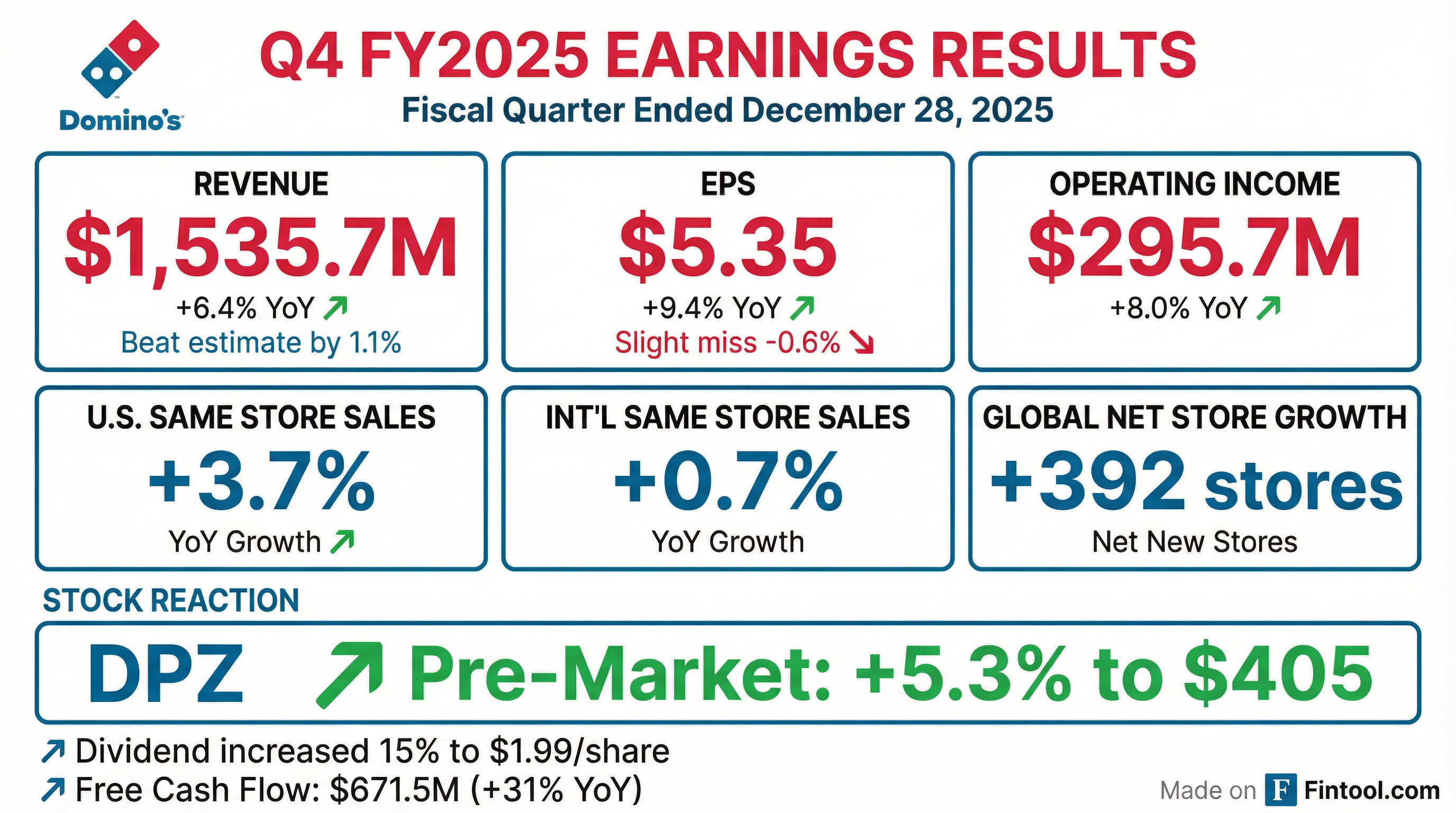

Earnings summaries and quarterly performance for DOMINOS PIZZA.

Executive leadership at DOMINOS PIZZA.

Russell J. Weiner

Chief Executive Officer

Cynthia A. Headen

Executive Vice President, Chief Supply Chain Officer

David A. Brandon

Executive Chairman

Frank R. Garrido

Executive Vice President, Chief Restaurant Officer

Joseph H. Jordan

Chief Operating Officer and President – Domino’s U.S.

Katherine E. Trumbull

Executive Vice President, Chief Marketing Officer

Kelly E. Garcia

Executive Vice President, Chief Technology and Data Officer

Kevin S. Morris

Executive Vice President, General Counsel and Corporate Secretary

Maureen S. Pittenger

Executive Vice President, Chief Human Resources Officer

Sandeep Reddy

Executive Vice President, Chief Financial Officer

Board of directors at DOMINOS PIZZA.

Andrew B. Balson

Director

C. Andrew Ballard

Presiding Director (Lead Independent Director)

Corie S. Barry

Director

Diane L. Cafritz

Director

James A. Goldman

Director

Patricia E. Lopez

Director

Richard L. Federico

Director

Stephen H. Kramer

Director

Research analysts who have asked questions during DOMINOS PIZZA earnings calls.

Brian Bittner

Oppenheimer & Co.

6 questions for DPZ

David Palmer

Evercore ISI

6 questions for DPZ

David Tarantino

Robert W. Baird & Co.

6 questions for DPZ

Dennis Geiger

UBS

6 questions for DPZ

John Ivankoe

JPMorgan Chase & Co.

6 questions for DPZ

Peter Saleh

BTIG

6 questions for DPZ

Danilo Gargiulo

AllianceBernstein

5 questions for DPZ

Sara Senatore

Bank of America

5 questions for DPZ

Brian Harbour

Morgan Stanley

4 questions for DPZ

Gregory Francfort

Guggenheim Securities

4 questions for DPZ

Jeffrey Bernstein

Barclays

4 questions for DPZ

Jeffrey Farmer

Gordon Haskett Research Advisors

4 questions for DPZ

Jon Tower

Citigroup

4 questions for DPZ

Alexander Slagle

Jefferies

3 questions for DPZ

Andrew Charles

TD Cowen

3 questions for DPZ

Christine Cho

Goldman Sachs Group

3 questions for DPZ

Christopher O'Cull

Stifel, Nicolaus & Company

3 questions for DPZ

Lauren Silberman

Deutsche Bank

3 questions for DPZ

Andrew Strelzik

BMO Capital Markets

2 questions for DPZ

Jeff Farmer

Gordon Haskett

2 questions for DPZ

Logan Reich

RBC Capital Markets

2 questions for DPZ

Patrick

Wolfe Research

2 questions for DPZ

Brian Mullan

Piper Sandler

1 question for DPZ

Chris O'cull

Stifel Financial Corp

1 question for DPZ

Danilo Geiger

Bernstein

1 question for DPZ

Gregory Francort

Guggenheim

1 question for DPZ

James Salera

Stephens Inc.

1 question for DPZ

Todd Brooks

The Benchmark Company

1 question for DPZ

Zachary Fadem

Wells Fargo

1 question for DPZ

Recent press releases and 8-K filings for DPZ.

- Shares of Domino’s Pizza jumped 17%–23% before a trading halt after reports Bain Capital is considering a A$4 billion takeover bid.

- The potential bid implies a 100%+ premium over Domino’s current market valuation of ~A$1.46 billion; no official offer has been made and neither party has commented.

- Domino’s reported FY sales down 0.9% to A$4.15 billion and earnings down 4.6% to A$198.1 million, contributing to its depressed share price.

- Founder Jack Cowin is transitioning to executive chair as part of leadership changes aimed at stabilizing fundamentals.

- Global market estimated at US$17.5 B in 2024, projected to US$22.1 B by 2030 at a 4.0% CAGR from 2024–2030.

- Rapid expansion driven by ghost kitchens and delivery-only models, with initial franchise investments under USD 30,000 and breakeven in 12–18 months.

- Operational efficiency through simplified menus, compact outlets (300–500 sq ft) with 3–5 employees per shift, and centralized digital ordering and procurement.

- Growth accelerated by partnerships with food aggregators, expansion into non-traditional locations, and digital engagement of Millennials and Gen Z consumers.

- U.S. retail sales grew 7%, driven by 5.2% same-store sales and net addition of 29 stores, bringing the U.S. system to 7,090 units. International retail sales rose 5.7% ex-FX, with 185 net new stores and 1.7% same-store sales.

- Key growth drivers included the Best Deal Ever promotion and Parmesan Stuffed Crust Pizza, while the full Q3 rollout on DoorDash supported a 2.5% delivery comp increase.

- Completed refinancing of approximately $1 billion of debt in two $500 million tranches at a blended 5.1% rate, and repurchased 166,000 shares for $75 million, leaving $540 million remaining under the repurchase authorization.

- For 2025, global retail sales are expected in line with 2024, with U.S. same-store sales of 3%, international same-store sales of 1–2%, about 175 net new U.S. stores, and operating income growth of 8% (ex-FX).

- Launched the first brand refresh in 13 years under the “Hungry for More” identity, went live with the new website and mobile web, and plans app rollouts by year-end to enhance digital ordering.

- Global retail sales grew 6.3%, with U.S. same-store sales up 5.2% and international same-store sales up 1.7% in Q3 2025.

- Total revenues rose 6.2% to $1,147.1 M, driving income from operations up 12.2% to $223.2 M (11.8% ex-FX).

- Net income declined 5.2% to $139.3 M, yielding diluted EPS of $4.08 versus $4.19 a year ago.

- Free cash flow increased 31.8% to $495.6 M for the first three quarters, and the leverage ratio improved to 4.5x from 4.9x.

- Total revenues rose 6.2% to $1,147.1 million, while net income fell 5.2% to $139.3 million and EPS declined 2.6% to $4.08

- Global retail sales growth of 6.3% with U.S. same store sales +5.2% and international same store sales +1.7% (ex-FX)

- Net store growth of 214 stores in Q3, including 29 in the U.S. and 185 internationally

- Declared a $1.74 quarterly dividend; repurchased 165,778 shares for $74.7 million; completed $1 billion refinancing via 5- and 7-year notes

- Johnson Fistel, PLLP is investigating potential securities law violations by Domino’s Pizza officers and directors following a class action lawsuit alleging materially false and misleading statements about the company’s business and prospects.

- The complaint alleges the company’s largest master franchisee, DPE, faced significant challenges with new store openings and closures, making it unlikely Domino’s would meet its previously issued long-term guidance for annual global net store growth.

- Plaintiffs claim these misstatements overstated Domino’s business and financial prospects and seek recovery of funds, corporate governance changes, and court-approved incentive awards at no cost.

- Reported a strategic reset in FY25 with total network sales slightly down and same-store sales falling 0.2% overall.

- Underlying EBIT declined 4.6% and a statutory net loss of A$3.7 million was recorded.

- Full-year dividend cut of about 27% to 77 cents per share, including a final unfranked dividend of 21.5 cents.

- Leadership change as Jack Cowin assumed the role of Executive Chair following the departure of the previous CEO.

- Launched a cost efficiency program to reinvest savings into marketing, franchisee support, and digital capabilities.

- Purchase Agreement: On August 12, 2025, Domino’s Pizza Master Issuer LLC and its Co-Issuers agreed with Barclays Capital Inc. and Guggenheim Securities, LLC to issue $500 million of 4.930% Series 2025-1 Class A-2-I notes (5-year) and $500 million of 5.217% Series 2025-1 Class A-2-II notes (7-year).

- Exempt Offering: The notes will be sold in a transaction exempt from registration under the Securities Act of 1933, with closing expected on September 5, 2025, subject to customary conditions.

- Documentation: The Purchase Agreement, which includes standard representations, warranties, covenants and indemnification provisions, is filed as Exhibit 99.1.

- The company plans to issue $1.0 billion of new securitized notes and use $150 million of cash on hand to repay $742.0 million of 2015-1 Class A-2-II notes, $402.7 million of 2018-1 Class A-2-I notes and all outstanding 2021-1 and 2022-1 variable funding notes at par.

- It expects to establish a new $320 million variable funding note facility to replace the existing $200 million 2021-1 and $120 million 2022-1 facilities.

- As of June 15, 2025, outstanding letters of credit totaled $56.4 million and there were no borrowings under the current variable funding facilities.

- The refinancing is subject to market conditions and is anticipated to close in Q3 2025.

- Total revenue rose 4.3% to $1.145 billion in Q2 2025

- Income from operations increased 14.8% to $225 million, but net income fell 7.7% to $131.1 million and EPS declined to $3.81

- Same-store sales grew 3.4% in the U.S. and 2.4% internationally

- Effective tax rate rose from 15% to 22.1%, weighing on profitability

Quarterly earnings call transcripts for DOMINOS PIZZA.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more