Earnings summaries and quarterly performance for General Motors.

Executive leadership at General Motors.

Mary Barra

Chief Executive Officer

Grant Dixton

Executive Vice President, Chief Legal, Public Policy Officer and Corporate Secretary

Mark Reuss

President

Paul Jacobson

Executive Vice President and Chief Financial Officer

Rory Harvey

Executive Vice President and President, Global Markets

Board of directors at General Motors.

Al Kelly

Director

Devin Wenig

Director

Jami Miscik

Director

Jan Tighe

Director

Joanne Crevoiserat

Director

Jon McNeill

Director

Joseph Jimenez

Director

Mark Tatum

Director

Patricia Russo

Independent Lead Director

Wesley Bush

Director

Research analysts who have asked questions during General Motors earnings calls.

Dan Levy

Barclays PLC

8 questions for GM

Emmanuel Rosner

Wolfe Research

8 questions for GM

Ryan Brinkman

JPMorgan Chase & Co.

7 questions for GM

Adam Jonas

Morgan Stanley

6 questions for GM

Itay Michaeli

TD Cowen

6 questions for GM

Joseph Spak

UBS Group AG

6 questions for GM

Mark Delaney

The Goldman Sachs Group, Inc.

6 questions for GM

Chris McNally

Evercore ISI

4 questions for GM

Michael Ward

Citi Research

4 questions for GM

James Picariello

BNP Paribas

3 questions for GM

John Murphy

Bank of America

3 questions for GM

Andrew Percoco

Morgan Stanley

2 questions for GM

Colin Langan

Wells Fargo & Company

2 questions for GM

Daniel Roeska

Bernstein Research

2 questions for GM

Federico Merendi

Bank of America

2 questions for GM

Joe Spak

UBS Group AG

2 questions for GM

Mike Ward

UBS

2 questions for GM

Tom Narayan

RBC Capital Markets

2 questions for GM

Edison Yu

Deutsche Bank

1 question for GM

Gautam Narayan

RBC Capital Markets

1 question for GM

Recent press releases and 8-K filings for GM.

- Stable start to 2026 marked by resilience against weather disruptions and manageable $3 billion–$4 billion in U.S. tariffs; capital allocation priorities remain investing in the business, maintaining a strong balance sheet, and returning cash to shareholders via balanced share buybacks.

- Implemented 30%–40% reduction in inventory levels, driving approximately $3 billion–$4 billion of incremental cash performance and achieving vehicle incentives roughly 200 basis points below the industry average.

- Announced $5 billion of onshoring investments to expand U.S. manufacturing capacity—bolstering domestic production, mitigating geopolitical risks, and balancing higher labor costs against tariff exposure.

- Advancing EV profitability through LFP battery technology and disciplined demand management (current EV penetration ~5%–7%); expanding digital and software services with growing deferred revenue streams at software-company-like margins.

- GM expects $3–4 billion in tariffs for 2026, a level deemed manageable and projected to decline as new U.S. capacity comes online.

- Inventory discipline has cut discounting by ~200 bps vs. the industry average, translating into $3–4 billion of incremental cash flow.

- Committed $5 billion to U.S. onshoring for next-gen V8 and assembly, balancing tariff savings against higher labor costs (≈ $1 000/vehicle) and reducing geopolitical supply-chain risk.

- EV penetration is stabilizing at 5–7% post-IRA credits, with a shift from volume to profitability; LMR battery technology is set to reduce pack costs by thousands per vehicle.

- Building high-margin recurring revenue via software & services (deferred revenue on SDV 2.0), while shares remain undervalued, supporting ongoing buybacks.

- GM CFO Paul Jacobson described 2026 as a stable year, with early-year challenges from weather and tariffs but reaffirmed that $3–4 billion of tariffs remain manageable and domestic capacity additions will help lower costs.

- The company has cut inventory by 30–40%, driving a $3–4 billion improvement in cash performance and maintaining discounts about 200 basis points below industry averages.

- Capital priorities remain heavy investment in the business, a strong balance sheet and returning cash via share buybacks—GM still views its stock as undervalued despite recent multiple uplifts.

- EV profitability is being addressed through cost reductions, notably using LMR prismatic cells to save thousands per pack, and by resetting demand expectations in a more rational incentive environment.

- GM is expanding software and services revenue—deferred revenue is growing via OnStar and the upcoming Software-Defined Vehicle 2.0 rollout, targeting higher-margin streams beyond vehicle sales.

- GM reduced inventory to 48 days, boosting free cash flow from ~$3 bn to $10 bn annually over the last 4–5 years.

- Despite $3 bn of tariff headwinds in 2025 and another $3–4 bn expected in 2026, North America margins returned to 8–10% about 12–18 months ahead of investor expectations.

- GM took $7 bn of charges in H2 2025 to right-size EV production capacity for ~8–12% adoption, leading to a more sustainable EV ramp.

- Announced $5 bn of U.S. onshoring investments by 2027, enabling domestic production of nearly 2 million vehicles to mitigate tariff impact.

- Developing its software-defined vehicle platform, targeting $7.5 bn of deferred revenue from Super Cruise, OnStar, and future digital services.

- GM absorbed >$3 billion in tariffs in 2025 and signals $3–4 billion in 2026, yet restored 8 %–10 % North America margins 12–18 months ahead of expectations.

- Took $7 billion of charges in H2 2025 on EV tooling for a 1 million VE/year capacity, realigning investments to match 8 %–12 % consumer EV adoption.

- Committed $5 billion of U.S. onshoring investments by 2027 to produce ~2 million vehicles and convert the Orion plant from EV to ICE to mitigate tariff exposure.

- Grew software and services with $7.5 billion of deferred revenue; Super Cruise and OnStar expansion will pave the way for hands-off autonomy by 2028.

- Expects a $1 billion–$2 billion regulatory tailwind in 2026 from EPA and CAFE rollbacks, while rolling out Gen 6 V8 engines—the most efficient V8s to date.

- GM delivered a strong 2025 with North America operating margins restored to 8%–10%—12–18 months ahead of investor expectations—despite absorbing $3 billion in tariffs and guiding for $3–4 billion in 2026.

- Inventory discipline reduced stock to 48 days (targeting 50–60 days), while annual free cash flow surged from $3 billion historically to about $10 billion, creating a buffer for future volatility.

- The company took $7 billion of EV-related charges in H2 2025 to right-size production capacity, aligning with a more measured EV adoption curve and driving cost reduction efforts in battery architecture.

- Announced $5 billion of onshoring investments by 2027, including retooling the Orion plant to ICE production, to mitigate long-term tariff impacts and support nearly 2 million U.S.-made vehicles annually.

- Emphasis on software and services growth: GM has built deferred revenue to $7.5 billion, expanding Super Cruise and paving the way for hands-off autonomy and a software-defined vehicle roadmap.

- Six DMD development projects are active, targeting 2027 volume production (SOP) in China and Europe on interior permanent-magnet synchronous motors, with plans to expand to external-rotor synchronous motors thereafter.

- In Q4 2025, a global tier-1 supplier completed DMD testing ahead of schedule; a Chinese OEM trial could enable remote wireless software upgrades by Q4 2026.

- In January 2026, a European OEM finished bench testing validating DMD’s real-world efficiency gains; two more OEMs are poised to begin trials by mid-2026.

- CEO John Fuller notes that software integration of DMD can deliver 0.5–1% energy-efficiency improvement on in-board permanent-magnet motors, with vehicle tests matching lab outcomes.

- Mitra EV secured $27 million in financing, comprising equity from Ultra Capital and a credit facility from S2G Investments to expand its capital-efficient fleet electrification platform.

- The funding will accelerate deployment of no-upfront-cost EV leasing (including GM, Ford, and Mercedes-Benz vehicles), dedicated overnight charging, and a shared DC fast-charging hub network aimed at serving 99% of U.S. fleet operators.

- The fully managed solution delivers immediate up to 75% operating cost reductions for commercial fleets by combining lower fueling costs and reduced maintenance.

- Proceeds will support expansion of shared charging infrastructure, additional fleet solutions, and entry into new markets.

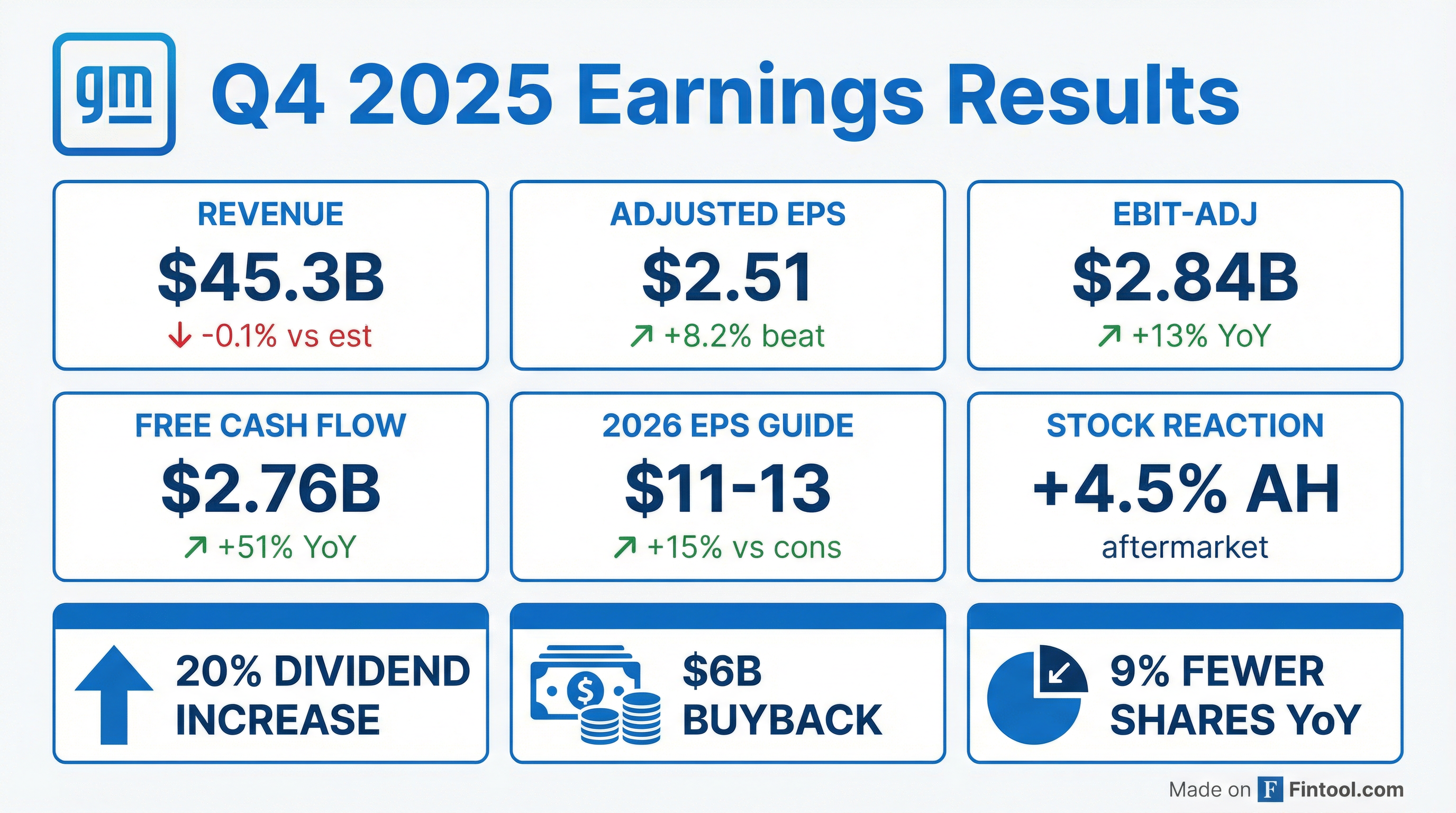

- GM delivered Q4 revenue of $45 B (–5% y/y), EBIT adj $2.8 B, EPS dil adj $2.51, and adj automotive FCF $2.8 B.

- Full-year 2025 results included EBIT adj $12.7 B, adj automotive FCF $10.6 B, year-end cash $21.7 B, 60 bps market share gain, and 54% total shareholder return.

- Capital returns: Q4 share repurchases of $2.5 B (33 M shares), $6 B total in 2025; board authorized an additional $6 B repurchase and raised the dividend 20% to $0.18.

- 2026 guidance: EBIT adj $13–15 B, EPS adj $11–13, adj automotive FCF $9–11 B, gross tariffs $3–4 B, targeting 8–10% North America margins.

- GM delivered $12.7 billion of adjusted EBIT and $10.6 billion of adjusted automotive free cash flow in 2025, ending with $21.7 billion in cash; the stock returned 54% to investors.

- GM achieved its highest U.S. market share in a decade in 2025, marking four consecutive years of share gains, and led the industry in full-size pickups and SUVs with award-winning models like the Cadillac Escalade IQ.

- GM recorded $7.6 billion of EV-related charges in Q3 and Q4 2025 to right-size its EV capacity—comprising impairments and contractual settlements—and expects significantly lower EV losses and cash outflows in 2026.

- For 2026, GM guides adjusted EBIT of $13–15 billion, adjusted EPS of $11–13 per share, and free cash flow of $9–11 billion, targets North America margins of 8–10%, and raised its quarterly dividend by 20%.

Fintool News

In-depth analysis and coverage of General Motors.

GM CFO Jacobson at Citi: 'Bet on Execution'—Tariff Playbook, $10B Cash Flow, and the Case for a Re-Rating

GM CFO Says Automaker Returning to 8-10% Margins 'Ahead of Expectations' Despite $3B+ Tariff Hit

GM Takes $7.2 Billion EV Charge, Rewards Shareholders with $6 Billion Buyback

Trump Raises Tariffs on South Korea to 25%, Hammering Auto Stocks

FTC Slaps GM with 20-Year Consent Order After OnStar Data Scandal

GM Takes $7.6 Billion EV Hit—Detroit's Second Massive Retreat in a Month

Quarterly earnings call transcripts for General Motors.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more