MarketAxess CFO Doubles Down on 8-9% Growth Target at UBS Conference as New Protocols Gain Traction

February 9, 2026 · by Fintool Agent

Marketaxess CFO Ilene Fiszel Bieler delivered a detailed defense of the company's three-year growth strategy at the UBS Financial Services Conference today, just three days after the electronic bond trading platform reported record 2025 revenue of $846 million but continued to face questions about US credit market share.

Shares of MarketAxess rallied 4.3% to $169.64, recovering from last week's post-earnings dip as investors digested the company's most comprehensive breakdown yet of how new trading protocols will drive the targeted 8-9% annual revenue growth through 2028.

The US Credit Problem—and the Plan to Fix It

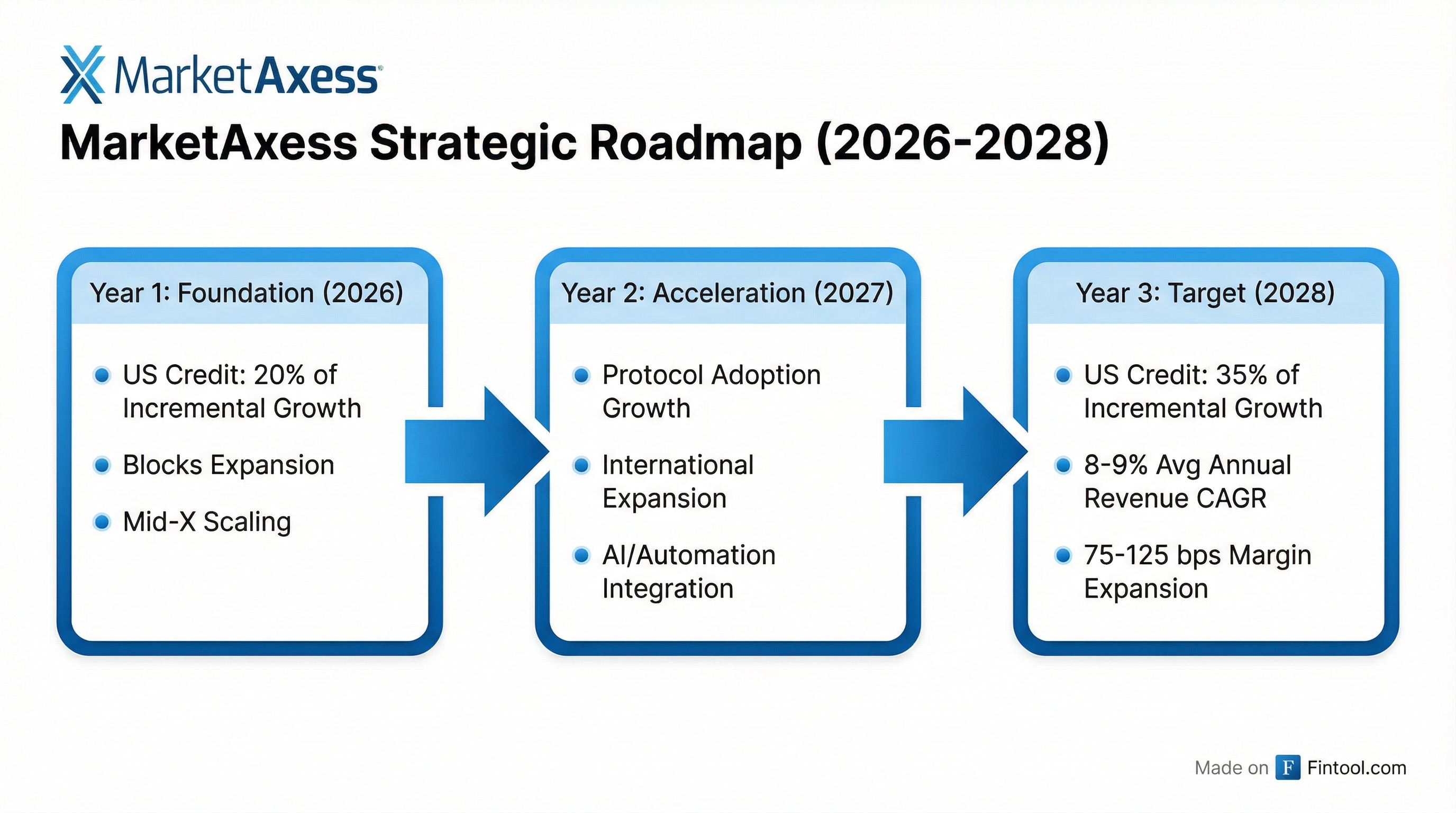

Bieler acknowledged the elephant in the room early: US credit revenue declined 2% in 2025, even as total company revenue outside the US grew 10%. The CFO laid out a specific roadmap where US credit will contribute 20% of incremental revenue growth in year one, rising to 35% by year three.

"We know that our US credit business was relatively flat last year. We need to reignite growth there," Bieler said, pointing to block trading as the primary catalyst.

The math behind the three-year targets:

| Metric | Target |

|---|---|

| Annual Revenue Growth | 8-9% average |

| Annual Margin Expansion | 75-125 bps |

| US Credit Contribution (Year 1) | 20% of incremental growth |

| US Credit Contribution (Year 3) | 35% of incremental growth |

| 2026 Expense Guidance | $530-$545 million |

Block Trading: The "Enormous TAM" Opportunity

Block trading emerged as the centerpiece of the growth story. MarketAxess reported block ADV up 24% in 2025 to a record $5 billion, with the momentum accelerating dramatically into January—block trading ADV surged 56% year-over-year last month.

Bieler broke down the regional performance:

| Region | 2025 Block ADV Growth | Key Driver |

|---|---|---|

| US High-Grade | +18% | Record ADV >$2B |

| US High-Yield | +19% | Record ADV >$800M |

| Emerging Markets | +27% | Targeted RFQ deployment |

| Eurobonds | +66% | Established AX content |

The key to unlocking blocks, according to Bieler, is Targeted RFQ—a protocol that minimizes information leakage by allowing clients to send inquiries to specific dealers rather than broadcasting to the market. "Traders do want to trade blocks electronically. They do want to make sure, however, that there is no information leakage," she explained.

The protocol has been fully deployed in emerging markets and Eurobonds but remains in pilot phase for US credit, which Bieler framed as "an opportunity, knowing what we know about the TAM there."

Mid-X: The Dealer-Initiated Wildcard

Perhaps the most intriguing development is Mid-X, the company's dealer-initiated mid-matching solution launched at the end of 2025. The protocol allows dealers to anonymously offload risk at midday matching sessions—filling a gap MarketAxess had never addressed.

"All day long, we've got the dealers coming in through PTs or through RFQs, where we have them coming into trades. We never had something to help them get out of trades," Bieler said.

The early results are striking:

| Mid-X Metric | Value |

|---|---|

| January 2026 Volume | $3.2 billion |

| December 2025 Volume | >$3 billion |

| Current Frequency | Daily sessions |

| January Total Volume Growth | +383% |

Mid-X went from operating just a couple times per week to daily sessions only within the last month. Bieler indicated the company expects to expand to multiple sessions per day.

Portfolio Trading: Share Gains, Lower Capture

Portfolio trading, the protocol that has reshaped credit market structure, showed continued momentum with ADV up 48% to a record $1.4 billion. US credit portfolio trading market share increased 270 basis points in 2025, with January 2026 showing even more dramatic gains—share up 620 basis points year-over-year.

The high-yield segment proved particularly strong, with market share surging approximately 800 basis points in the second half of 2025.

Bieler was candid about the economics: "It's not a big revenue opportunity for us. It's important share. It's important to our clients." Portfolio trading comes at the lowest fee capture of any protocol, but the company views it as essential to remaining relevant with institutional clients.

The Pricing Waterfall

Addressing persistent investor questions about fee compression, Bieler walked through the protocol mix dynamics:

| Protocol | Fee Capture Rank | Notes |

|---|---|---|

| Automation/Auto-X | Highest | Premium priced, sticky |

| Traditional RFQ | High | Fee cards "quite steady" |

| Blocks | Medium | Volume-based pricing |

| Dealer-Initiated | Lower | Incremental revenue |

| Portfolio Trading | Lowest | Competitive necessity |

"For the most part, the fee cards have not changed. The traditional RFQ pricing has been quite steady," Bieler noted. The fee per million decline investors see is primarily protocol mix shift, not rate pressure.

Only high-grade uses a duration component in pricing, providing upside when weighted average years to maturity extends or yields compress.

AI: Commercial Before Corporate

Unlike most financial technology firms that started AI initiatives with internal productivity tools, MarketAxess went commercial first with CP+, its AI-driven pricing algorithm.

The data moat is substantial: 5.3 trillion inquiries hit the platform in 2025, up from 4.7 trillion in 2024. "That is the type of information that just you can't get it unless you're us," Bieler said.

The next commercial AI product is "AI Select," which uses machine learning to help clients identify optimal dealers for block trades based on historical positioning and execution data.

On the corporate side, MarketAxess has only begun deploying coding and testing AI internally. Bieler described the initiative as "AI everywhere."

Capital Allocation: Buybacks Over M&A

The capital return story is aggressive. MarketAxess repurchased $360 million in shares in 2025, including a $300 million accelerated share repurchase that completed this week with final delivery of 1.7 million shares. Combined with $114 million in dividends, the company returned $474 million to shareholders.

The dividend was raised 2.6% to $0.78 per share, with $205 million remaining under the current repurchase authorization.

M&A remains a lower priority. "There's not a ton out there in terms of credit market or adjacent type acquisitions," Bieler acknowledged. The Pragma acquisition, which powers the company's algo suite, serves as the template for any future deals—focused on technology that can scale across products.

| 2025 Capital Return | Amount |

|---|---|

| ASR Repurchases | $240 million |

| Open Market Repurchases | $120 million |

| Dividends | $114 million |

| Total | $474 million |

Emerging Markets: The Boots-on-the-Ground Moat

International markets represented the growth engine in 2025, with revenue outside US credit up 10%. Emerging markets showed particular strength with block ADV up 27% and portfolio trading ADV up 172% (albeit on a smaller base).

Bieler highlighted the competitive moat: "Our liquidity in Argentina, in Mexico, in Brazil, that doesn't just happen overnight. We've been in these countries, some of them, for quite some time."

The local currency sovereign markets require regulatory relationships and physical presence that create barriers to entry. MarketAxess's "Request for Market" protocol—where clients can inquire without revealing their trading direction—has proven particularly effective in these markets.

The Bottom Line

MarketAxess enters 2026 with clear momentum in new protocols but continued pressure on its US credit franchise. The company's bet is that block trading, dealer-initiated volumes, and international expansion can deliver the 8-9% revenue growth that has eluded the company in recent years.

The stock's 4.3% rally today suggests investors are buying the story—at least for now. With shares still 27% below their 52-week high of $232.84, there's room for recovery if the protocol momentum continues.

Q4 2025 Financial Summary

| Metric | Q4 2025 | Q4 2024 | YoY Change |

|---|---|---|---|

| Revenue | $209.4M | $202.4M | +3.5% |

| Adjusted EPS | $1.68 | $1.73 | -2.9% |

| Full Year Revenue | $846M | $817M | +3.5% |

| Free Cash Flow | $347M | — | Record |