Earnings summaries and quarterly performance for Allegion.

Executive leadership at Allegion.

John Stone

President and Chief Executive Officer

David Ilardi

Senior Vice President, Allegion Americas

Jennifer Hawes

Senior Vice President and Chief Human Resources Officer

Michael Wagnes

Senior Vice President and Chief Financial Officer

Nickolas Musial

Vice President, Controller and Chief Accounting Officer

Robert Martens

Senior Vice President and Chief Innovation and Design Officer

Timothy Eckersley

President, International, and Senior Vice President, Allegion

Tracy Kemp

Senior Vice President and Chief Information and Digital Officer

Vincent Wenos

Senior Vice President and Chief Technology Officer

Board of directors at Allegion.

Research analysts who have asked questions during Allegion earnings calls.

Julian Mitchell

Barclays Investment Bank

6 questions for ALLE

Brett Linzey

Mizuho Securities

5 questions for ALLE

Christopher Snyder

Morgan Stanley

5 questions for ALLE

Jeffrey Sprague

Vertical Research Partners

5 questions for ALLE

Tomohiko Sano

JPMorgan Chase & Co.

5 questions for ALLE

Joe O'Dea

Wells Fargo

4 questions for ALLE

Joseph O'Dea

Wells Fargo & Company

4 questions for ALLE

Andrew Obin

Bank of America

3 questions for ALLE

Robert Schultz

Baird

3 questions for ALLE

Joe Ritchie

Goldman Sachs

2 questions for ALLE

Timothy Wojs

Robert W. Baird & Co.

2 questions for ALLE

Tim Wojs

Robert W. Baird & Co. Incorporated

2 questions for ALLE

Joseph Nolan

Longbow Research

1 question for ALLE

Joseph Ritchie

Goldman Sachs

1 question for ALLE

Peter Costa

Mizuho Financial Group

1 question for ALLE

Vivek Srivastava

Wolfe Research

1 question for ALLE

Recent press releases and 8-K filings for ALLE.

- 2026 guidance: Non-residential volume growth expected in line with 2025; residential segment remains soft; anticipate typical seasonality with Q1 mirroring Q4 and stronger Q2–Q3 activity.

- Institutional and commercial markets: Broad non-residential organic growth driven by stable institutional aftermarket and municipal bond–funded projects; office Class A demand recovering and early green shoots in multifamily.

- Electronics and services mix: Electronics, software & services accounted for 33% of 2025 revenue with double-digit growth; connected locks and acquisitions like ELATEC underpin the strategy to outpace mechanical products.

- M&A and international focus: Active acquisition pipeline in Americas and International, prioritizing electronics/software targets; key markets are Australia, New Zealand and Western Europe, with no near-term expansion into new geographies.

- Pricing and margins: Strong pricing power in non-residential to cover inflation; residential margins pressured by volume deleverage; Q1 2026 margins expected to show pressure from tariff-related price recovery.

- Guided non-residential volumes in Q1 2026 to track in line with 2025, noting typical seasonality with lighter Q1/Q4 and busier Q2/Q3 quarters.

- Expects the residential segment to remain soft and potentially lumpy in 2026 due to channel inventory dynamics and customer concentration.

- Electronics, software and services represent 33% of total revenue, with electronics growing double-digit in 2025; pursuing disciplined M&A (e.g., ELATEC, Waitwhile) to advance connected-lock solutions.

- International business is delivering profitable growth after divesting non-core assets, focusing on Australia/New Zealand and Western Europe while leveraging modular designs for faster product introduction.

- Allegion expects non-residential volume growth in 2026 to match 2025, with Q1 seasonality mirroring Q4 and busier Q2/Q3, while residential demand remains soft and lumpy.

- Electronics, software and services represent 33% of total revenues, with double-digit growth in 2025 driven by acquisitions such as ELATEC and software integrations (Waitwhile, Gatewise) to advance connected lock solutions.

- International segment delivered profitable growth and is targeting further margin expansion, focusing on Australia, New Zealand and Western Europe after divesting in China, South Korea and Australia to improve portfolio quality.

- Data center vertical, once “small,” is now a growing high-security market, leveraging Allegion’s spec writing and end-user relationships with hyperscalers.

- Allegion reported Q4 revenue of $1.0 billion, up 9.3% year-over-year and 3.3% organically; Q4 adjusted operating margin was 22.4%, and adjusted EPS was $1.94, a 4.3% increase.

- Americas segment revenue was $795.5 million, up 6.1% (organic + 4.8%), driven by non-residential growth despite a high-single-digit residential decline; International revenue was $237.7 million, up 21.5% (organic – 2.3%).

- Full-year available cash flow reached $685.7 million, up 17.6%, and net debt to adjusted EBITDA was 1.6×, supporting continued capital deployment.

- In 2025, Allegion deployed approximately $630 million in M&A, paid $175 million in dividends (12th consecutive annual increase), and repurchased $80 million of shares.

- For FY 2026, Allegion expects total revenue growth of 5–7% (organic 2–4%) and adjusted EPS of $8.70–$8.90, implying ~8% EPS growth at the midpoint.

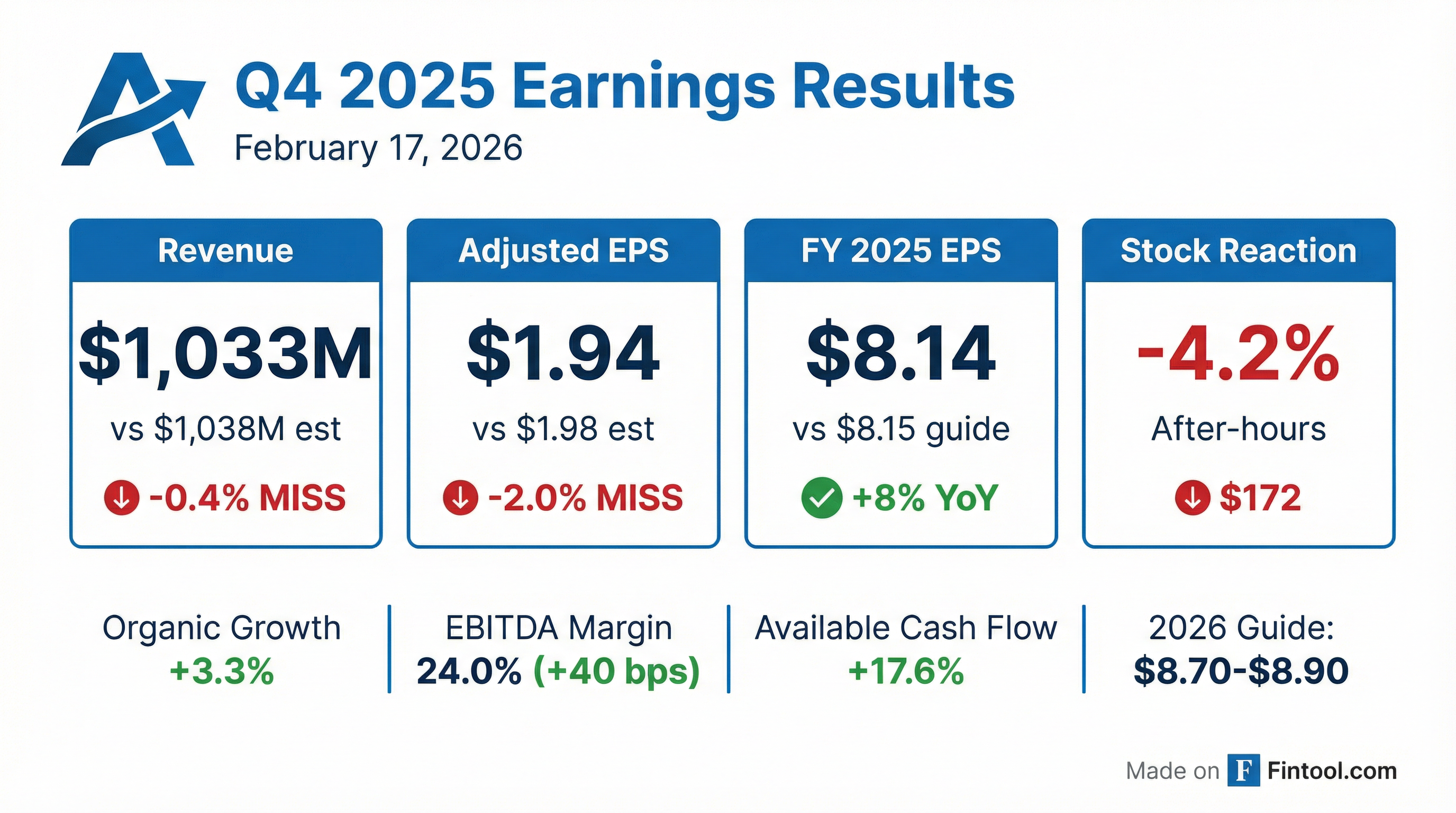

- Q4 revenue increased 9.3% to $1,033.2 million; adjusted EPS was $1.94, a 4.3% rise year-over-year.

- FY-2025 revenue rose 7.8% to $4,067.3 million; adjusted EPS reached $8.14, up from $7.53.

- Available cash flow grew 17.6% to $685.7 million, while gross debt/EBITDA leverage improved to 2.0x at year-end.

- FY-2026 guidance targets 5.0%–7.0% revenue growth and $8.70–$8.90 adjusted EPS.

- Allegion delivered Q4 2025 revenue of over $1 billion, up 9.3% year-over-year (organic +3.3%), with adjusted operating margin of 22.4% (+30 bps) and adjusted EPS of $1.94 (+4.3%).

- Americas segment Q4 revenue was $795.5 million (+6.1% reported, +4.8% organic), led by non-residential, while International revenue reached $237.7 million (+21.5% reported, –2.3% organic).

- For FY2026, Allegion expects total revenue growth of 5–7% (organic 2–4%) and adjusted EPS of $8.70–$8.90 per share.

- In 2025, Allegion deployed $630 million in acquisitions, paid $175 million in dividends (12th consecutive annual increase), and repurchased $80 million of shares.

- Available cash flow for 2025 was $685.7 million (up 17.6%), with net debt to adjusted EBITDA at 1.6×, underpinning continued capital deployment.

- Allegion’s Q4 2025 revenue was over $1 billion, up 9.3% reported and 3.3% organic; adjusted operating margin rose to 22.4%, and adjusted EPS was $1.94, up 4.3% year-over-year.

- Americas segment delivered Q4 revenue of $795.5 million, up 6.1% reported and 4.8% organic; non-residential grew high single digits, while residential declined high single digits.

- International segment Q4 revenue was $237.7 million, up 21.5% reported (driven by 16 points from acquisitions and 7.8 points from FX) and down 2.3% organically; segment margin expanded 90 bps.

- Fiscal 2026 guidance: total revenue growth of 5–7%, organic growth of 2–4%, and adjusted EPS of $8.70–$8.90 per share.

- 2025 capital allocation included ~$630 million of M&A, $175 million in dividends (12th consecutive increase), $80 million of share repurchases, and net debt/EBITDA of 1.6×.

- Q4 2025 EPS was $1.70 (up 3.0%) and adjusted EPS was $1.94 (up 4.3%); revenues were $1,033.2 M (+9.3% reported; +3.3% organic) with an operating margin of 20.3% (adjusted 22.4%)

- FY 2025 EPS was $7.44 (up 9.1%) and adjusted EPS was $8.14 (up 8.1%); revenues were $4,067.3 M (+7.8% reported; +4.1% organic) with an operating margin of 21.1% (adjusted 23.2%)

- Available cash flow for 2025 was $685.7 M (up 17.6%); year-end cash was $356.2 M, total debt $1,980.1 M, and Q4 dividend was $0.51 per share (~$44 M)

- 2026 outlook calls for reported revenue growth of 5–7% (organic 2–4%), adjusted EPS of $8.70–8.90, and available cash flow of 85–95% of adjusted net income

- Allegion posted Q4 EPS of $1.70 (+3.0%) and adjusted EPS of $1.94 (+4.3%) on revenues of $1,033.2 m (+9.3% reported, +3.3% organic); operating margin rose to 20.3% (adjusted 22.4%).

- Full-year 2025 EPS reached $7.44 (+9.1%) with adjusted EPS of $8.14 (+8.1%) on revenues of $4,067.3 m (+7.8% reported, +4.1% organic); adjusted operating margin was 23.2%.

- Available cash flow was $685.7 m (up 17.6%); year-end cash and equivalents stood at $356.2 m against $1,980.1 m of debt.

- For 2026, the company forecasts 5–7% reported revenue growth (2–4% organic), adjusted EPS of $8.70–$8.90, and available cash flow at 85–95% of adjusted net income.

- Allegion reported $3.8 billion in 2024 revenue, with an 80/20 split between the Americas and international segments.

- Since 2022, management has expanded operating margins by over 200 basis points while increasing R&D investment from 2.5% to over 3% of sales and completing 14 bolt-on acquisitions.

- The company sees continued mid-single-digit growth in non-residential markets, flat residential demand, and stable institutional segments, with commercial office showing early signs of recovery into 2026.

- Allegion’s unique spec-writing capability—one of only three global players—leverages an apprenticeship program and AI-enhanced tools to drive end-user demand, with 10-day lead times and revenue recognition spanning 9 months to 3 years post-specification.

- Adoption of electronic locks is accelerating in both residential and commercial sectors through partnerships with smartphone platforms and the launch of real-time connected locks enabling system integration in hours vs. months.

Quarterly earnings call transcripts for Allegion.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more