Steel Dynamics and SGH Lodge 'Best and Final' $11 Billion Bid for BlueScope Steel

February 17, 2026 · by Fintool Agent

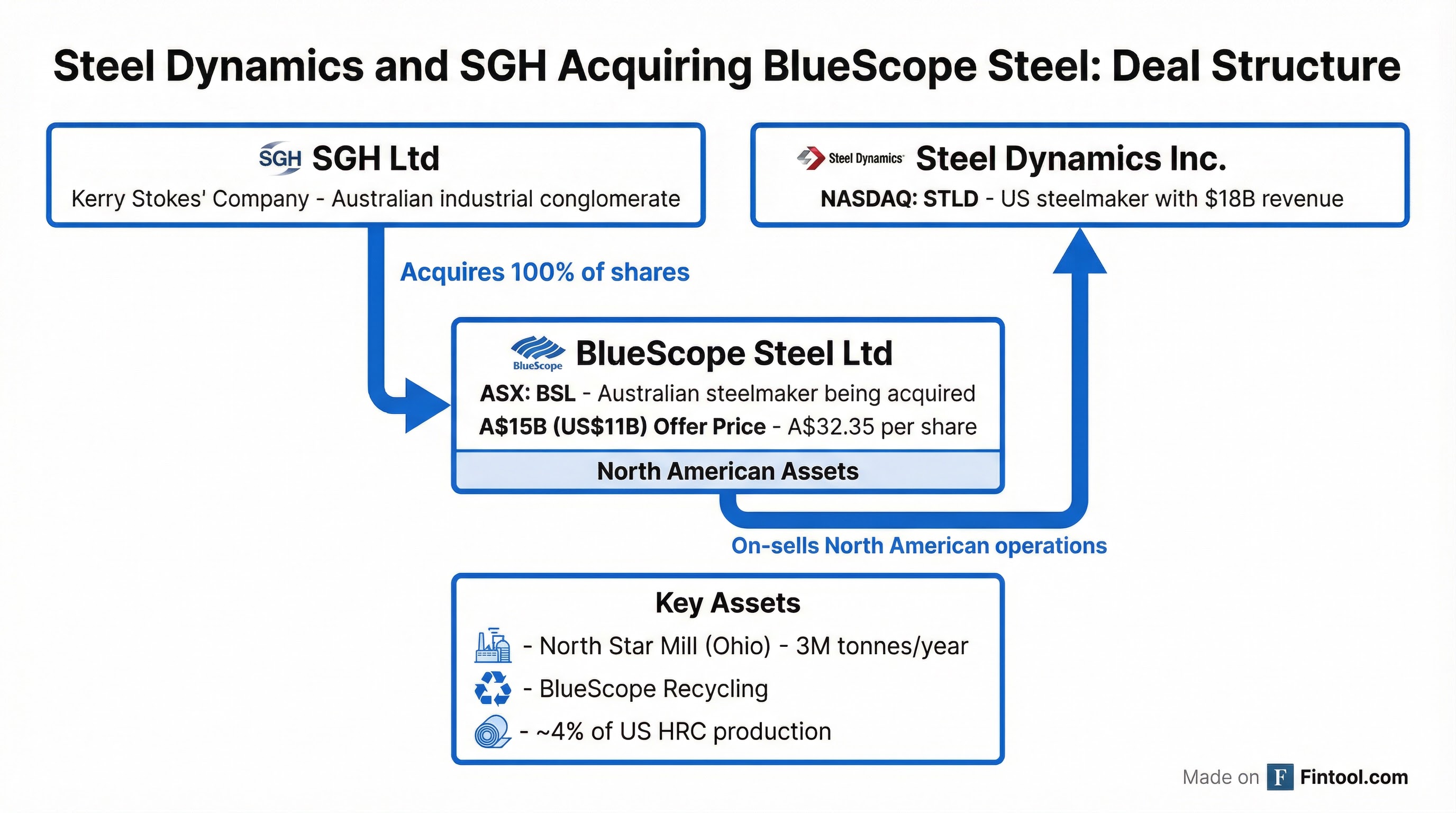

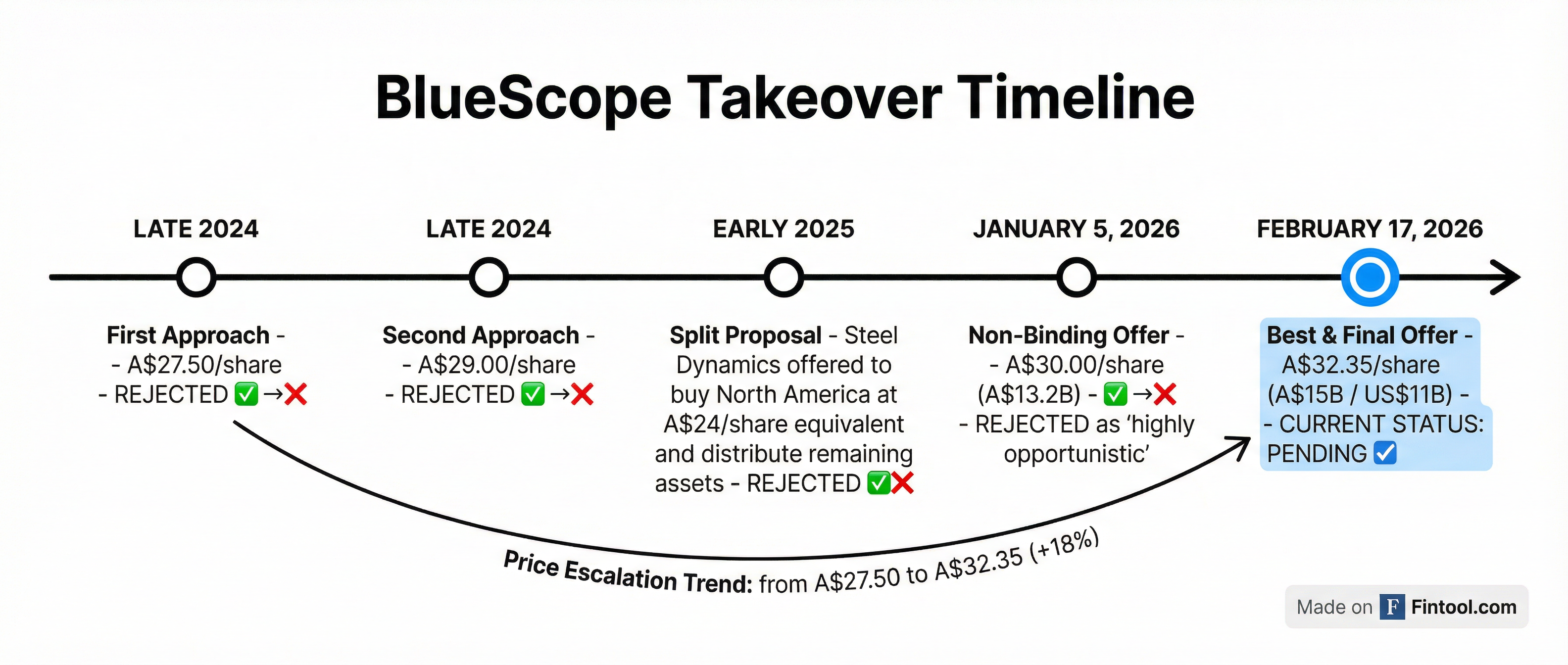

Steel Dynamics and Australian conglomerate SGH have raised their takeover offer for BlueScope Steel to A$32.35 per share in cash—a total equity value of A$15 billion (US$11 billion)—marking their fifth attempt to acquire the Australian steelmaker and its prized North American operations.

The consortium labeled this a "best and final offer," signaling the strategic pressure on BlueScope's board to engage or risk losing the bidders entirely.

The Deal at a Glance

The revised offer represents an 8% premium to the consortium's January bid of A$30 per share—and a 47% premium to BlueScope's undisturbed share price of A$23.66 on December 11, 2025, before deal speculation began.

Under the proposed structure, SGH—controlled by Australian billionaire Kerry Stokes—would acquire 100% of BlueScope via a scheme of arrangement. Steel Dynamics would then purchase BlueScope's North American businesses from SGH, gaining direct control of assets the Fort Wayne-based steelmaker has coveted for years.

Fifth Time's the Charm?

This bid marks the fifth approach from the Steel Dynamics-led consortium since late 2024:

| Date | Offer | Outcome |

|---|---|---|

| Late 2024 | A$27.50/share | Rejected |

| Late 2024 | A$29.00/share | Rejected |

| Early 2025 | Split proposal: A$24/share for North America + residual distribution | Rejected |

| January 5, 2026 | A$30.00/share (A$13.2B) | Rejected as "highly opportunistic" |

| February 17, 2026 | A$32.35/share (A$15B) | Pending |

BlueScope's board has been emphatic in its rejection of prior bids. In January, the company argued that the A$30 offer "failed to adequately recognise the value of BlueScope's assets" and came during a period of depressed steel spreads in Asia. The board noted that if spreads and FX rates reverted to historical averages, BlueScope could generate an additional A$400 million to A$900 million of EBIT annually.

The Prize: North Star and US Market Access

The crown jewel for Steel Dynamics is BlueScope's North Star steel mill in Delta, Ohio. The facility produces approximately 3 million tonnes of hot-rolled coil per year—roughly 4% of total US domestic production.

BlueScope has invested heavily in North Star:

- $735 million expansion (2022): Added a third electric arc furnace, increasing capacity from 2.2 to 3+ million tonnes

- $325 million acquisition (2021): Purchased three nearby scrap recycling facilities to secure feedstock supply

- $130 million debottlenecking (approved 2024): Further capacity expansion to 3.3 million tonnes by FY2028

For Steel Dynamics, acquiring North Star would significantly expand its US footprint. The company reported $18.2 billion in revenues for FY 2025 and has a market capitalization of approximately $28 billion.*

| Metric | FY 2023 | FY 2024 | FY 2025 |

|---|---|---|---|

| Revenue | $18.8B | $17.5B | $18.2B |

| Net Income | $2.5B | $1.5B | $1.2B |

| EBITDA Margin | 19.1%* | 13.8%* | 11.2%* |

| Total Debt | $3.2B | $3.3B* | $4.2B* |

*Values retrieved from S&P Global.

The Stokes Factor

The bid is being orchestrated by Kerry Stokes, an 85-year-old Australian billionaire worth approximately A$12.69 billion—Australia's 10th richest person according to the 2025 AFR Rich List.

Stokes built his fortune through a diversified empire spanning media (Seven West Media), heavy equipment (WesTrac, which distributes Caterpillar products), and construction materials (Boral). His company SGH Ltd (formerly Seven Group Holdings) has revenue of approximately A$10.7 billion.

The BlueScope acquisition would be one of the largest deals ever orchestrated by Stokes, who has a history of patient deal-making. His son, Ryan Stokes, serves as CEO of SGH and has been actively engaging BlueScope shareholders.

Why BlueScope Has Resisted

BlueScope's board has articulated several reasons for rejecting prior bids:

-

Cyclical timing: The bids have arrived during depressed steel spreads in Asia, understating BlueScope's normalized earning power

-

Growth pipeline: BlueScope has a $2.3 billion capital program underway with targeted $500 million per annum earnings uplift

-

Cost savings: The company expects $200 million of cost and productivity improvements in FY2026

-

Land portfolio monetization: BlueScope owns 1,200 hectares of land being rezoned for development

-

Synergy capture: The consortium would benefit from significant synergies that should accrue to BlueScope shareholders, not bidders

Just yesterday, BlueScope announced plans to push for continued growth in the US through North Star expansion and premium products—a signal that management believes the standalone path remains compelling.

What to Watch

The "best and final" language creates a clear decision point for BlueScope's board. Key considerations:

-

Shareholder pressure: Will major BlueScope shareholders push the board to engage? Expectations are that any successful deal will need to exceed A$15 billion.

-

Regulatory pathway: Previous bids were rejected partly due to "significant execution risk in relation to regulatory outcomes"

-

Competing bids: The consortium's offer is structured to be the final one "in the absence of a superior competing proposal for all or a material part of BSL"

-

Steel market dynamics: Rising protectionism and domestic steel demand in the US have made North American steel assets increasingly valuable

If completed, this would rank among the largest cross-border steel transactions in recent memory—and would give Steel Dynamics a significant expansion of its US capacity at a time when domestic steel production is increasingly strategic.

Related Companies: Steel Dynamics