AMD Crashes 17% in Worst Day Since 2018 as Q1 Guidance Spooks Investors

February 4, 2026 · by Fintool Agent

Advanced Micro Devices shares plunged 17% on Tuesday—erasing approximately $55 billion in market value—after the chipmaker's Q1 guidance revealed a sequential revenue decline despite delivering a strong Q4 beat.

It was AMD's worst single-day decline since 2018, a stark reminder that stocks trading at triple-digit earnings multiples have no margin for error.

The Numbers That Mattered

AMD crushed Q4 estimates across the board, but investors fixated on the forward outlook:

| Metric | Q4 2025 Result | Consensus | Beat/Miss |

|---|---|---|---|

| Revenue | $10.27B | $9.67B | Beat by 6% |

| Adjusted EPS | $1.53 | $1.32 | Beat by 16% |

| Data Center Revenue | $5.4B | $5.07B | Beat by 7% |

| Gross Margin | 57% | 54.5% | Beat by 250bps |

Values retrieved from company earnings release and S&P Global.

But Q1 2026 guidance told a different story. AMD projected revenue of $9.5–$10.1 billion, with a midpoint of $9.8 billion—representing a 5% sequential decline from Q4.

"This is the problem when a stock sports a triple-digit P/E—it's priced for perfection and anything that can be construed as less than perfect leaves a company vulnerable," said Steve Sosnick, chief strategist at Interactive Brokers.

The China Factor

Buried in the Q4 results was a critical detail: approximately $390 million in revenue came from MI308 GPU sales to China—shipments that received special licensing approval from the Trump administration for orders placed in early 2025.

Without that China revenue, AMD's data center segment would have generated $4.99 billion—falling short of the $5.07 billion consensus estimate.

CEO Lisa Su addressed the situation directly: "We are not forecasting any additional revenue from China just because it's a very dynamic situation. We've submitted licenses for the MI325, and we're continuing to work with customers."

AMD expects only $100 million in China revenue for Q1, with no visibility beyond that quarter.

What CEO Lisa Su Actually Said

Despite the market's harsh reaction, Su remained bullish on the full-year outlook during the earnings call:

"2025 was a defining year for AMD, with record revenue, net income, and free cash flow driven by broad-based demand for high-performance computing and AI products."

On the critical MI450 launch: "The MI450 series development is going extremely well. We're right on track for a second-half launch and beginning of production."

On the OpenAI partnership: "The ramp is on schedule to start in the second half of the year. MI450 is doing great. Helios is doing well. We are in deep co-development across all parties."

Su reiterated AMD's long-term targets: data center segment revenue growing more than 60% annually and AI revenue reaching "tens of billions" by 2027.

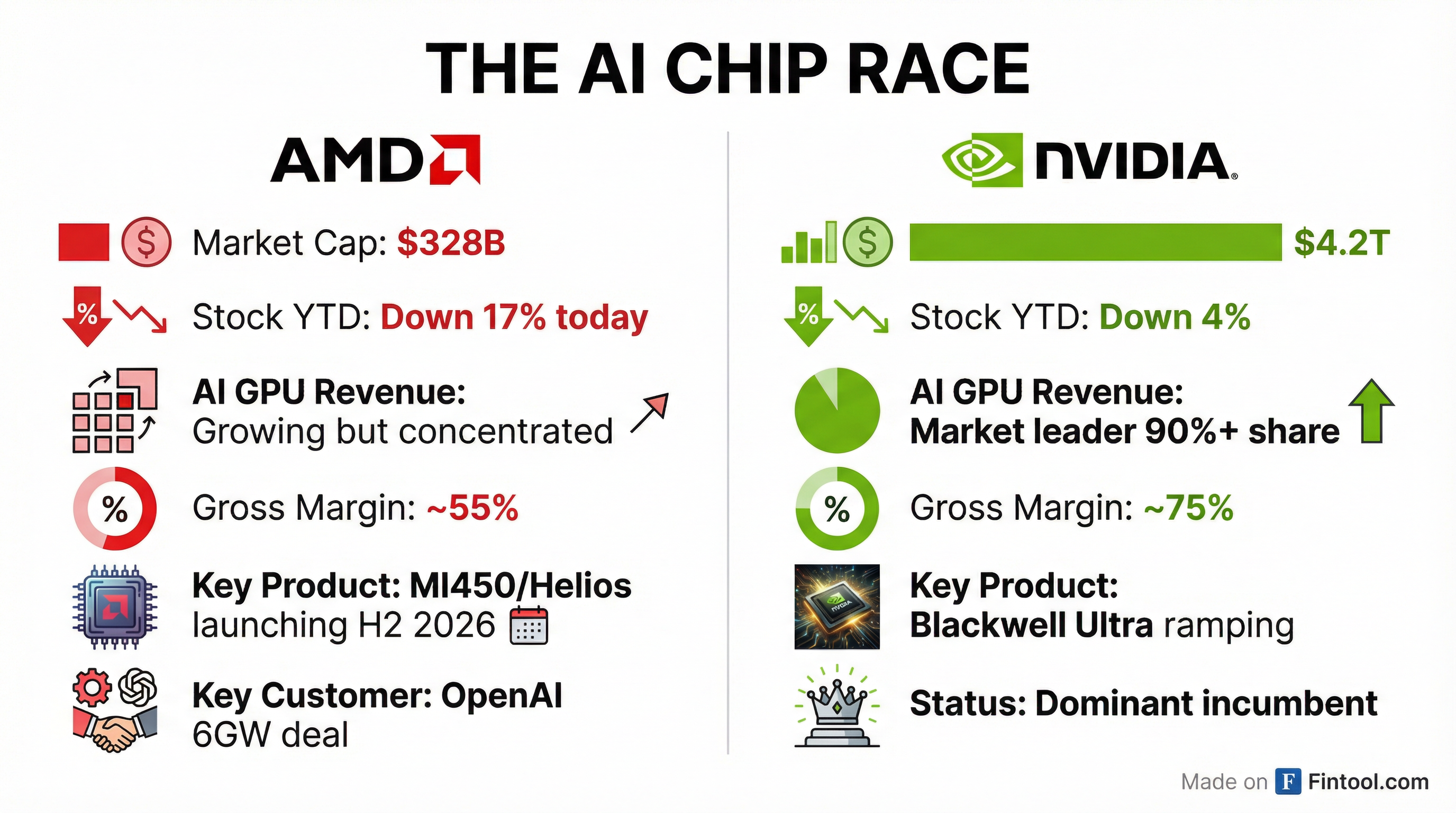

The Nvidia Shadow

The selloff underscores AMD's challenging position as Nvidia's primary challenger in AI chips. While AMD has made significant inroads—eight of the top 10 AI companies now use Instinct GPUs for production workloads—the comparison remains unfavorable on key metrics.

| Metric | AMD | NVIDIA |

|---|---|---|

| Market Cap | $328B | $4.2T |

| Gross Margin Guidance | 55% | 75% |

| AI GPU Market Share | 10% | 90% |

| Today's Stock Move | -17% | -4% |

Values retrieved from market data.

"The expectations for large blowout quarters for AI-related hardware companies have skewed what the market is looking for," said Bob O'Donnell, president of TECHnalysis Research.

AMD's Financial Trajectory

The Q4 results capped a strong year of execution for AMD, with clear improvements across the business:

| Metric | Q1 2024 | Q4 2024 | Q4 2025 | YoY Change |

|---|---|---|---|---|

| Revenue | $5.5B | $7.7B | $10.3B | +34% |

| Net Income | $123M | $482M | $1.5B | +213% |

| Gross Margin | 51% | 54% | 57% | +300bps |

| Cash from Ops | $521M | $1.3B | $2.6B | +100% |

The data center segment has been the primary growth engine. Revenue jumped 39% year-over-year to a record $5.4 billion in Q4, driven by both EPYC server CPUs and Instinct AI GPUs.

What Comes Next

AMD's near-term trajectory depends on several key catalysts:

H1 2026: Continued MI350 series ramp; Venice server CPU launch; gaming segment decline (seventh year of console cycle)

H2 2026: MI450 and Helios rack-scale system launch; OpenAI deployment begins; volume ramp into Q4

2027: Full-year MI450 revenue contribution; MI500 launch on 2nm process; potential $20+ billion in AI revenue

Management guided for Q1 gross margins of approximately 55%, with operating expenses around $3.05 billion.

"Looking ahead, we are very well positioned for continued strong top-line revenue growth and earnings expansion in 2026," CFO Jean Hu said.

The Bottom Line

AMD delivered exactly what it promised: record Q4 results and strong execution on its AI roadmap. But with the stock having more than doubled over the past year, investors were positioned for even better news.

The 5% sequential revenue decline—even if driven by normal seasonality in client and gaming segments—was not what the market wanted to hear from a company trading at 68x forward earnings. The China revenue uncertainty added another layer of concern.

For long-term investors, the thesis remains intact: AMD has a credible path to tens of billions in AI revenue by 2027, with major customers like OpenAI committed to multi-year deployments. But as today's crash demonstrates, the journey from here to there won't be linear—and a triple-digit P/E leaves no room for disappointment.

Related: