Paramount Adds $650M Quarterly 'Ticking Fee' to $108B Warner Bros. Offer

February 10, 2026 · by Fintool Agent

Paramount Skydance is putting its money where its mouth is. The company sweetened its $30 per share all-cash offer for Warner Bros. Discovery on Tuesday, adding a novel "ticking fee" that will pay shareholders an extra $0.25 per share—roughly $650 million—for every quarter the deal remains unclosed past year-end 2026.

The move comes one day after Paramount certified compliance with the Department of Justice's Second Request—a key regulatory milestone—and as WBD's own proxy statement revealed that Netflix's headline $27.75 offer can sink as low as $21.23 depending on debt levels.

WBD shares rose 2% to $27.75 on the news, still trading below Paramount's $30 offer but now exactly at Netflix's maximum consideration.

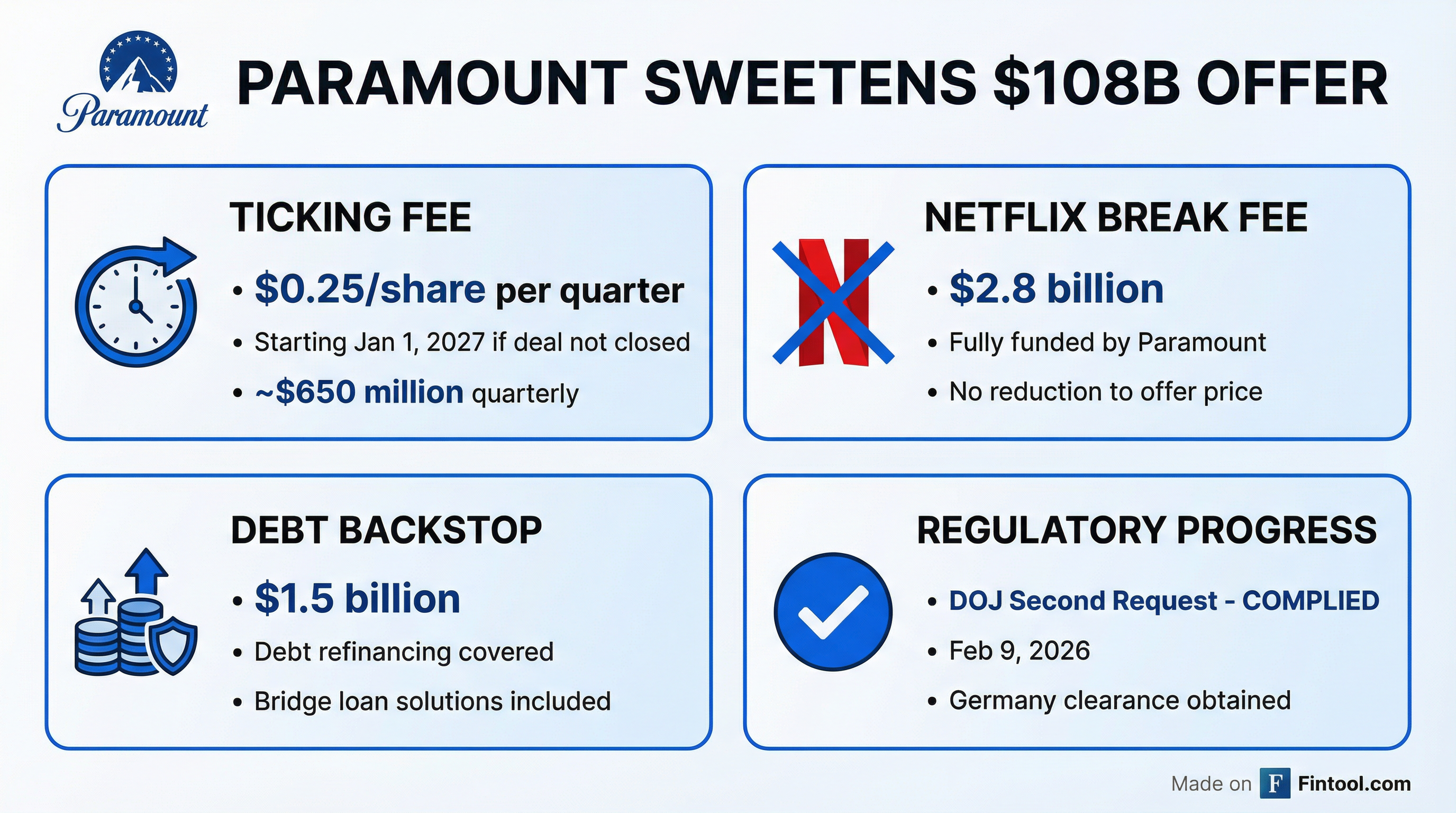

The Sweetened Terms

Paramount's revised offer doesn't raise the headline price, but it adds billions in shareholder protections and eliminates the "value leakage" concerns WBD's board has repeatedly cited.

Ticking Fee: $0.25 per share per quarter (~$650 million) for every quarter the transaction doesn't close past December 31, 2026. This is incremental to the $30 offer price—if the deal closes in Q2 2027, shareholders get $30.50.

Netflix Break Fee: Paramount will fund the $2.8 billion termination fee WBD would owe Netflix—as a separate payment, with no reduction to the $30 per share or the $5.8 billion reverse termination fee.

Debt Backstop: Paramount will eliminate WBD's potential $1.5 billion debt refinancing cost by backstopping an exchange offer that relieves bondholder obligations. If the exchange fails and Paramount's deal doesn't close, shareholders are fully reimbursed.

Bridge Loan: If WBD's current lenders won't extend the $15 billion bridge loan, Paramount's financing sources—Bank of America, Citigroup, and Apollo—will step in.

The total package remains fully financed by $43.6 billion of equity commitments from the Ellison family and RedBird Capital Partners, plus $54 billion in debt commitments—now explicitly covering all the new enhancements. Larry Ellison's personal guarantee has increased to $43.3 billion.

The Netflix Reality Check

Perhaps the most damaging revelation comes from WBD's own preliminary proxy statement, filed February 9. Paramount seized on a key detail: Netflix's consideration isn't actually $27.75.

According to WBD's disclosure, Netflix's offer "ranges from a minimum of $21.23 to a maximum of $27.75 per share in cash, depending on debt levels on Discovery Global at the time of separation."

That's a sliding scale that could cost WBD shareholders nearly $17 billion in value—the difference between $27.75 and $21.23 across 2.6 billion shares.

Paramount also applied a 10% discount rate to Netflix's $27.75 maximum, arguing that the 12-18 month timeline reduces the present value to approximately $26.45. "And unlike the Netflix transaction, which exposes WBD shareholders to this value destruction over the course of its long and uncertain approval timeline, our Revised Offer compensates WBD shareholders for any unanticipated delay in closing through an incremental ticking fee," Paramount wrote.

Regulatory Progress

Paramount certified compliance with the DOJ's Second Request on February 9, 2026—commencing a 10-day waiting period under Hart-Scott-Rodino rules. The company has also secured clearance from German foreign investment authorities as of January 27.

"To underscore our confidence in our ability to secure antitrust clearance and the progress we have made to date, we have added a $0.25 per share 'ticking fee,'" CEO David Ellison wrote in a letter to WBD shareholders.

This contrasts with Netflix, which faces heightened antitrust scrutiny over a deal that would combine the #1 and #3 streaming platforms. Congressional lawmakers have raised concerns about market concentration, and the regulatory path appears longer and less certain.

Market Reaction

WBD shares rose on the sweetened offer but remain at a telling level:

| Metric | Current | Paramount Offer | Netflix Max | Netflix Min |

|---|---|---|---|---|

| Price/Share | $27.75 | $30.00 + ticking fee | $27.75 | $21.23 |

| Premium to Current | — | +8.1% | 0% | -23.5% |

| Enterprise Value | $70B | $108B | $83B | — |

The stock trading at $27.75—exactly Netflix's maximum and 7.5% below Paramount's offer—suggests markets still see meaningful probability that Netflix prevails, despite the board's four rejections of Paramount.

RedBird's Gerry Cardinale told CNBC that if WBD's board still declines to engage, "we will continue going directly to shareholders to make the case."

"What we've done is we've perfected it by taking off the table all of the, what I call, more clerical items that they have been using to suggest that they are not going to engage with us," Cardinale said.

What's Next

Paramount's tender offer now expires March 2, 2026. As of February 9, roughly 42.3 million WBD shares had been tendered—a small fraction of the 2.6 billion outstanding, suggesting shareholders are waiting for developments before committing.

Key dates ahead:

- February 19, 2026: DOJ 10-day waiting period ends (earliest potential clearance)

- March 2, 2026: Paramount tender offer expires (unless extended)

- Q2-Q3 2026: Expected WBD annual meeting (proxy fight culmination)

- Q3 2026: Discovery Global separation expected (Netflix deal structure)

The ball is now firmly in WBD's court. With Paramount addressing every objection the board raised—financing certainty, regulatory path, value leakage—the question becomes whether WBD will engage or force this to a shareholder vote.

The Bottom Line

Paramount's sweetened offer doesn't raise the headline price, but it does something arguably more important: it eliminates every excuse WBD's board has used to avoid engagement.

The ticking fee signals regulatory confidence. The break fee funding removes Netflix's leverage. The debt backstop addresses bondholder concerns. And WBD's own proxy revealed that Netflix's $27.75 headline is actually a $21.23 floor with a sliding scale attached.

David Ellison, backed by his father Larry's now-$43.3 billion personal guarantee, is betting that $30 certain beats $21-$27.75 variable—and that WBD shareholders will agree when they understand the math.

Four rejections in. Billions on the table. And now a ticking clock that pays $650 million per quarter for every delay.

The WBD board's next move will determine whether this becomes the largest hostile deal in media history—or whether Netflix gets to absorb HBO and Warner Bros. for 30% less than Paramount offered.