SS&C CEO Says AI Enables 'Zero Headcount Growth' Despite Revenue Surge—Here's Why That Matters

February 9, 2026 · by Fintool Agent

SS&C Technologies CEO Rahul Kanwar delivered a striking data point at today's UBS Financial Services Conference: for the first time in 20 years at the company, headcount has remained essentially flat for three consecutive years while revenue continues to grow. The secret? AI-powered automation through the firm's Blue Prism acquisition—and Kanwar says the technology is now being packaged for clients facing the same margin pressures.

The comments come just days after SS&C posted record Q4 2025 results that beat consensus expectations, with adjusted EPS of $1.69 (up 18.2% YoY) and revenue of $1.65 billion (up 8.1%). The stock trades at $76.56, down 1% on Monday but up from its post-earnings low of $73.58 as investors digest the company's 2026 outlook.

Why GenAI Won't Disrupt Fund Administration

In a nuanced take that cuts against prevailing market fears about AI disruption, Kanwar explained why generative AI actually reinforces SS&C's competitive moat rather than threatening it.

"Our entire fund administration business is an accounting business," Kanwar told the conference. "What accounting systems require is they require ledgers. And they require that when you close a period, the period sort of stays closed."

The problem? GenAI doesn't deliver identical outputs. "In our experiments to date, GenAI and things like that are really good at a lot of things. They're not particularly good at leaving things the same," Kanwar noted. "You can ask ChatGPT a question that you asked last week, you'll get almost the same answer. It won't be word-for-word the same. In accounting, it has to be word-for-word the same."

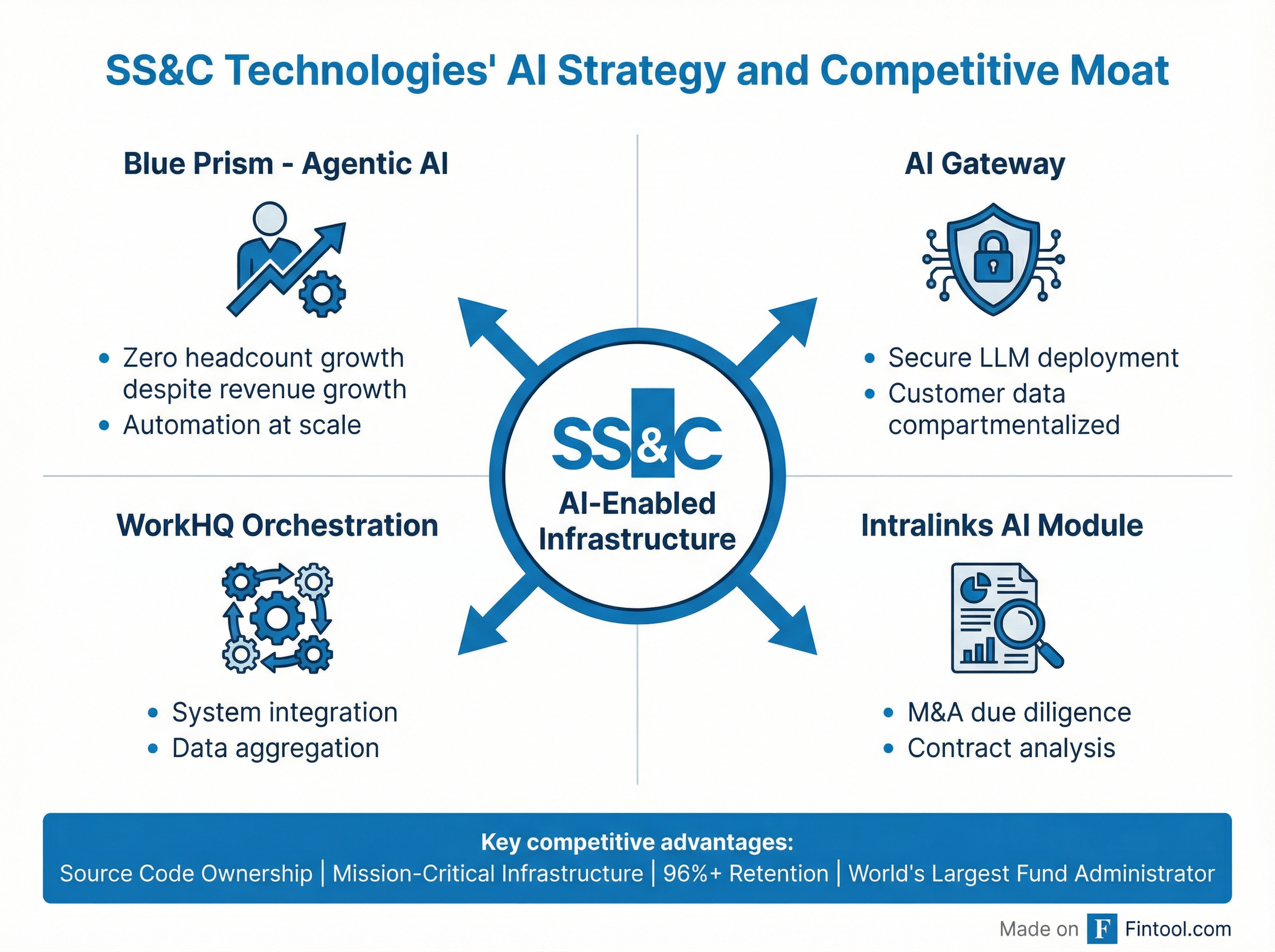

This technical limitation means GenAI is better suited for inputs and outputs around the core ledger—data ingestion, customer interfaces, and text analysis—rather than replacing the mission-critical accounting infrastructure itself. SS&C is deploying AI in precisely these peripheral areas through products like Intralinks' new AI module, which enables instant analysis of M&A data rooms that previously required hours of manual review.

The Blue Prism Payoff: Flat Headcount, Growing Revenue

The clearest evidence of SS&C's AI advantage shows up in its staffing metrics. Kanwar revealed that excluding acquisitions and liftouts (outsourcing deals where clients transfer operations to SS&C), headcount has been "virtually flat" for about three years—something he'd never seen in two decades at the company.

"I've almost always seen when revenue goes up, headcount goes up. I've never seen it just stay the same," Kanwar said. "Part of the reason we've been able to do it is because of this Blue Prism acquisition and the technology that we're rolling out across the place."

SS&C is now packaging these automation tools for external customers through two platforms:

- AI Gateway: Runs large language models within SS&C's secure infrastructure, compartmentalizing each customer's data to address confidentiality concerns that prevent financial institutions from using commercial GenAI directly

- WorkHQ: An orchestration platform that integrates data across disparate systems before applying AI analysis—solving the fragmentation problem that limits GenAI's usefulness for most enterprises

The pitch to clients mirrors SS&C's own experience: deploy AI to offset inflationary pressures while improving service quality. "When they see us do it and the way we're building these things, we're building them so that they can be deployed externally," Kanwar explained.

2026 Outlook: Targeting 40% EBITDA Margin

SS&C's 2026 guidance reflects continued margin discipline alongside steady organic growth:

| Metric | 2026 Guidance | 2025 Actual | YoY Growth |

|---|---|---|---|

| Revenue | $6.65-$6.74B | $6.27B* | 5-7% |

| Adjusted EPS | $6.70-$7.02 | $6.14* | 12% |

| Operating Cash Flow | $1.71-$1.81B | $1.74B* | 2% |

| EBITDA Margin Target | Exit at 40% | 39.3%* | +50bps |

*Values retrieved from S&P Global and company filings

The 50-basis-point margin expansion target comes despite ongoing "liftout" wins—large outsourcing contracts that arrive at lower margins before being integrated. Kanwar noted that acquired operations often start at 15-20% margins but typically reach 30-40% within 18-24 months.

"In effect, what we're doing with automation and productivity is a very good counter to some of the inflationary pressures that are out there," Kanwar said, citing rising technology vendor costs, employee compensation, and healthcare expenses as persistent headwinds.

Calastone and the Tokenization Opportunity

SS&C's recent Calastone acquisition positions the company in the emerging tokenized fund market—though Kanwar was measured about near-term expectations.

"It's not a huge part of our business right now," he acknowledged, noting SS&C currently services about a dozen tokenized funds. But the strategic rationale is compelling: tokenized funds still require all the same regulatory reporting, tax calculation, and accounting work as traditional funds—meaning tokenization is additive rather than disruptive to SS&C's core business.

"Somebody's got to tokenize the asset itself and then put it on a blockchain somewhere. That's the part that Calastone does," Kanwar explained. "So it gives us one more capability."

Calastone also brings a network connecting fund distributors with asset managers—providing cross-sell opportunities across SS&C's 23,000-customer base.

Customer Stickiness: 96%+ Retention

SS&C's retention metrics underscore the difficulty of displacing mission-critical infrastructure. Kanwar noted retention in the most recent quarter was approximately 96.4%—and emphasized the metric uses the "most punitive possible" methodology, counting only gross client losses with no credit for price increases or upsells.

"It does speak to the strength of the business that, in general, these are very, very sticky relationships," Kanwar said. "You're in there. You're in there. Absent some real dissatisfaction, people really don't want to switch."

The flip side? When SS&C wins new business, competitors face the same switching costs. "For whatever it is, there's plenty of dissatisfaction out in the marketplace," Kanwar noted, suggesting market share gains remain achievable despite industry stickiness.

Capital Return: Buybacks Over Debt Paydown

With net leverage at 2.8x EBITDA—down from approximately 7x after the 2018 DST Systems acquisition—SS&C has shifted capital allocation priorities toward shareholder returns.

In Q4 2025 alone, SS&C repurchased 3.7 million shares for $319 million at an average price of $85.81—well above today's trading level. Full-year 2025 capital deployment skewed roughly 60% toward buybacks and 30% toward debt reduction, with acquisitions opportunistically evaluated.

"We're a little more skewed towards buying back stock over the last couple of years," Kanwar confirmed. "Particularly at these kinds of valuations and share price kind of ranges."

Healthcare: The Long-Term Bet

SS&C's healthcare segment—centered on its DomaniRx pharmacy transaction system—remains a work in progress. Kanwar characterized it as a "long-term play" with "lumpy" revenue recognition, noting a multi-million dollar license that was expected in Q4 2025 closed in the first ten days of January instead.

The strategic case rests on technology differentiation: DomaniRx represents "over 1 million hours of code" and is the only new pharmacy management system at scale, according to Kanwar. Competitors largely run on dated infrastructure.

"We do think that our bet on healthcare has an outsized return," Kanwar said. "The point in time where it starts to return much more is coming."

The Bottom Line

SS&C's UBS appearance reinforced a consistent message: AI is an enabler rather than a disruptor for mission-critical financial infrastructure. The company's ability to hold headcount flat while growing revenue—and package that automation capability for clients—represents a tangible competitive advantage that's flowing through to margins.

At 12.5x forward earnings and an 8.5% free cash flow yield, the stock offers exposure to durable organic growth, disciplined capital returns, and optionality on healthcare and tokenization without requiring aggressive assumptions about AI monetization.

The key risk? Execution on margin expansion while simultaneously integrating liftout wins at sub-corporate profitability. Kanwar's track record on DST Systems—taking margins from 19% to the high 30s in 18 months—provides some comfort, but each new outsourcing deal resets the integration clock.

Related