem engagement

- February jobs report (March 6) could influence Fed rate path, impacting growth multiples

Risks:

- Tariff uncertainty: Management explicitly excluded Supreme Court ruling impacts from guidance

- Memory price increases: Keysight has "factored that into our outlook," but it bears monitoring

- Customer concentration: While broadening, AI remains concentrated among hyperscalers

Bull case: AI infrastructure buildout is "early innings"—management noted sovereign AI investments globally and edge AI applications are still largely ahead. The convergence of multiple technology waves (800G→1.6T→3.2T) creates sustained demand.

Bear case: Test equipment is historically cyclical. If AI capex growth moderates, Keysight's 20%+ growth rate could prove unsustainable. The stock trades at a premium that requires continued execution.

The Bottom Line

Keysight's blowout quarter validates its positioning as critical infrastructure for the AI buildout. Unlike hyperscaler capex announcements that drive headlines, test equipment represents the unglamorous but essential plumbing that enables AI systems to function reliably.

With wireline on its ninth consecutive quarter of growth, AI revenue still just 10% of the mix (and growing rapidly), and a record pipeline, Keysight appears to be in the early innings of capturing a structural shift in its end markets. The 15% after-hours move reflects both the magnitude of the beat and the market's recognition that this may be more than a one-quarter story.

Related:

Data sourced from company filings and S&P Global.