Omnicom Doubles Synergy Target to $1.5B, Launches $5B Buyback in First Post-IPG Earnings

February 18, 2026 · by Fintool Agent

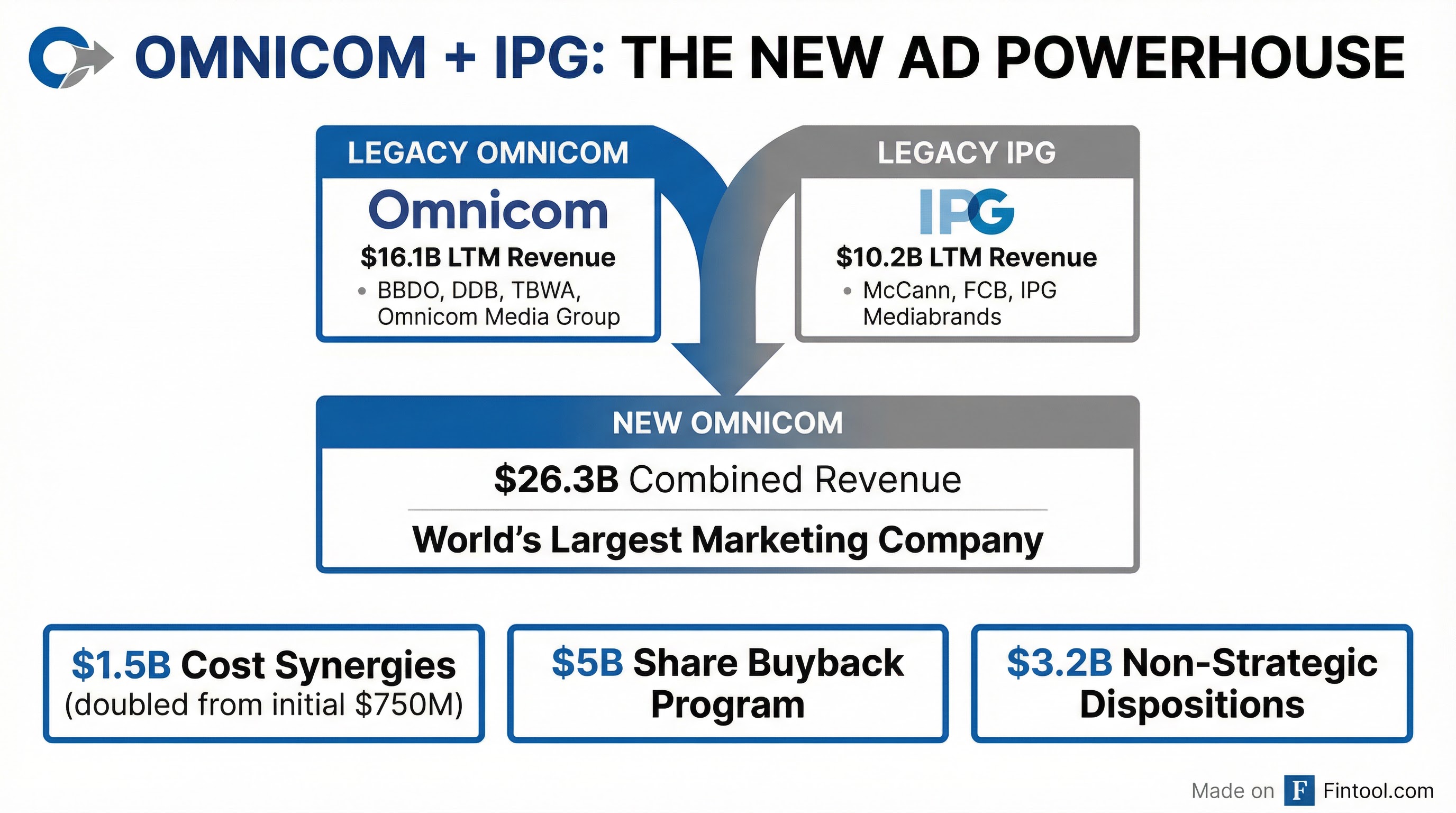

Omnicom Group delivered its first earnings report since completing the $13.25 billion acquisition of Interpublic Group, beating revenue estimates while unveiling an aggressive capital return program and dramatically expanded cost synergy targets that sent shares up 3.2% in regular trading and another 2.7% after hours.

The advertising giant reported Q4 revenue of $5.53 billion, up 27.9% year-over-year and exceeding the $5.04 billion analyst consensus. However, adjusted EPS of $2.59 fell short of the $2.65 estimate by $0.06, while the company recorded a GAAP net loss of $941 million due to $1.12 billion in severance and repositioning costs.

"Since the successful closing of the Interpublic acquisition on November 26, we made key leadership and brand announcements, refreshed our enterprise growth strategy, and launched the next generation of our Omni data and technology platform," CEO John Wren said on the earnings call.

Synergy Target Doubles to $1.5 Billion

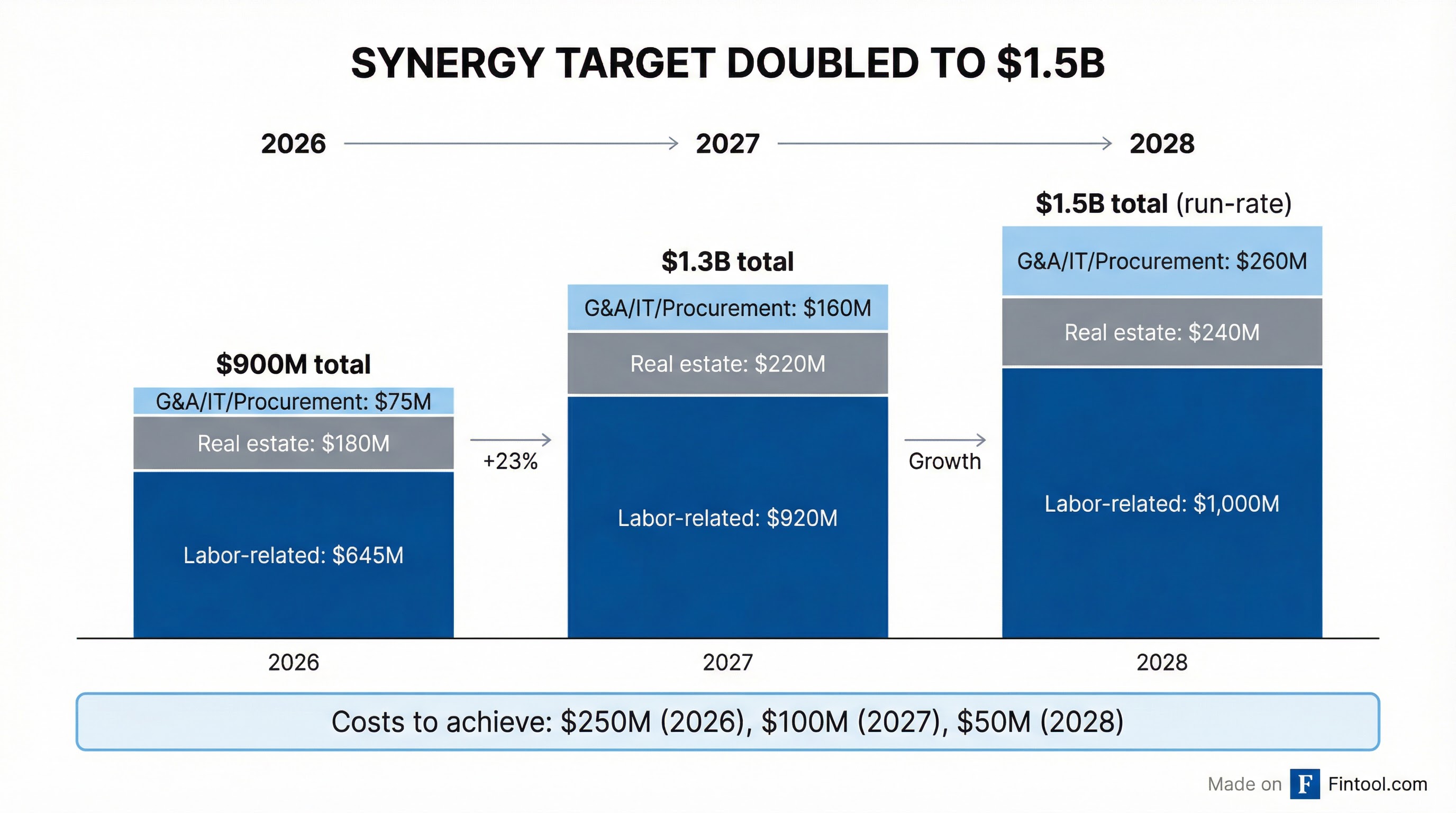

The most significant surprise was management's doubling of the cost synergy target from the initial $750 million estimate to $1.5 billion over 30 months—a clear signal that integration planning has revealed more overlap than originally anticipated.

The synergies break down across three categories:

| Category | 2026 | 2027 | 2028 (Run-Rate) |

|---|---|---|---|

| Labor-related | $645M | $920M | $1,000M |

| Real estate | $180M | $220M | $240M |

| G&A, IT, Procurement | $75M | $160M | $260M |

| Total | $900M | $1,300M | $1,500M |

Values retrieved from S&P Global

Costs to achieve these synergies are estimated at $250 million in 2026, $100 million in 2027, and $50 million in 2028.

"The key areas for these synergies are reductions in labor costs through the elimination of duplicative corporate network and operational functions, streamlining our regional, country, and brand structure, and optimizing utilization by shifting to a more unified resourcing model, including accelerating outsourcing and offshoring," Wren explained.

$5 Billion Share Buyback Signals Confidence

The board authorized a $5 billion share repurchase program, with management immediately launching a $2.5 billion accelerated share repurchase (ASR) arrangement. The company also plans to repurchase an additional $500 million to $1 billion during the remainder of 2026.

CFO Phil Angelastro outlined the impact: "We estimate the reduction to our shares outstanding compared to the balance of shares outstanding at December 31, 2025, of 313.1 million shares, will decline by approximately 9%-11% by the end of 2026, with weighted average shares outstanding for the year estimated to be reduced by approximately 7%-8%."

The aggressive capital return comes alongside a 15% dividend increase to $0.80 per share announced in December.

Portfolio Reshaping: $3.2 Billion in Dispositions

Omnicom moved quickly to reshape its portfolio, identifying approximately $3.2 billion in annual revenue for sale or exit. This includes:

- $700 million in smaller markets where Omnicom will move from majority to minority ownership

- $2.5 billion in non-strategic or underperforming operations to be sold or exited

The company has already completed dispositions representing over $800 million in annual revenue, including the sale of IPG's Jack Morton experiential business this week.

"Our retained portfolio of businesses generated revenue of $23.1 billion for the 12 months ended September 30, 2025," Wren noted. "This portfolio positions Omnicom to drive stronger growth and deliver measurable business outcomes for our clients."

The disposed businesses carried an average adjusted EBITDA margin of approximately 10%—significantly below the company's blended 15.6% margin—meaning dispositions are accretive to profitability.

Q4 Performance: Revenue Beats, Integration Costs Bite

The quarter's results reflect just one month of IPG operations following the November 26 close:

| Metric | Q4 2025 | Q4 2024 | Change |

|---|---|---|---|

| Revenue | $5.53B | $4.32B | +27.9% |

| Operating Income (Loss) | ($977M) | $685M | N/A |

| Adj. EBITA | $929M | $722M | +28.6% |

| Adj. EBITA Margin | 16.8% | 16.7% | +10bps |

| Diluted EPS (GAAP) | ($4.02) | $2.26 | N/A |

| Adj. Diluted EPS | $2.59 | $2.41 | +7.5% |

*Source: *

Excluding the planned dispositions and assets held for sale, organic growth would have been approximately 4%, according to Angelastro.

Media & Advertising now represents 60.1% of quarterly revenue, up from historical levels, reflecting Omnicom's strategic pivot toward higher-growth connected media capabilities.

Client Momentum and New Business Wins

Despite integration challenges, Wren highlighted strong commercial momentum: "We've secured new business and extended contracts with leading brands such as American Express, Bayer, BBVA, BNY, Clarins, Mercedes, and NatWest."

The company also received external validation when Forrester named Omnicom a leader in its commerce services evaluation. "The evaluation noted that clients praised Omnicom's ability to operate as a single agency, providing them with access to a large pool of highly qualified talent," Wren said.

2026 Outlook: More Details Coming at Investor Day

Management declined to provide specific 2026 guidance given the complexity of integration, but outlined several financial framework details:

- Net interest expense: Expected to increase by approximately $210 million compared to 2025, driven by IPG debt assumption and refinancing costs

- Tax rate: Expected at approximately 26% for planning purposes

- FX impact: Currency expected to benefit reported revenue by more than 2% assuming current rates hold

"Given the IPG acquisition recently closed, we have not yet completed our 2026 planning process. As a result, we will provide additional details on our expectations regarding revenue growth and EBITDA growth for 2026 at our Investor Day on March 12," Angelastro said.

Competitive Implications

The combination creates the world's largest marketing and sales company by revenue, surpassing WPP and intensifying competition in an industry already consolidating amid AI disruption. WPP recently announced its own restructuring of creative agencies.

Omnicom's enhanced scale provides leverage in media buying—its largest and fastest-growing segment—while the combined technology platform (Omni) integrates Acxiom's identity data, Flywheel's commerce cloud, and IPG's Interact capabilities.

Stock Reaction

Omnicom shares closed at $70.16, up 3.2% on the day, and rose to $72.05 in after-hours trading—a 2.7% additional gain. The stock remains 21% below its 52-week high of $89.27 but has stabilized from its recent low of $66.33.

What to Watch

- March 12 Investor Day: Management will provide 2026 revenue and EBITDA growth expectations

- Synergy execution: $900 million target for 2026 is aggressive; quarterly updates will be key

- Client retention: Integration risks remain; any material client losses would be a red flag

- Disposition progress: Completing the $2.5 billion in planned sales within 12 months

- AI integration: How effectively Omnicom deploys automation across creative and media workflows

Related Companies: Omnicom Group | WPP