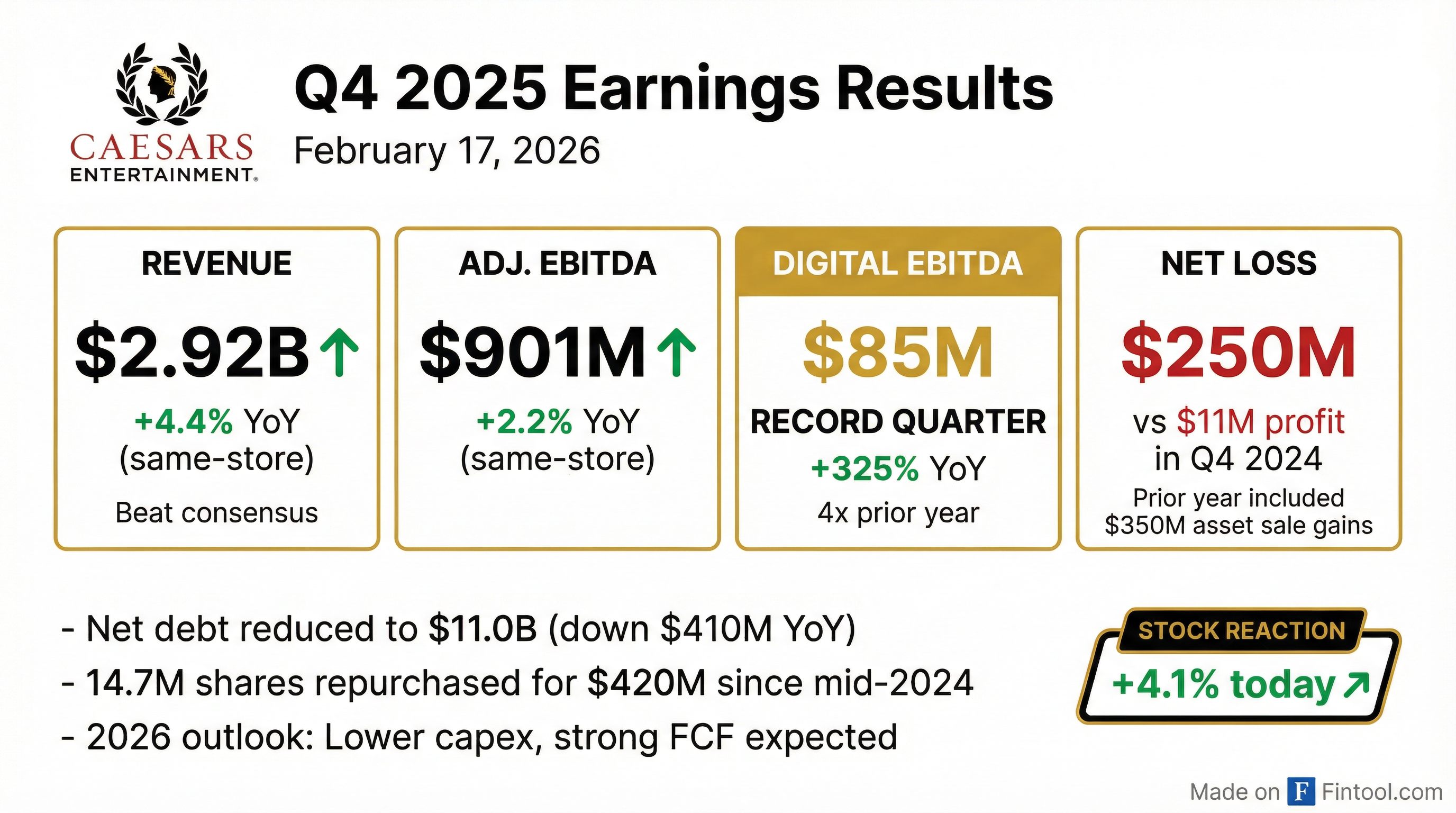

Earnings summaries and quarterly performance for Caesars Entertainment.

Executive leadership at Caesars Entertainment.

Thomas R. Reeg

Chief Executive Officer

Anthony L. Carano

President and Chief Operating Officer

Bret Yunker

Chief Financial Officer

Edmund L. Quatmann, Jr.

Chief Legal Officer

Gary L. Carano

Executive Chairman of the Board

Josh Jones

Chief Marketing Officer

Stephanie Lepori

Chief Administrative and Accounting Officer

Board of directors at Caesars Entertainment.

Bonnie S. Biumi

Director

Courtney R. Mather

Director

David P. Tomick

Lead Independent Director

Don R. Kornstein

Vice Chairman

Frank J. Fahrenkopf

Director

Jan Jones Blackhurst

Director

Jesse Lynn

Director

Kim Harris Jones

Director

Michael E. Pegram

Director

Ted Papapostolou

Director

Research analysts who have asked questions during Caesars Entertainment earnings calls.

Barry Jonas

Truist Securities

8 questions for CZR

Brandt Montour

Barclays PLC

8 questions for CZR

Daniel Guglielmo

Capital One

8 questions for CZR

David Katz

Jefferies Financial Group Inc.

8 questions for CZR

John DeCree

CBRE

8 questions for CZR

Jordan Bender

JMP Securities

8 questions for CZR

Steven Wieczynski

Stifel

8 questions for CZR

Chad Beynon

Macquarie

7 questions for CZR

Stephen Grambling

Morgan Stanley

7 questions for CZR

Lizzie Dove

Goldman Sachs

5 questions for CZR

Shaun Kelley

Bank of America Merrill Lynch

5 questions for CZR

Carlo Santarelli

Deutsche Bank

3 questions for CZR

Daniel Politzer

Wells Fargo

3 questions for CZR

Dan Politzer

Wells Fargo

3 questions for CZR

Steve Pizzella

Deutsche Bank

3 questions for CZR

Steven Pizzella

Jefferies

2 questions for CZR

Trey Bowers

Wells Fargo & Company

2 questions for CZR

Daniel Politzer

JPMorgan Chase & Co.

1 question for CZR

Joseph Greff

JPMorgan Chase & Co.

1 question for CZR

Samir Ghafir

Macquarie

1 question for CZR

Recent press releases and 8-K filings for CZR.

- Don Kornstein, Vice Chair, will retire effective December 31, 2025, after 12 years, and the board will shrink from 12 to 11 members

- Kornstein was instrumental in the Caesars–Eldorado merger and is praised for his strategic leadership

- The company reports a negative net margin of -2.12%, a high debt-to-equity ratio of 6.57, and an Altman Z-Score of 0.53, indicating financial distress

- Caesars’ stock has traded around $23.52 per share, down ~30% YTD and well below its 52-week high of $40

- Caesars Sportsbook mobile app and in-person betting are now live statewide in Missouri for residents aged 21+, with retail sportsbooks at Harrah’s Kansas City and Horseshoe St. Louis.

- The launch features the Universal Digital Wallet, enabling seamless deposits and withdrawals across Caesars’ digital platforms; Missouri is the first state to offer this capability from day one.

- Caesars is offering promotional welcome bonuses, including profit boost tokens and bonus bets for new users, plus a VIP Super Bowl weekend contest with luxury travel incentives.

- Despite its expansion, Caesars faces financial challenges, with a debt-to-equity ratio of 6.57, a current ratio of 0.78, a negative net margin of -2.12%, and an Altman Z-Score of 0.53 indicating financial distress.

- Everbay Capital calls the $2.75/share price for RemainCo inadequate at 1.1x EBITDA, and argues bundling this sale with the real estate transaction dramatically undervalues the assets.

- Everbay urges Golden’s board to provide detailed disclosures on valuation, sale process, and separate shareholder votes for the real estate and RemainCo transactions.

- The firm warns the go-shop period is too short to attract competitive bids, highlights a termination fee payable to CEO Blake Sartini, and objects to a voting agreement allowing him to vote his shares for a self-deal.

- Everbay notes the deal timing appears opportunistic—announced after Golden's stock hit a four-year low—and estimates shareholders could instead realize $42/share through an alternative two-step sale process.

- CEO Tom Reeg anticipates a recovery in Las Vegas visitation in Q4 2025 following a year of declining hotel occupancy and room rates.

- In Q3 2025, slot handle was down 2%, while hold percentage fell nearly 600 basis points, resulting in a year-over-year impact of >$30 million—the lowest hold in over three years.

- September 2025 marked the strongest month of Q3 for Caesars in Las Vegas, driven by robust group bookings that are projected to deliver a record EBITDA year in 2026.

- Caesars has realized over $1 billion in combined sales and cost synergies from its 2020 merger, equating to about a 30% increase in pro forma 2019 EBITDAR.

- Caesars posted consolidated Q3 net revenues of $2.9 billion and adjusted EBITDA of $884 million ($927 million hold-normalized).

- Digital segment delivered $311 million net revenue, $28 million adj EBITDA ($40 million hold-normalized); Las Vegas segment had same-store adj EBITDA of $379 million ($398 million hold-normalized) with 92% occupancy (-5 pp) and ADR down 5%; Regional segment achieved $506 million adj EBITDA ($517 million hold-normalized) on 6% net revenue growth.

- Redeemed $546 million of senior notes and repurchased $100 million of stock in Q3 (∼$400 million since mid-2024, share base -6%); nearest debt maturity in 2028; weighted average cost of debt ~6%; using free cash flow for debt reduction and buybacks.

- Outlook: expect sequential Q4 recovery in Las Vegas driven by strong group bookings (group mix to rise to 17%), targeting a record full-year 2025 Vegas EBITDA; Digital remains on track for long-term ~20% topline growth and 50% flow-through despite sports outcome volatility.

- Consolidated net revenues of $2.9 billion and adjusted EBITDA of $884 million (hold-normalized $927 million).

- Digital segment net revenue of $311 million with adjusted EBITDA of $28 million (hold-normalized $40 million); achieved 6% sports volume growth and 29% iCasino revenue growth despite low NFL hold and WSOP sale.

- Las Vegas segment same-store adjusted EBITDA of $379 million (hold-normalized $398 million) with 92% occupancy and 5% ADR decline; strong Q4 group bookings expected to drive a record EBITDA year in 2025.

- Regional segment adjusted EBITDA of $506 million (hold-normalized $517 million) on 6% net revenue growth; redeemed $546 million of senior notes and repurchased $100 million of stock in Q3, with debt maturing in 2028 at ~6% average cost.

- Q3 2025 net revenues grew 0.1% YoY while Adjusted EBITDA declined 11.2% YoY to $884 million, yielding a 30.8% margin on an unfavorable hold impact.

- On a hold-adjusted basis, net revenues rose 3.0% YoY and Adjusted EBITDA fell 4.4% YoY to $927 million.

- Caesars Digital net revenues increased 3% YoY, driven by a 24% rise in iGaming handle (net gaming revenue of $124 million) and a 6% increase in sports gaming handle; ARPMUP was $200 with 458,434 monthly unique payers (+15% YoY).

- For the trailing twelve months ending 9/30/2025, Caesars Digital delivered approximately $1.3 billion of net revenue and $171 million of Adjusted EBITDA, while total TTM Adjusted EBITDA was distributed as Owned $2,037 million, Leased $1,688 million, and Managed & Branded $68 million.

- Consolidated Q3 net revenue of $2.9 B, adjusted EBITDA of $884 M, and hold-normalized EBITDA of $927 M

- Las Vegas segment delivered same-store adjusted EBITDA of $379 M (hold-normalized $398 M), with 92% occupancy vs 97% LY and 5% ADR decline, and saw sequential improvement into Q4 driven by stronger group bookings

- Regional segment generated adjusted EBITDA of $506 M (hold-normalized $517 M) on 6% net revenue growth, with strategic marketing reinvestment improving margins

- Digital segment reported net revenue of $311 M, adjusted EBITDA of $28 M (hold-normalized $40 M), with 29% iCasino net revenue growth and monthly active payers up 15% to 460 K

- Balance sheet actions included $546 M senior note redemption, $100 M stock repurchase in Q3 (≈$400 M since mid-2024), with weighted-average cost of debt just over 6% and next maturity in 2028

- GAAP net revenues of $2.9 billion in Q3 2025, broadly flat YoY, and a net loss of $55 million vs. $9 million loss in Q3 2024.

- Same-store Adjusted EBITDA of $884 million, down 11.2% YoY; Caesars Digital Adjusted EBITDA was $28 million vs. $52 million a year ago.

- Cash and cash equivalents of $836 million and total debt of $11.9 billion (net debt $11.1 billion) as of September 30, 2025.

- Share buybacks: repurchased 3.9 million shares for $100 million in Q3; total 13.2 million shares for $391 million since mid-2024.

- CEO Tom Reeg expects improved Q4 performance driven by stronger Las Vegas occupancy and digital momentum.

- Caesars Entertainment is the first US operator to launch IGT’s “Kitty Glitter Grand™” simultaneously online and in-casino across New Jersey, Pennsylvania, Michigan, West Virginia and Ontario, with Tropicana joining pending approval.

- This exclusive launch reflects Caesars’ strategy to bridge digital and physical gaming to enhance customer engagement.

- Caesars reported Q2 2025 net revenue of $2.9 billion (up 2.9% YoY) and a net loss of $82 million.

- Caesars is partnering with Dry Creek Rancheria to develop the Caesars Republic Sonoma County integrated resort off Highway 101 above Alexander Valley Vineyards.

- CasinoTrac is enhancing its Nevada footprint with new installations of player management and loyalty systems at Barton’s Club 93 and Border Inn Casino.

Quarterly earnings call transcripts for Caesars Entertainment.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more