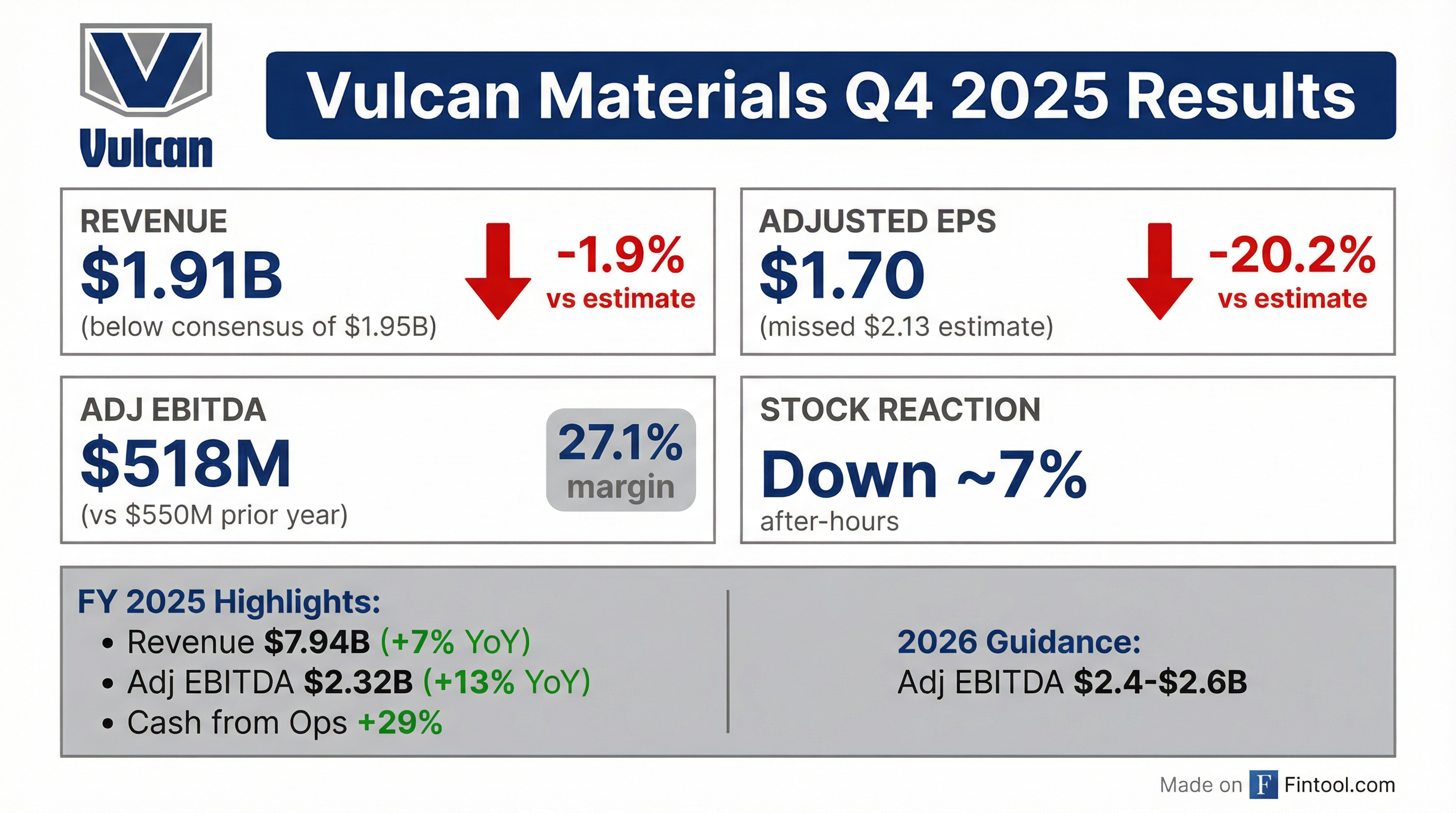

Earnings summaries and quarterly performance for Vulcan Materials.

Executive leadership at Vulcan Materials.

Board of directors at Vulcan Materials.

Cynthia L. Hostetler

Director

David P. Steiner

Director

George A. Willis

Director

James T. Prokopanko

Director

Kathleen L. Quirk

Director

Lee J. Styslinger, III

Director

Lydia H. Kennard

Director

Melissa H. Anderson

Director

O. B. Grayson Hall, Jr.

Independent Lead Director

Richard T. O’Brien

Director

Thomas A. Fanning

Director

Research analysts who have asked questions during Vulcan Materials earnings calls.

Garik Shmois

Loop Capital Markets

7 questions for VMC

Kathryn Thompson

Thompson Research Group

7 questions for VMC

Michael Dudas

Vertical Research Partners

7 questions for VMC

Trey Grooms

Stephens Inc.

7 questions for VMC

Angel Castillo Malpica

Morgan Stanley

5 questions for VMC

David Macgregor

Longbow Research

5 questions for VMC

Keith Hughes

Truist Financial Corporation

5 questions for VMC

Steven Fisher

UBS

5 questions for VMC

Timna Tanners

Wolfe Research

5 questions for VMC

Ivan Yi

Wolfe Research, LLC

4 questions for VMC

Tyler Brown

Raymond James Financial, Inc.

4 questions for VMC

Adam Thalhimer

Thompson, Davis & Company, Inc.

3 questions for VMC

Andrew Maser

Stifel Financial Corp.

3 questions for VMC

Asher Sohnen

Citigroup Inc.

3 questions for VMC

Jerry Revich

Goldman Sachs Group Inc.

3 questions for VMC

Michael Feniger

Bank of America

3 questions for VMC

Philip Ng

Jefferies

3 questions for VMC

Angel Castillo

Morgan Stanley & Co. LLC

2 questions for VMC

Anthony Pettinari

Citigroup Inc.

2 questions for VMC

Asher Sohnen

Citigroup

2 questions for VMC

Brian Brophy

Stifel Financial Corp

2 questions for VMC

Jesse Barone

Jefferies Financial Group Inc.

2 questions for VMC

Michael Dahl

RBC Capital Markets

2 questions for VMC

Adam Falheimer

Thompson Davis

1 question for VMC

Adrian Huerta

JPMorgan Chase & Co.

1 question for VMC

Brent Thielman

D.A. Davidson

1 question for VMC

Jean Veliz

D.A. Davidson Companies

1 question for VMC

Joe Nolan

Longbow Research

1 question for VMC

Patrick Brown

Raymond James

1 question for VMC

Recent press releases and 8-K filings for VMC.

- CEO Ronnie Pruitt outlined a two-pronged strategy—enhancing the core via the Vulcan Way of Selling and Operating, and expanding reach through M&A and greenfield projects—to solidify its industry leadership in aggregates.

- The company reported $11.33 cash gross profit per ton in 2025, a 45% increase since 2022, on shipments of 227 million tons.

- Since the 2022 Investor Day, Vulcan has added 36 aggregate operations and completed 7 greenfield projects, and is pursuing a pipeline of 350 million annual sales tons, including opportunities outside its current footprint.

- CFO Mary Andrews Carlisle highlighted a 1.8x net leverage, $1.1 billion free cash flow in 2025, and a balanced capital allocation approach; management sees a path to $20 per ton cash gross profit, implying $4.5–$5.0 billion adjusted EBITDA organically.

- Management anticipates low single-digit demand growth, driven by public infrastructure and private non-residential markets, supporting high single- to low double-digit improvements in unit profitability.

- Vulcan delivered $11.33 per ton of aggregates cash gross profit in 2025 and now targets $20 per ton on 260–270 million tons through enhanced pricing and cost controls.

- Achieved a 13% CAGR in adjusted EBITDA and 16% in operating cash flow over the past three years, with operating cash flow exceeding $1.8 billion and free cash flow surpassing $1.1 billion in 2025.

- Executes a two-pronged growth strategy: enhancing core operations via the Vulcan Way of Operating & Selling and expanding reach with 36 aggregate acquisitions, seven greenfield projects, and divestiture of 149 ready-mix plants in the past 3.5 years.

- Maintains disciplined capital allocation—O&M capex at 6–6.5% of revenue, growth capex at 1–4%, net leverage at 1.8×, and nearly $6 billion deployed over three years to support M&A and shareholder returns.

- Vulcan Materials achieved $11.33 cash gross profit per ton on 227 million tons shipped in 2025, driving over $2.3 billion adjusted EBITDA.

- Announced medium-term target of $20 cash gross profit per ton on 260–270 million tons, translating to $4.5–5.0 billion adjusted EBITDA (organic), with M&A upside.

- Reaffirmed two-pronged strategy to enhance the core via Vulcan Way of Selling and Operating and expand reach through M&A and greenfield investments, completing 36 acquisitions and 7 greenfields since 2022.

- Free cash flow surpassed $1.1 billion in 2025; net leverage at 1.8x, supporting 6–6.5% revenue capex, ongoing acquisitions, and increased dividends & share buybacks.

- Positioned in 23 states with 90% of revenue from #1 or #2 markets and 16.5 billion tons of reserves, targeting 350 million sales tons for future expansion.

- Vulcan reported 425 aggregates operations generating $7.9 B revenue and $2.3 B Adjusted EBITDA in 2025, with a 1.9× Total Debt/TTM EBITDA ratio as of December 31, 2025.

- The company achieved a 45% increase in Aggregates Cash Gross Profit per ton since 2022, reaching $11.33/ton, meeting its $11–12/ton target despite muted demand.

- Strategic initiatives include the Vulcan Way of Selling & Operating, driving +10% price growth vs. peers, alongside $3 B in acquisitions and $1.5 B in divestitures since 2022 to optimize its footprint.

- Vulcan’s strong balance sheet features 1.8× Net Debt/EBITDA, 5.0% weighted average interest rate, and 13.7 years average debt maturity, supporting $707 M in share repurchases over the past three years.

- FY 2025 total revenues of $7,941 M, up 7% year-over-year.

- FY 2025 Adjusted EBITDA of $2,324 M, up 13%, with margin expanding to 29.3% (+160 bps).

- Aggregates segment: volume +3%, mix-adjusted pricing +6%, delivering cash gross profit per ton of $11.33 (+7%).

- Operating cash flow of $1.8 B, up 29%; capital returned via $438 M in share repurchases and $260 M in dividends.

- 2026 outlook: aggregates volume growth of 1–3%, pricing up 4–6%, and Adjusted EBITDA of $2.4–2.6 B.

- In 2025, Adjusted EBITDA of $2.3 billion represented a 13% increase and margin expansion of 160 bps to 29.3%.

- Aggregate shipments reached 227 million tons (+3%), with cash gross profit per ton of $11.33, hitting target levels despite same-store volume softness.

- The company generated over $1.8 billion of operating cash flow (+29%) and free cash flow up 40% after $678 million of CapEx, returning $260 million in dividends and $438 million in share repurchases; net debt/EBITDA ended at 1.8x.

- 2026 guidance forecasts aggregate volume growth of 1–3%, price increases of 4–6%, low-single-digit cost inflation, and Adjusted EBITDA of $2.4–2.6 billion, with CapEx of $750–800 million.

- Adjusted EBITDA of $2.3 billion in FY 2025, up 13% year-over-year, with margin expansion of 160 bps to 29.3%

- Aggregates shipments of 227 million tons, +3% (driven by acquisitions; same-store volumes slightly below prior year), and cash gross profit per ton up 7% to $11.33

- Generated $1.8 billion in operating cash flow (+29%), returned $260 million via dividends and $438 million through share repurchases; net debt/EBITDA at 1.8× after $2 billion of note issuance and $550 million commercial paper repayment

- 2026 outlook: Adjusted EBITDA of $2.4–2.6 billion; aggregates shipments growth of 1–3%, selling prices +4–6%, unit costs up low single-digit; CapEx of $750–800 million

- Vulcan delivered $2.3 billion Adjusted EBITDA in 2025, a 13% increase over prior year, with margin expansion to 29.3%, operating cash flow of over $1.8 billion, and 227 million tons of aggregate shipments (+3%).

- Achieved $11.33 cash gross profit per ton in aggregates, driving >40% free cash flow growth after $678 million of CapEx, reducing leverage to 1.8× net debt/EBITDA, and returning $698 million to shareholders via $260 million of dividends and $438 million of share repurchases.

- 2026 guidance calls for aggregate shipments to grow 1–3%, freight-adjusted ASP up 4–6%, unit cash costs up low single-digits, resulting in high single-digit growth in cash gross profit per ton and $2.4–2.6 billion of Adjusted EBITDA; CapEx of $750–800 million.

- Demand outlook underpinned by continued public infrastructure spending (IIJA tail, highway starts +24% in Vulcan markets), a robust data center pipeline (>150 million sq ft under construction), and modest private non-residential growth, while single-family housing activity remains subdued.

- Vulcan saw FY 2025 revenues of $7.94 billion (+7%) and Q4 revenues of $1.91 billion.

- Adjusted EBITDA grew 13% to $2.324 billion, with margin expansion to 29.3% in 2025 from 27.7% in 2024.

- Operating cash flow rose 29% to $1.8 billion, capital expenditures were $703 million, and $698 million was returned to shareholders via $438 million of buybacks and $260 million of dividends.

- Net debt/Adjusted EBITDA was 1.8× at year-end and total debt/EBITDA was 1.9×, reflecting strong leverage metrics.

- 2026 outlook: $2.4 billion to $2.6 billion of Adjusted EBITDA, with aggregates shipments up 1–3% and price growth of 4–6%.

- Total revenues of $1.913 billion in Q4 (+3% YoY) and $7.941 billion for FY 2025 (+7% YoY).

- Adjusted EBITDA of $518 million in Q4 (27.1% margin) and $2.324 billion for FY 2025 (29.3% margin), with net earnings of $252 million in Q4 and $1.077 billion for the year.

- Operating cash flow rose 29% to $1.8 billion; full-year capital expenditures were $703 million, with $438 million returned via share repurchases and $260 million in dividends.

- Aggregates shipments of 55.1 million tons in Q4 (+2% YoY) and 226.8 million tons for FY 2025 (+3% YoY), delivering full-year cash gross profit per ton of $11.33 (+7% YoY).

- 2026 outlook: expects Adjusted EBITDA of $2.4–$2.6 billion, shipments up 1–3%, price improvement of 4–6%, SAG expense of $580–$590 million and capex of $750–$800 million.

Quarterly earnings call transcripts for Vulcan Materials.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more