Pan American Silver CEO: 'Buckle Up for Q1' as $87 Silver Drives Historic Margin Expansion

February 23, 2026 · by Fintool Agent

Pan American Silver CEO Michael Steinmann delivered a bullish message at the BMO 35th Global Metals, Mining & Critical Minerals Conference today, telling investors to "buckle up for Q1" as silver's surge to $87 per ounce drives what he called "unprecedented" margin expansion at the world's premier silver producer.

"The silver price was $58 average for the quarter. Right now, we're sitting at $85-$87, and a way higher average for Q1," Steinmann said from the Hollywood, Florida conference. "Really looking forward to the Q1 numbers."

The comments come just days after Pan American reported record Q4 2025 results, generating over $550 million in free cash flow in a single quarter—a staggering figure that could be eclipsed if current metal prices hold through Q1 2026.

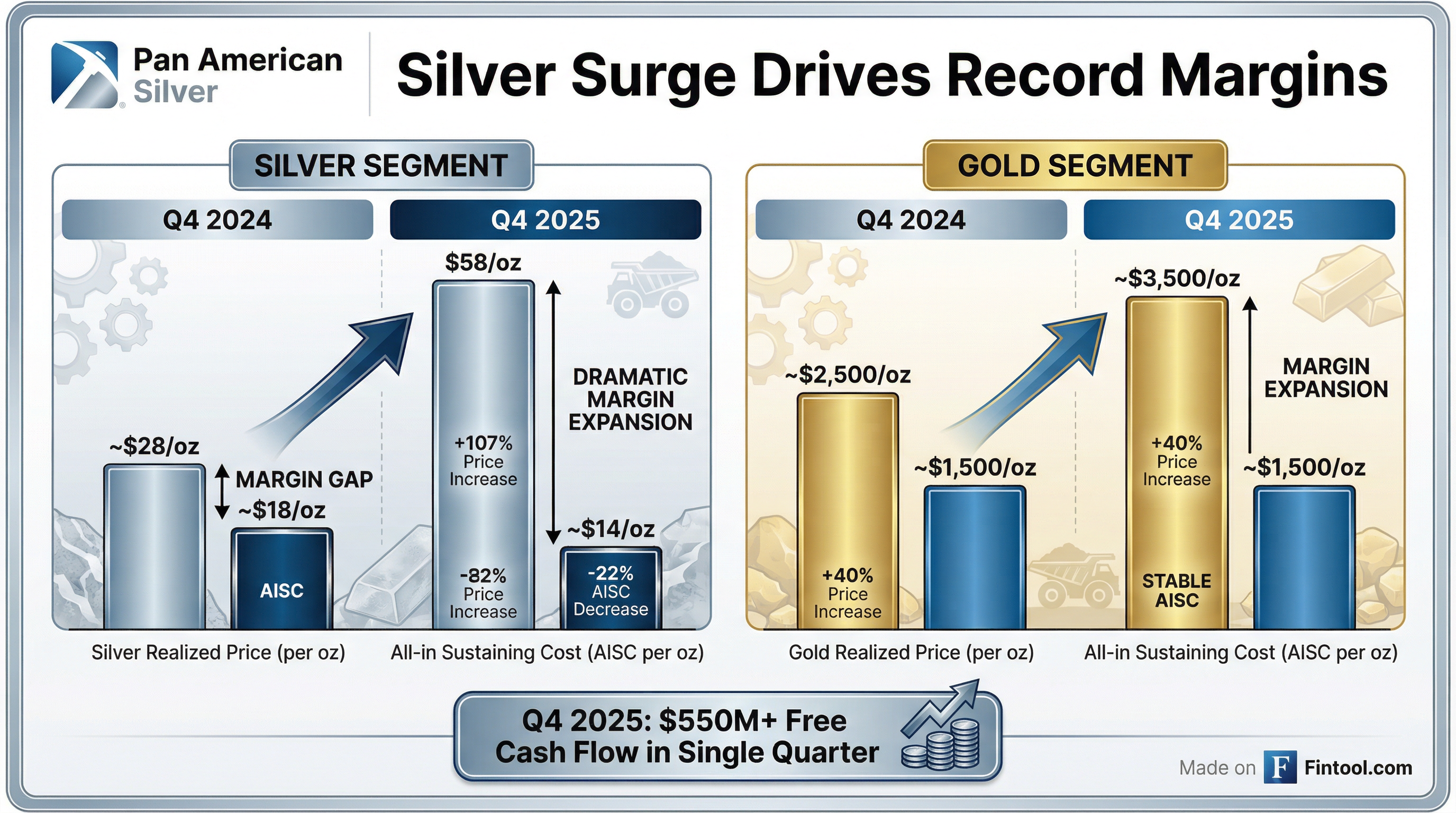

The Margin Story in Two Charts

Steinmann emphasized what he called the "really big impact" of the company's transformed cost structure, displaying margin data that shows a dramatic decoupling from the historical pattern where silver miners' costs would "cross over" during price rallies, erasing gains.

"Something that the market has been very critical in the past—where we saw the runs in metal prices, suddenly the costs would just cross over, and the whole run was over. This time it's very, very different," Steinmann said.

The transformation is driven by two factors: the September 2025 acquisition of MAG Silver's 44% interest in the Juanicipio mine—which Steinmann called "the best silver-producing asset globally on the planet"—and structurally lower costs from increased underground operations.

| Metric | Q4 2024 | Q4 2025 | Change |

|---|---|---|---|

| Revenue | $646M | $1,179M* | +82% |

| Net Income | $109M | $452M* | +315% |

| EBITDA | $268M | $560M* | +109% |

| Operating Cash Flow | $201M | $556M* | +177% |

*Values retrieved from S&P Global

Juanicipio: The 'Just in Time' Acquisition

The MAG Silver deal, which closed in September 2025, has proven transformative. Steinmann described it as "just in time," noting that metal prices began running "literally after we closed the deal."

The Juanicipio mine contributed 2.5 million ounces of silver in just four months of ownership, exceeding expectations. The mine's ultra-low costs—all-in sustaining costs in the $6-8/oz range compared to Pan American's corporate silver segment AISC of $15.75-18.25/oz—have pulled down the company's overall cost structure.

"The biggest decline, the biggest reason for that [cost improvement] is really the addition of the Juanicipio mine to our portfolio," Steinmann confirmed.

The $2.1 billion acquisition—comprising $500 million in cash and 60.2 million Pan American shares—gave MAG shareholders 14.3% of the combined company.

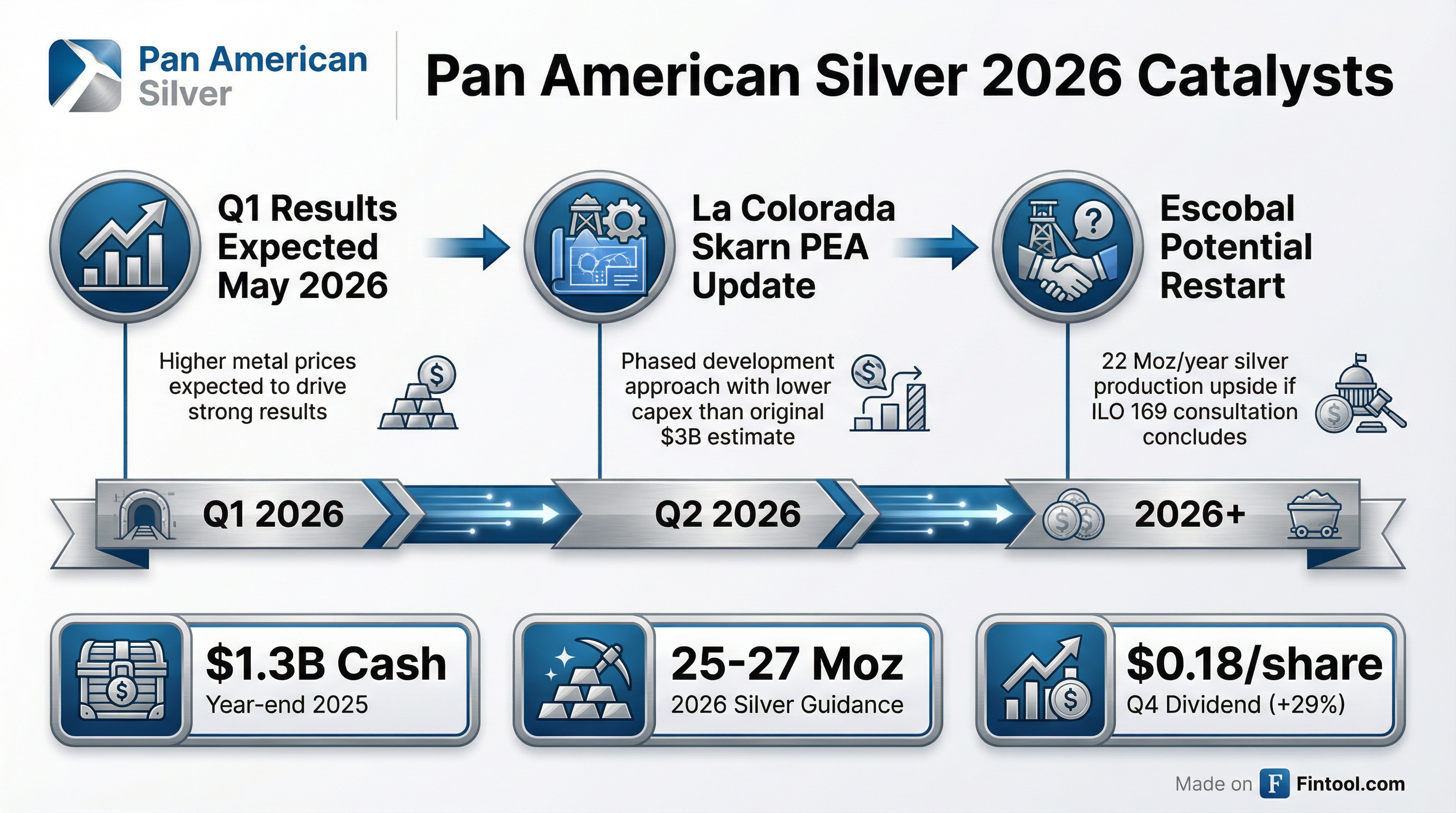

La Colorada Skarn: The Next Major Catalyst

Steinmann provided extensive color on La Colorada Skarn, calling it "one of the biggest base metal and biggest zinc discovery on the planet right now, with a very big silver credit." The project could add decades of production.

The company is pivoting from the original $3 billion block caving concept to a phased development approach that will cost "way, way less" and mine high-grade material first:

- Phase 1: Long-hole open stoping targeting high-grade zones at 10,000-15,000 tonnes per day

- Phase 2: Block caving operation "maybe 20-25 years" later, depending on metal prices

- Updated PEA: Expected Q2 2026

"The resource really varies so much between the mining methods that you use—maybe from 400-420 million tons to more than 700 million tons, depending how selective you go," Steinmann explained.

Escobal: The Hidden Upside

Pan American's most compelling—but uncertain—catalyst remains the Escobal mine in Guatemala, which Steinmann described as "the big upside for Pan American."

The shuttered mine could produce approximately 22 million ounces of silver annually at all-in costs that would likely be $12-13/oz (up from $8/oz when it last operated in 2017). The restart depends on completing an ILO Convention 169 consultation process with indigenous communities.

Critically, Pan American structured the acquisition with minimal downside risk:

"When we purchased the resource, we really didn't pay for the asset... We issued a CVR, a contingent value right for that asset. If it comes back into production and is de-risked, we will exchange those for Pan Am shares," Steinmann said.

The company would issue approximately 15 million shares (less than 4% dilution) to unlock 22 million ounces of annual silver production—a potentially transformative trade at current silver prices.

Capital Allocation: Dividends and Buybacks

With $1.3 billion in cash at year-end and minimal debt ($800 million in long-term bonds with the largest tranche not due until 2031 at 2.6% interest), Pan American is returning substantial capital to shareholders.

The company has increased its dividend for three consecutive quarters:

| Quarter | Dividend | Increase |

|---|---|---|

| Q2 2025 | $0.11 | +15% |

| Q3 2025 | $0.14 | +27% |

| Q4 2025 | $0.18 | +29% |

"If metal prices stay where they are or keep climbing, we will accelerate that return as well," Steinmann said, noting the company employs both dividends and share buybacks.

2026 Outlook: Strong but Back-Half Weighted

Pan American guides 25-27 million ounces of silver and 700-750 thousand ounces of gold for 2026, with production weighted toward the second half due to rainy season impacts on South American open pits.

Steinmann cautioned investors about quarterly seasonality: "We put the quarterly guidance in our MD&A, just to avoid that people just divide the production by 4. You're gonna outguide really your, as an analyst, where you think we're gonna be for the first two months, and then we will outperform on the second two months of the year always."

On costs, management expects approximately 8% wage inflation to flow through, translating to 3-4.5% operating cost increases depending on the asset. This is partially offset by lower cyanide and grinding media costs, plus favorable exchange rates if the dollar weakens.

Stock Performance and Valuation

PAAS shares have surged 217% from their 52-week low of $20.55, closing at $65.10 today—within striking distance of the $69.99 all-time high set earlier this year.

Analyst consensus price targets average $65.79, suggesting the market is catching up to the silver rally. J.P. Morgan forecasts silver averaging $81/oz in 2026, potentially rising to $85/oz by Q4.

| Metric | Value |

|---|---|

| Current Price | $65.10 |

| Market Cap | $23.9B |

| 52-Week Range | $20.55 - $69.99 |

| YTD Performance | +43% |

| P/E (TTM) | 24.4x |

*Values retrieved from S&P Global and market data as of February 23, 2026

What to Watch

Q1 2026 Results (Expected May 2026): With silver averaging well above Q4 levels, free cash flow could exceed the record $550M+ quarter.

La Colorada Skarn PEA (Q2 2026): The updated economic assessment will reveal capital requirements and returns for the phased approach, potentially a major re-rating catalyst.

Escobal Consultation Progress: Any movement on the ILO 169 process could unlock significant upside given current silver prices.

Silver Price Trajectory: At $87/oz, silver is nearing levels not seen since the Hunt Brothers squeeze. Whether prices hold or correct will determine the magnitude of Pan American's margin expansion.

Related Companies: Pan American Silver | Fresnillo | First Majestic Silver | Hecla Mining | Coeur Mining