NXP Semiconductors Beats Q4 Estimates, Guides Q1 Above Street as Auto Recovery Takes Hold

February 2, 2026 · by Fintool Agent

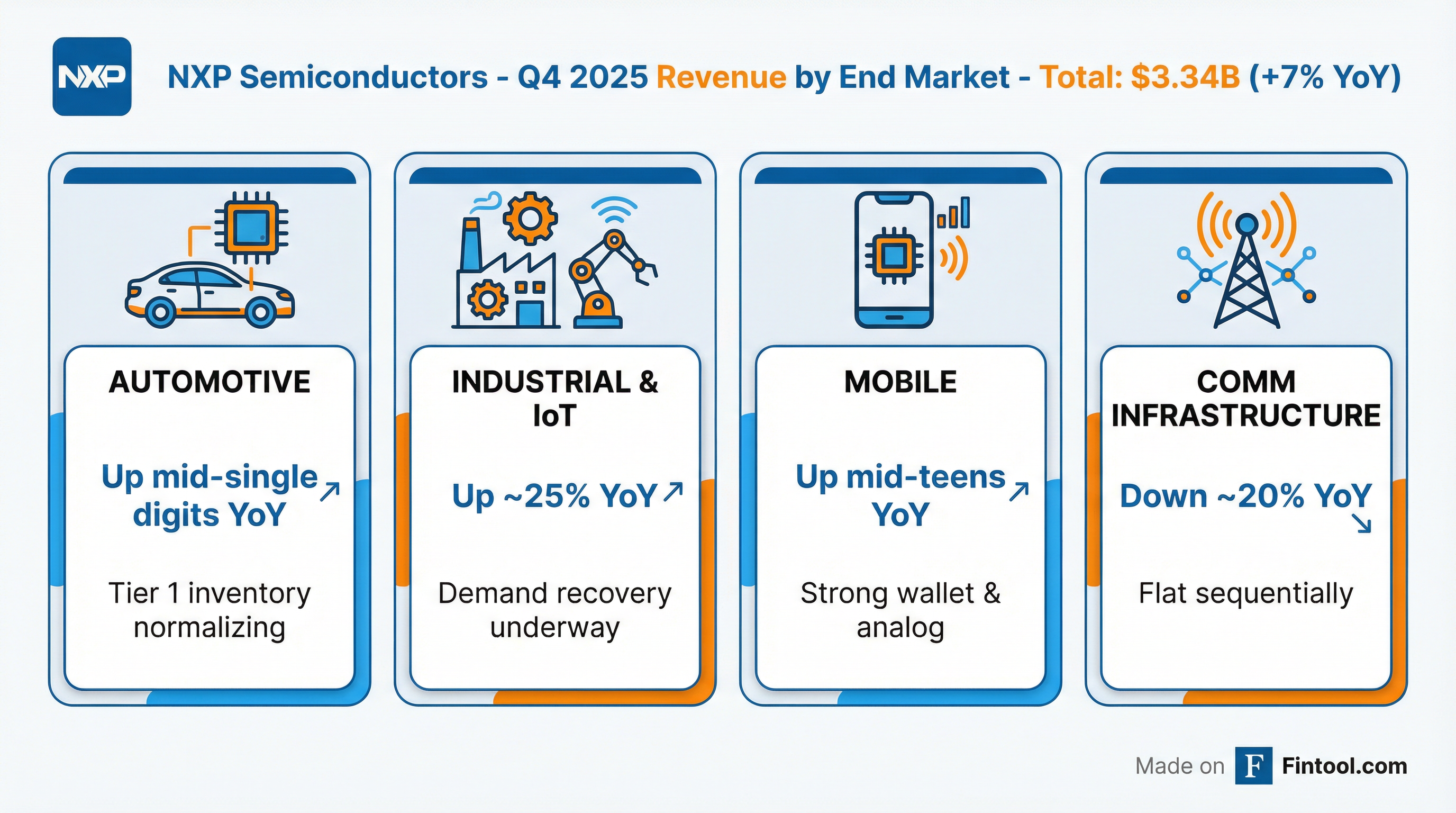

NXP Semiconductors delivered Q4 revenue of $3.34 billion, surpassing the $3.31 billion consensus estimate and rising 7% year-over-year. Adjusted EPS came in at $3.35, edging past the $3.31 Street expectation. The Dutch chipmaker guided Q1 2026 revenue to approximately $3.15 billion at the midpoint—above the $3.09 billion consensus—signaling that a multi-quarter inventory correction in its largest end market has finally run its course.

The results extend NXP's earnings beat streak to five consecutive quarters, though shares gave back early gains in after-hours trading, slipping to $219.85 from a regular session close of $231.08 (+2.2%).

The Numbers

| Metric | Q4 2025 | Estimate | Beat/Miss |

|---|---|---|---|

| Revenue | $3.34B | $3.31B | +0.8% |

| Adjusted EPS | $3.35 | $3.31 | +1.2% |

| Gross Margin | 57.5% | — | In-model |

| Operating Margin | 34.6% | — | In long-term model |

Q1 2026 Guidance:

- Revenue: ~$3.15B (midpoint) vs. $3.09B consensus

- Non-GAAP gross margin: ~57.5%

- Non-GAAP operating margin: ~34%

Automotive Inventory Finally Normalizes

The headline story is automotive—NXP's largest segment at roughly half of revenue. After eight quarters of undershipping to Tier 1 customers like Continental, Bosch, and Denso as they worked down elevated inventories, management declared the correction largely complete.

"We believe our shipments into the Tier 1 automotive supply chain best approach end demand," CEO Rafael Sotomayor said on the Q3 call. "We estimate that aggregate inventory levels of NXP-specific products at our major Tier 1 partners are below NXP's manufacturing cycle time."

This is significant because the inventory burn had been a persistent headwind masking underlying content growth. NXP was absorbing the digestion better than peers—Q3 automotive revenue was only 3% below its Q4 2023 peak, versus double-digit declines at competitors exposed to the same cycle.

Industrial & IoT: The Cyclical Surprise

Industrial & IoT, served primarily through distribution (80% of segment revenue), delivered the quarter's outperformance. Revenue was up approximately 25% year-over-year and 10% sequentially—well above typical seasonality.

Management attributed the strength to:

- Broad-based recovery across regions and products

- Energy storage systems and building automation driving core industrial

- Smart wearables creating new demand for high-performance, low-power processing

"We do remind you that we're not the bellwether for industrial and IoT," Sotomayor cautioned. "What we see, it may be that this is very company specific."

Distribution channel inventory remained at 9 weeks, below NXP's 11-week target, with management indicating they may selectively stage additional products as the recovery continues.

Strategic Acquisitions Close

NXP completed three acquisitions in Q4 that support its vision to lead in "intelligent edge systems":

| Acquisition | Focus | Strategic Value |

|---|---|---|

| TTTech Auto | Automotive software | Accelerates software-defined vehicle platform (S32) |

| Kinara | AI neural processors | Adds GenAI capability for edge applications |

| Aviva Links | SERDES technology | Standardizes sensor connectivity for radar/cameras |

"These acquisitions are directly aligned with bringing intelligent systems at the edge of industrial and automotive," Sotomayor explained. The deals are immaterial to near-term financials but expected to become material contributors by 2028.

Margin Trajectory Intact

NXP returned to its long-term operating model in Q4:

| Metric | Q4 2025 | Long-Term Model | Trend |

|---|---|---|---|

| Gross Margin | 57.5% | 57%-63% | In range |

| Operating Margin | 34.6% | 34%-38% | In range |

CFO Bill Betz reiterated the rule of thumb: every $1 billion in annual revenue drives approximately 100 basis points of gross margin improvement. At $15 billion in annual revenue, NXP should reach 60% gross margins.

Beyond 2027, the company expects an additional 200 basis points of margin expansion from its hybrid manufacturing strategy, including the VSMC joint venture in Singapore. "When VSMC is fully loaded in 2028, it will drive a 200 basis points improvement in NXP's total gross margin," Betz said.

What to Watch

Near-term catalysts:

- Q1 2026 execution on seasonal guidance ($3.15B midpoint)

- Distribution inventory normalization toward 11 weeks

- Automotive restocking—not yet visible but a potential upside driver

Longer-term:

- S32 automotive processing platform ramp

- Radar penetration in ADAS applications

- Integration of TTTech Auto, Kinara, and Aviva Links

- VSMC/ESMC foundry investments driving margin expansion

Revenue Trend: Sequential Improvement Continues

| Period | Revenue | YoY Change | QoQ Change |

|---|---|---|---|

| Q4 2023 | $3.42B | — | — |

| Q1 2024 | $3.13B | — | -8.5% |

| Q2 2024 | $3.13B | — | flat |

| Q3 2024 | $3.25B | — | +3.8% |

| Q4 2024 | $3.11B | -9.1% | -4.3% |

| Q1 2025 | $2.84B | -9.3% | -8.7% |

| Q2 2025 | $2.93B | -6.4% | +3.2% |

| Q3 2025 | $3.17B | -2.5% | +8.2% |

| Q4 2025 | $3.34B | +7.4% | +5.4% |

The trajectory shows a clear inflection: NXP's cyclical trough appears to have been Q1 2025, with four consecutive quarters of sequential improvement following.

The Bottom Line

NXP delivered a clean beat-and-raise quarter that validates the cyclical recovery thesis. The automotive inventory correction that weighed on results for two years has largely concluded, removing a significant headwind. Industrial & IoT showed surprising strength, while the company's strategic acquisitions position it well for the software-defined vehicle and edge AI opportunity.

The after-hours pullback likely reflects profit-taking after a 55% run from the 2025 lows rather than any fundamental concern with the quarter. With the cycle turning and company-specific growth drivers intact, NXP enters 2026 with its strongest setup in two years.

Related: NXP Semiconductors