Wheaton Pays $4.3B for BHP's Antamina Silver Stream—Largest Precious Metals Deal Ever

February 17, 2026 · by Fintool Agent

Wheaton Precious Metals announced a $4.3 billion silver streaming agreement with BHP on Tuesday—the largest precious metals streaming transaction in history—doubling its exposure to one of the world's premier copper-zinc operations and setting up 50% production growth by decade's end.

The deal was unveiled during a conference call Tuesday morning at 11:30 AM ET, hosted by outgoing CEO Randy Smallwood and incoming CEO Haytham Hodaly. Shares fell 3.9% to $140.27 on the news as investors digested the financing implications, though the stock remains up over 100% from November lows.

"Quality silver production is becoming increasingly difficult to source, while demand continues to rise for both critical industrial uses and for silver's safe haven qualities in today's economic environment," Smallwood said on the call. "The largest mining company in the world has chosen streaming as a means to unlock value, underscoring how compelling the streaming model has become."

Deal Terms: Record-Breaking Numbers

Under the agreement, Wheaton's subsidiary will acquire 33.75% of payable silver from BHP's stake in the Antamina mine in Peru, with the stream dropping to 22.5% after cumulative deliveries reach 100 million ounces. Wheaton will make ongoing payments equal to 20% of spot silver prices for delivered ounces.

The transaction doubles Wheaton's total Antamina exposure to 67.5% when combined with its existing stream on Glencore's share of production, acquired in 2015 for $900 million.

| Metric | Value |

|---|---|

| Upfront Payment | $4.3 billion |

| Initial Stream % | 33.75% of payable silver |

| Post-Threshold % | 22.5% (after 100M oz delivered) |

| Ongoing Payment | 20% of spot silver price |

| Effective Date | April 1, 2026 |

President Haytham Hodaly called Antamina "a proven, long-life, low-cost operation that will deliver immediate production and operating cash flow." The stream includes highly attractive structural terms: no buyback clause, a production percentage drop-down limited to one-third, and full BHP parent guarantee.

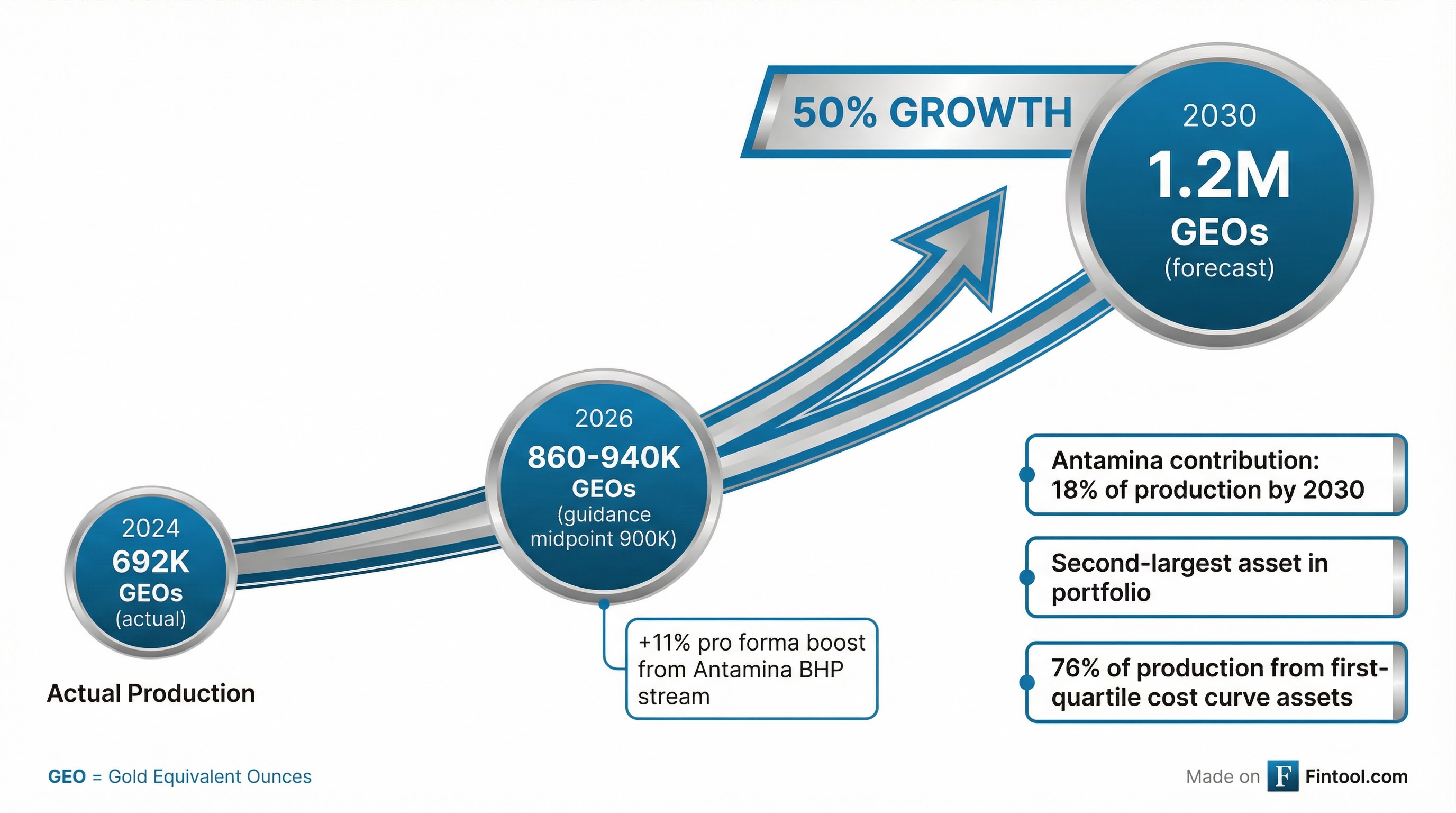

50% Production Growth by 2030

The Antamina stream transforms Wheaton's growth profile. Management issued updated 2026 guidance of 860,000-940,000 gold equivalent ounces (GEOs), with a midpoint of 900,000—an 11% pro forma boost from the transaction alone.

By 2030, production is forecast to reach 1.2 million GEOs, representing 50% growth from current levels. This growth trajectory is expected to be sustained through 2035 based on current mine plans.

| Year | Production (GEOs) | Notes |

|---|---|---|

| 2024 | 692,000 | Actual (9% above guidance midpoint) |

| 2026 | 860,000-940,000 | Guidance range |

| 2030 | 1,200,000 | +50% growth forecast |

VP Operations Wes Carson noted that Antamina has been Wheaton's strongest performer on a relative basis, having delivered 17% more silver ounces than originally anticipated since the 2015 Glencore deal. "We have witnessed firsthand improved safety and operational performance on site, translating directly into stronger delivery," Carson said.

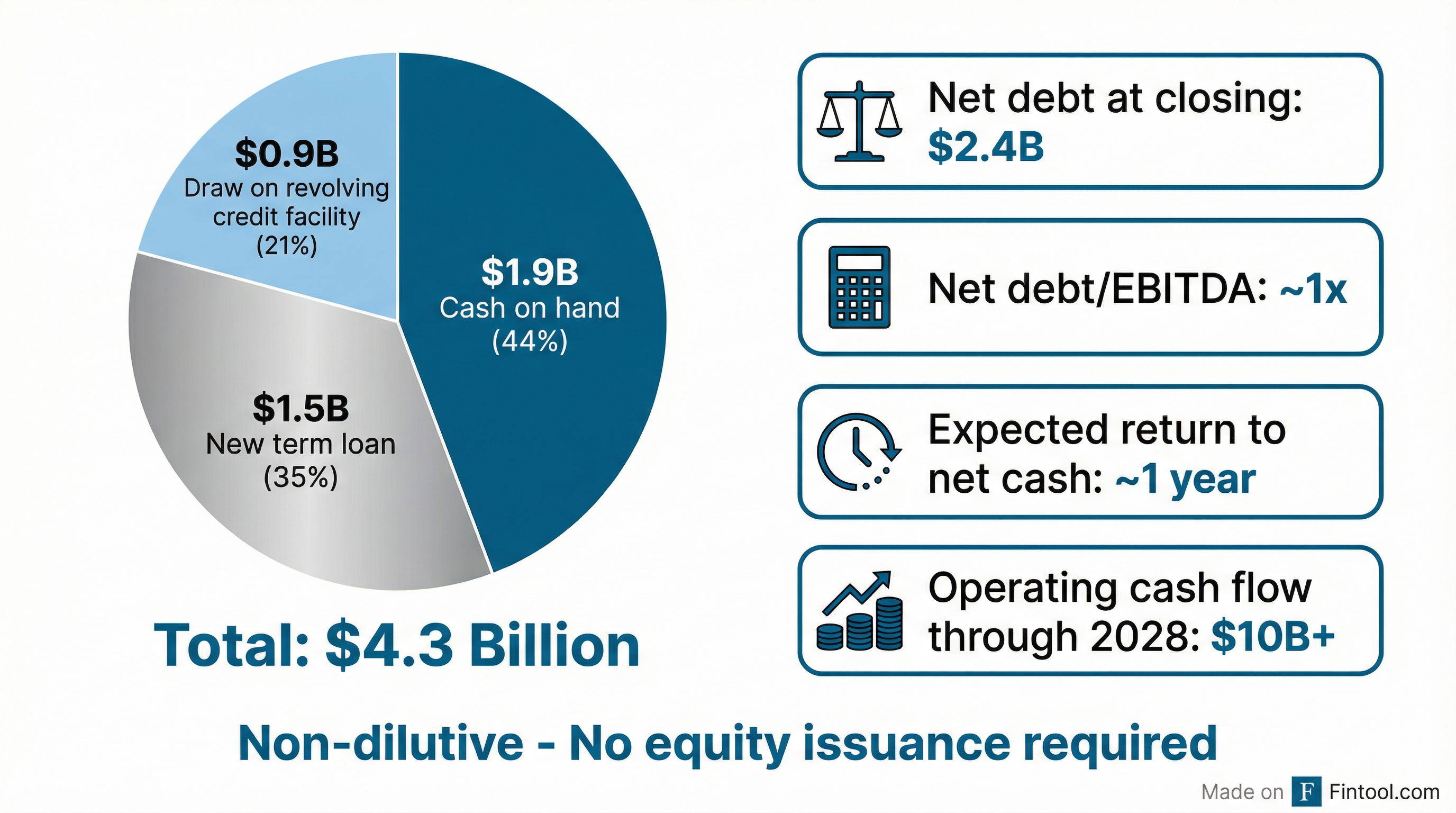

Financing: Back to Net Cash in One Year

The transaction is funded entirely without equity dilution. CFO Vincent Lau outlined the financing structure during the call:

- $1.9 billion in cash on hand (including $300M from recently monetized equity investments)

- $1.5 billion new two-year term loan (underwritten by BMO and Scotiabank)

- $0.9 billion draw on existing $2 billion revolving credit facility

Net debt at closing will be approximately $2.4 billion, translating to just 1x net debt/EBITDA—a "very comfortable level" according to Lau.

"With more than $3.2 billion in cash flows expected in 2026 alone and more than $10 billion in operating cash flow forecast to be generated through 2028, we currently expect to return to a net cash position in approximately one year," Lau said.

The deal's accretive nature was underscored by the math: at $4.3 billion, the investment represents just 6.5% of Wheaton's total market capitalization while boosting 2026 production by 11.3% on a pro forma basis.

Why BHP Chose Streaming

The transaction marks a strategic shift for BHP, the world's largest mining company, which is using precious metals streaming to fund future growth rather than repair a distressed balance sheet as Glencore did in 2015.

"Glencore was in a bit of a distressed financial situation [in 2015]. BHP obviously has a very, very strong credit position," Hodaly noted, pointing out that BHP is investment-grade rated by Moody's and Fitch. The deal increases Wheaton's exposure to investment-grade counterparties to 70%.

Smallwood was bullish on the pipeline implications: "The message that this sends, that streaming is an attractive source of capital to help fund growth—when I sit and think about the large companies around the world... the opportunity that I think this opens up is incredible."

The CEO hinted at ongoing discussions with "several of the larger companies" and highlighted copper development projects as the next frontier. "We will need new mines to get built, and those mines are tens of billions of dollars to get built. That is the perfect space for the streaming business model."

Antamina: A Multi-Generational Asset

Antamina sits in Peru's Ancash region of the Andes Mountains, 270 kilometers north of Lima, and has been operating since 2001. It ranks as one of the world's largest copper-zinc mines, contributing approximately 2.9% of Peru's GDP in 2024.

The mine is jointly owned by BHP (33.75%), Glencore (33.75%), Teck Resources (22.5%), and Mitsubishi (10%).

VP Corporate Development Neil Burns emphasized the asset's quality: "Antamina sits well within the first quartile of the global cost curve for copper, and is in fact the first significant asset in that quartile. With the addition of this stream to our portfolio, 76% of our production now falls within the lowest cost quartile."

Current reserves support mine operations through 2036, but management is confident in a much longer runway. Since Wheaton's first stream in 2015, over 95% of silver reserves have been replaced through resource conversion and exploration success. The land package—covering over 1,000 square kilometers—has grown 20-30% larger since the Glencore transaction.

"The potential at depth is something that can't be ignored," Burns said, noting that directional drilling from the pit's rim continues to return "wide intersections of similar grades" as the orebody is explored deeper. "One day it will transition to an underground mine. I think that's decades out there, but that potential certainly exists."

Silver Market Backdrop: Sixth Consecutive Deficit Year

The timing of the deal aligns with a structural tightening in silver markets. According to the Silver Institute, the market is heading for a sixth consecutive year of structural deficit in 2026, with supply failing to keep pace with demand.

Silver prices have surged dramatically, rising over 130% in 2025 from $29/oz to above $70/oz, driven by industrial demand (particularly solar manufacturing), safe-haven buying, and tight physical supply. J.P. Morgan now forecasts silver averaging $81/oz in 2026.

Smallwood called silver "the most critical mineral out there" during the Q&A session, noting: "We've been in a silver supply deficit for the last five years. We expect that deficit to continue for the next five years. Every time the silver price pulls back from one of these highs, it creates a new bottom, and investment demand is growing significantly."

What to Watch

Near-term catalysts:

- Deal closing expected April 1, 2026

- Full-year 2025 results conference call scheduled for March 13

- Salobo production guidance from Vale (expected shortly)

Longer-term considerations:

- Antamina mine life extension beyond 2036 (permitting in progress for tailings, pit, and waste dump expansions)

- Potential additional streams from Mitsubishi's 10% Antamina stake (the only remaining unstreambed silver share)

- Pipeline of 15-20 opportunities under evaluation, with majority focused on gold

- CEO transition: Haytham Hodaly taking over from Randy Smallwood

Key risk: The 33.75% stream drops to 22.5% after 100 million ounces are delivered. Based on forecasted production of ~6 million ounces annually, this threshold would be reached in approximately 16-17 years. The Glencore stream has a similar dropdown at 140 million ounces, with roughly 86 million ounces remaining before that trigger.

Related: Wheaton Precious Metals · BHP Group · Glencore · Teck Resources