Palo Alto Networks (PANW)·Q2 2026 Earnings Summary

Palo Alto Networks Beats on Revenue and EPS, Stock Falls 6% on CyberArk Dilution

February 17, 2026 · by Fintool AI Agent

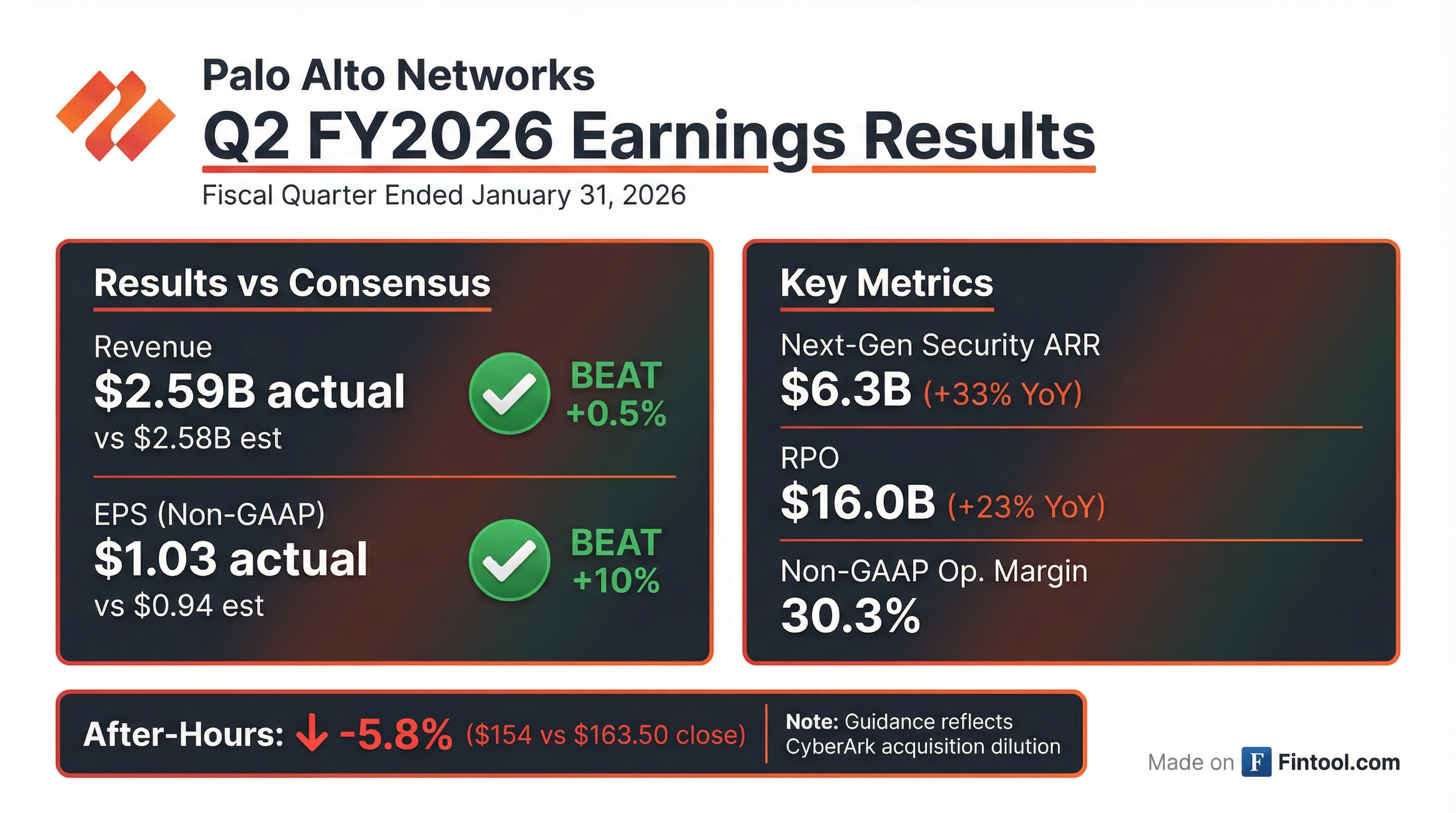

Palo Alto Networks reported Q2 FY2026 results that beat on both revenue and earnings, extending its quarterly beat streak to eight. Revenue grew 15% year-over-year to $2.59 billion, while non-GAAP EPS of $1.03 exceeded consensus by nearly 10%. Despite the strong results, shares fell 5.8% after-hours to $154 as Q3 EPS guidance came in light due to dilution from the recently closed CyberArk acquisition.

Did Palo Alto Networks Beat Earnings?

Yes — PANW delivered a double beat with solid outperformance on EPS:

This marks PANW's eighth consecutive quarter of beating both revenue and EPS estimates.

Year-Over-Year Performance

What Are the Key Growth Metrics?

PANW's platform transformation continues to accelerate, with Next-Generation Security ARR and RPO showing strong momentum:

This represents the third consecutive quarter with non-GAAP operating margins above 30%, demonstrating strong operating leverage.

What Did Management Say?

CEO Nikesh Arora emphasized accelerating platformization driven by AI:

"We saw continued strength in platformizations, a trend that is accelerating due to AI - customers are keen to both modernize and normalize their cybersecurity stack, aligning them to our approach. We also saw steady and strong adoption of AI security, which we expect will be a long term trend."

CFO Dipak Golechha highlighted the integration of recent acquisitions:

"We once again delivered strong top-line growth, complimented by operating efficiency, with our third straight quarter of 30%-plus non-GAAP operating margins. We are deploying the same playbook of operational excellence that has guided Palo Alto Networks the last several years across CyberArk and Chronosphere."

The mention of welcoming "employees of Chronosphere and CyberArk" signals these acquisitions have closed and integration is underway.

What Did Management Guide?

Q3 FY2026 Guidance

Critical detail: Q3 EPS guidance uses 812-817 million shares outstanding, up from 711 million in Q2. This ~14% dilution from the CyberArk acquisition is the primary driver of the lower sequential EPS guidance.

Full Year FY2026 Guidance

How Did the Stock React?

The stock declined despite the earnings beat, reflecting investor concern about:

- Dilution from CyberArk: Share count increasing ~14% weighs on per-share metrics

- Q3 EPS guidance: $0.78-$0.80 looks weak vs. Q2's $1.03 (though apples-to-oranges due to share count)

- Integration execution risk: Two major acquisitions (CyberArk, Chronosphere) create near-term uncertainty

What Changed From Last Quarter?

Key developments since Q1:

- CyberArk and Chronosphere acquisitions closed

- Third consecutive quarter of 30%+ operating margins

- AI security adoption highlighted as "long-term trend"

Revenue Breakdown

Subscription and support revenue now represents 80% of total revenue, highlighting the successful transition to recurring revenue.

Balance Sheet Highlights

The $2.4B increase in goodwill reflects the CyberArk acquisition. Cash increased substantially, partially offset by a decrease in investments.

Forward Catalysts

- CyberArk/Chronosphere Integration: Execution on "operational excellence playbook" will be key in coming quarters

- AI Security Adoption: Management sees this as a "long-term trend" — watch for product announcements

- Next-Gen Security ARR: Guided to $7.94-7.96B next quarter (+56% YoY) — suggests platformization momentum continues

- Q3 FY2026 Earnings: Scheduled for mid-May 2026 — first full quarter with CyberArk contribution

Key Risks

- Integration Risk: Absorbing two acquisitions simultaneously creates execution challenges

- Dilution Impact: 14% higher share count will pressure per-share metrics through FY2026

- Valuation: At ~$114B market cap, stock trades at premium multiples requiring continued growth

Earnings call transcript not yet available. This analysis is based on the 8-K filing and earnings press release.