Xerox Monetizes Its Brand: $450M IP-Backed Deal with TPG Funds Transformation

February 17, 2026 · by Fintool Agent

Xerox is turning to its most valuable intangible asset—its century-old trademark—to fund its survival. The company announced today that it has raised $450 million through a creative intellectual property joint venture with private credit investors led by TPG, monetizing the Xerox brand without selling it outright.

The deal, which closed today, represents one of the most significant IP-backed financings in recent memory and underscores how far legacy tech companies must go to fund transformations in an era of declining traditional businesses.

The Deal Structure

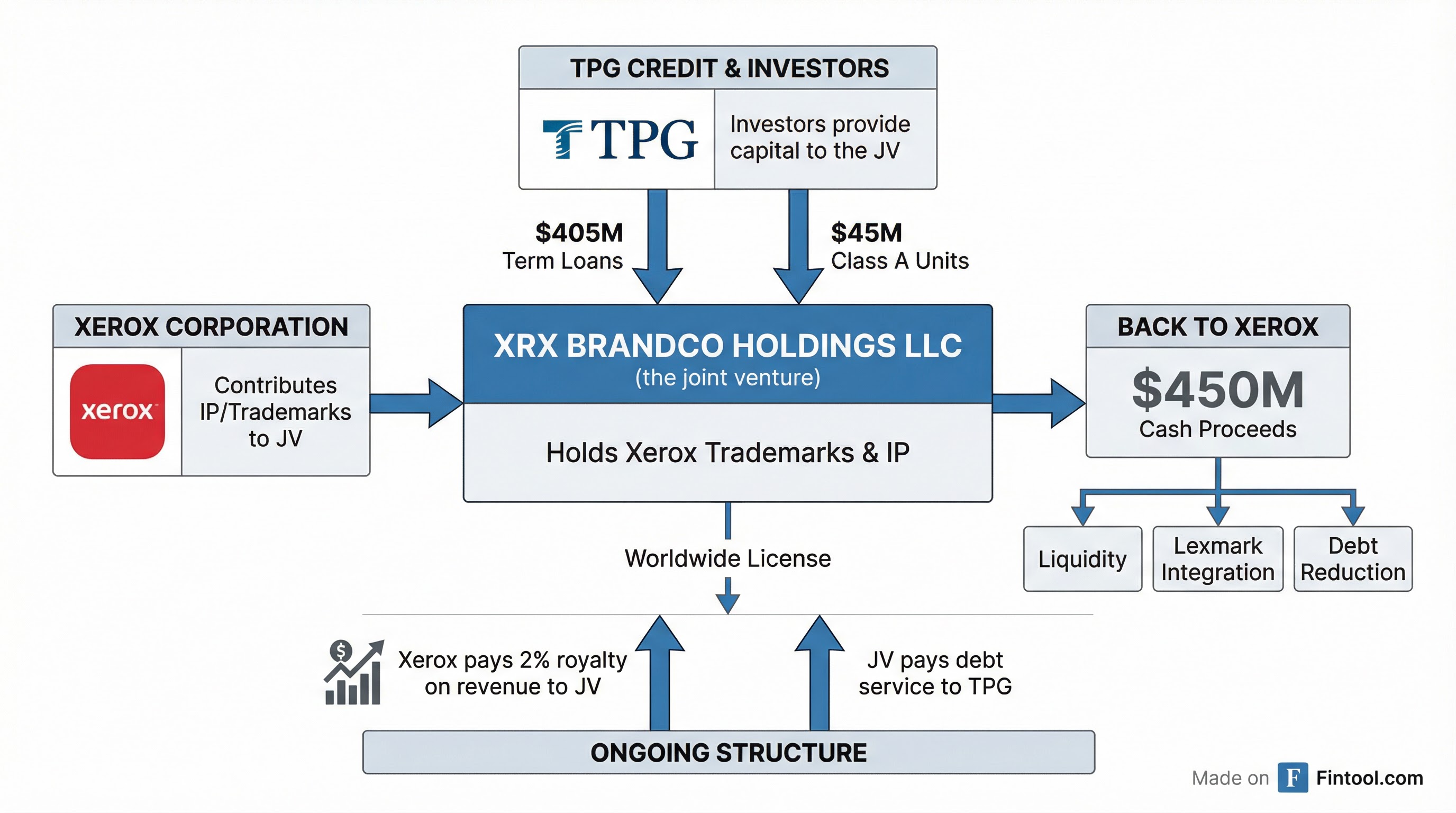

Xerox contributed its trademarks and related intellectual property—including the iconic "Xerox" brand name—to a newly formed joint venture called XRX Brandco Holdings LLC. In exchange, the company received Class B units in the JV and, crucially, a worldwide, royalty-free, non-exclusive license to continue using the IP.

TPG Credit led a consortium that provided $405 million in senior secured term loans and purchased $45 million in Class A equity units from the JV, with all proceeds flowing back to Xerox.

The financing comes at a steep price:

| Financing Terms | Details |

|---|---|

| Total Raised | $450 million |

| Term Loans | $405 million (SOFR + 8.125%) |

| Preferred Equity | $45 million (Class A Units) |

| Maturity | 5 years (February 2031) |

| Amortization | 4.5% annually starting Q4 2026 |

| Interest Rate Floor | 3.0% |

The loans are secured by the contributed IP and bear interest at SOFR plus 8.125%—a rate typically associated with distressed or highly leveraged borrowers. In a notable wrinkle, Xerox will now pay a 2% royalty on specified consolidated revenues to the JV, effectively renting back use of its own brand name.

Why Now?

The timing reflects Xerox's urgent need for liquidity as it executes an ambitious—and expensive—transformation strategy.

"This financing strengthens our balance sheet and completes the liquidity-enhancing actions we began in the fall," said Louie Pastor, Xerox president and COO.

The company has been on an acquisition spree:

- July 2025: Acquired Lexmark for $1.5 billion, expanding its printer and document services footprint

- November 2024: Acquired ITsavvy for approximately $400 million, boosting IT services capabilities

These deals have loaded the balance sheet with debt—total debt stood at $4.25 billion at the end of Q4 2025—while organic revenue continues to decline as enterprises shift to digital document workflows.

A Company in Transition

The numbers tell a stark story of a legacy business fighting secular headwinds:

| Metric | Q1 2025 | Q2 2025 | Q3 2025 | Q4 2025 |

|---|---|---|---|---|

| Revenue ($M) | $1,424* | $1,544* | $1,929* | $1,999 |

| Operating Income ($M) | ($15)* | $20 | ($51)* | $27 |

| Net Income ($M) | ($90) | ($106) | ($760) | ($73) |

| Total Debt ($M) | $3,508* | $4,146* | $4,754* | $4,247 |

*Values retrieved from S&P Global

While revenue jumped in the second half of 2025 following the Lexmark acquisition, organic revenue—excluding acquisitions—declined approximately 8%. The massive Q3 net loss reflected goodwill impairments and integration costs.

Xerox shares have cratered from around $8 a year ago to just $2.04 today—though the stock jumped 6.5% on the TPG announcement, with investors apparently viewing the liquidity injection as positive. The company's market cap has shrunk to approximately $262 million, a fraction of its debt load.

The Reinvention Gamble

Management calls its transformation strategy "Reinvention," and the TPG proceeds are explicitly earmarked to accelerate it. The plan has three pillars:

-

Lexmark Integration Synergies: Xerox is targeting at least $300 million in cumulative cost synergies from Lexmark by 2027, with $150-200 million expected in 2026

-

IT Services Growth: The ITsavvy acquisition and internal build-out aim to shift revenue toward higher-margin, recurring IT services rather than declining hardware sales

-

Cost Rationalization: The Reinvention program has already delivered over $200 million in gross savings, with a target exceeding $500 million

Management is guiding for more than $200 million in operating income improvement in 2026—an ambitious target given the company's recent track record.

Private Credit's Growing Power

The Xerox deal illustrates the expanding role of private credit in funding corporate transformations that traditional lenders won't touch.

TPG, the San Francisco-based alternative asset manager with $303 billion in assets under management, provided the financing through its credit arm. The deal structure—secured by intellectual property with a licensing arrangement—allows Xerox to monetize an asset that traditional banks struggle to value or accept as collateral.

"TPG is pleased to be a capital partner to Xerox and have the opportunity to help strengthen its balance sheet and support the execution of its long-term growth strategy," said Joe Lenz, Partner and Co-Head of Research at TPG Credit Solutions.

For Xerox, the cost is steep: an all-in interest rate likely exceeding 12% (SOFR at ~4% plus the 8.125% spread), plus the ongoing 2% royalty on revenues. But for a company with limited options, it buys time to execute.

What to Watch

The TPG deal provides breathing room, but several catalysts will determine whether Xerox's Reinvention succeeds:

- Q1 2026 Earnings (May 2026): First full quarter integrating both acquisitions; investors will scrutinize organic revenue trends and synergy realization

- Lexmark Synergy Milestones: Management must demonstrate concrete progress toward the $150-200 million 2026 synergy target

- Tariff Headwinds: With production increasingly moving in-house to mitigate tariff exposure, execution on manufacturing transitions will be critical

- Debt Reduction: The proceeds are partly earmarked for debt paydown—watch for refinancing announcements

The Xerox name—invented in 1938 from Greek words meaning "dry writing"—has survived the transition from analog copiers to digital document management. Whether it can survive the AI revolution and fund a true business transformation remains the $450 million question.

Related: