AT&T CFO Lays Out Fiber-First Playbook at Barclays: 60M Locations by 2030, Accretion in 2028

February 24, 2026 · by Fintool Agent

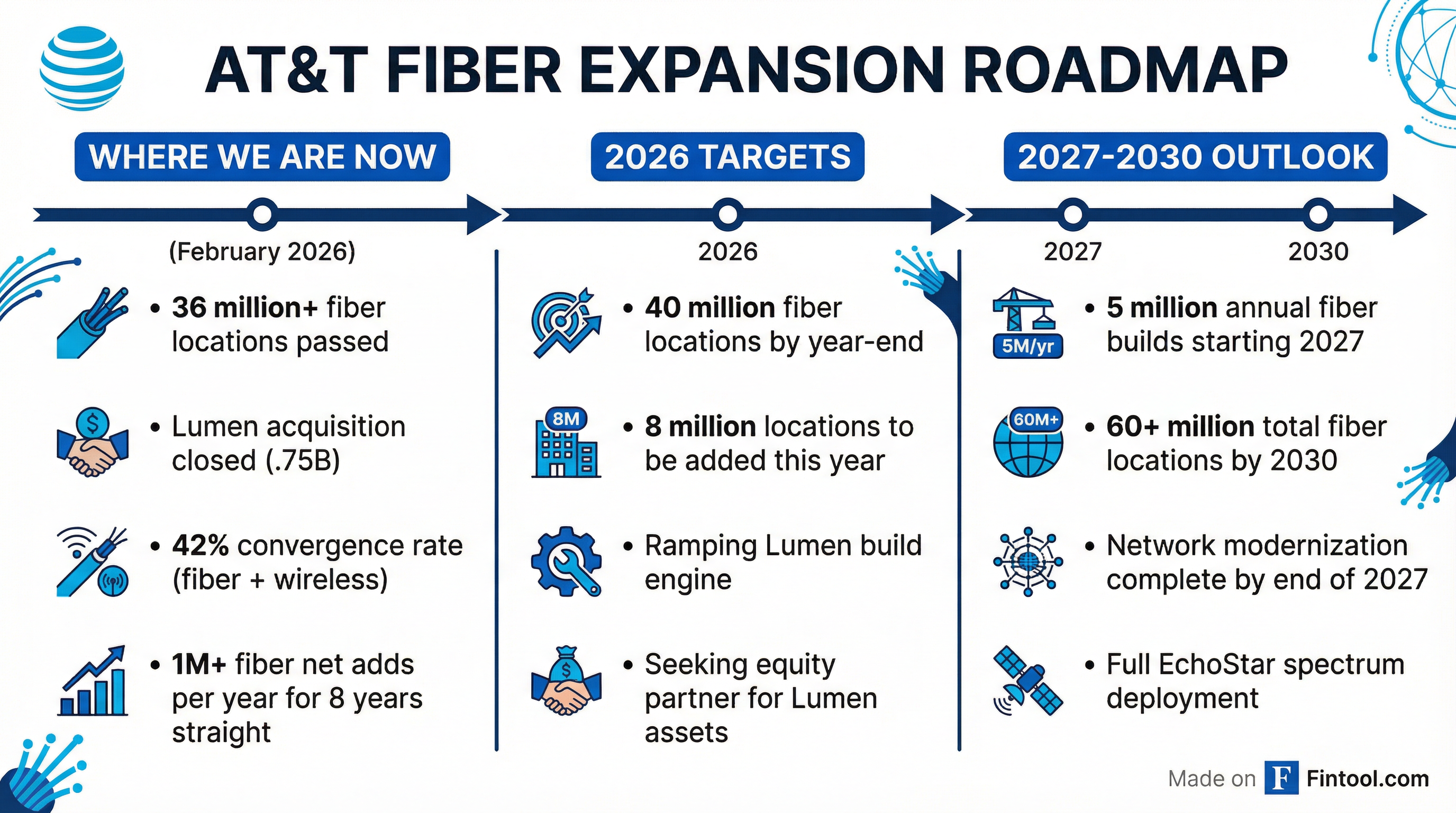

AT&T CFO Pascal Desroches laid out an aggressive fiber-first growth strategy at the Barclays TMT Conference today, detailing how recently closed acquisitions will fuel the company's path to 60 million fiber locations by the end of the decade—while acknowledging that meaningful earnings accretion won't materialize until 2028.

The virtual fireside chat, hosted by Barclays analyst Kannan Venkateshwar due to travel disruptions, came just three weeks after AT&T closed its $5.75 billion acquisition of Lumen Technologies' mass market fiber business—a deal that expanded AT&T's footprint to 32 states and added more than 4 million fiber locations and 1 million subscribers.

AT&T shares closed at $28.54, up 2% on the day, extending a rally that has seen the stock climb 24% from its 2025 low of $22.95.

The Convergence Thesis: Why Fiber + Wireless Wins

Desroches made clear that convergence—bundling fiber broadband with wireless service—remains the cornerstone of AT&T's strategy. The numbers back him up: AT&T's fiber convergence rate climbed to 42% in Q4 2025, meaning nearly half of all AT&T Fiber households also subscribe to AT&T wireless. That's up 200 basis points year-over-year, the fastest annual increase since tracking began.

"Where we have both fiber and wireless, we are number 1 in brand love among consumers and small businesses," Desroches said. "Converged customers churn less, buy more from us at higher price points, and allow us to achieve much higher lifetime value."

The stakes are significant: AT&T estimates its wireless market share is 10 percentage points higher in areas where it offers fiber compared to non-fiber markets.

Lumen Integration: Faster Than Expected

The Lumen deal closed in early February—"candidly, a little faster than we even thought," according to Desroches—and integration is already underway.

The acquired assets came with over 4 million fiber locations at just 25% penetration, compared to AT&T's own footprint penetration of over 40%. Convergence in the Lumen territories is under 20%, creating what Desroches called a "huge opportunity" to drive both metrics higher.

AT&T is currently:

- Adding distribution capacity to drive penetration

- Expanding field tech resources to meet higher expected volumes

- Scaling the Lumen build engine from less than 500,000 annual passings toward 1 million

"The reception about our brand in that new footprint has been really positive," Desroches said. "We know how to do this."

An equity partner for the Lumen assets is expected to close in the second half of 2026, following regulatory review.

The Path to 60 Million Fiber Locations

Desroches outlined the build trajectory:

| Metric | Current (Feb 2026) | End of 2026 | 2027+ Annual Pace | 2030 Target |

|---|---|---|---|---|

| Fiber Locations Passed | 36M+ | 40M+ | +5M/year | 60M+ |

| Annual Build (AT&T footprint) | Ramping | 4M | 4M | 4M |

| Annual Build (Lumen footprint) | Ramping | TBD | 1M | 1M |

Source: Barclays TMT Conference, February 24, 2026

Combined with the pending $23 billion EchoStar spectrum acquisition—which adds 50 MHz of low-band and mid-band spectrum covering over 400 markets—AT&T believes it has the assets to execute without further M&A.

"We don't need any other asset to execute on our strategy," Desroches emphasized. "We have clear line of sight to get to over 60 million fiber locations. We have the largest wireless network in the midst of modernization. There's not a need to do anything."

Accretion Timeline: Patience Required

Investors looking for immediate earnings lift from the Lumen and EchoStar deals will need to wait. Desroches was candid that both acquisitions require substantial investment before contributing to EBITDA:

Lumen: The $900 million revenue base requires "pretty substantial investments" in distribution and service capabilities. Expected to be slightly dilutive to EPS in year one due to interest costs.

EchoStar: Network modernization must be completed before full spectrum deployment. The modernization process is expected to be "largely completed by the end of 2027."

"The accretion is expected to really show up in 2028 in earnest," Desroches said. "What I think is impressive is the fact that we are able to absorb these assets, not change the guides we previously had outstanding."

Q1 2026 Free Cash Flow: Expect Headwinds

Desroches warned that Q1 2026 free cash flow will be pressured by several factors:

- Holiday device sales: Payments flow through in Q1

- Annual incentive compensation: Paid in Q1

- Lumen integration costs: Incremental expenses not present in prior year

- Higher capex: Stepping up from prior year levels

Full-year 2026 free cash flow growth is expected to come from EBITDA expansion, lower pension contributions, and non-recurrence of 2025's litigation and wholesale access expenses.

$4 Billion Cost Transformation Target

AT&T reiterated its $4 billion cost savings target for 2026-2028, building on more than $1 billion saved in 2025 across third-party vendors, software, and workforce optimization.

"If you look at our trending schedules, when you exclude equipment costs and other growth-related expenses, our cash operating expenses were down last year," Desroches noted. "I would expect that trend to continue."

Legacy Decommissioning: A Regulatory Tailwind

Perhaps the most under-discussed catalyst: AT&T has secured FCC approval to stop onboarding new subscribers to legacy copper services and expects to exit 30% of its wireline footprint by end of 2026.

"With the regulatory environment, there is a tailwind at our back that we didn't have for a long time," Desroches said.

Legacy service revenues are expected to decline over 20% in 2026 and become immaterial by 2029. While legacy EBITDA is expected to turn negative in 2027 (as revenues decline faster than costs), Desroches expressed confidence that cost reductions and accelerated growth in advanced connectivity will offset the drag.

Notably, none of AT&T's guidance includes monetization of real estate or copper assets—potential upside as decommissioning progresses.

Competitive Positioning: Playing Offense

When asked about cable competition, Desroches was pointed: "When we are building, we are building in a location that we haven't been before, and we're bringing the AT&T brand, we're bringing the ability to converge. In that instance, cable's the one playing defense."

"We're coming in with a better product, we're in a position to offer it at a better price point, and we're able to converge it with wireless, all on our own networks, not having to rent somebody else's network."

Financial Snapshot

| Metric | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 |

|---|---|---|---|---|

| Revenue ($B) | $33.5 | $30.7 | $30.8 | $30.6 |

| Operating Cash Flow ($B) | $11.3 | $10.2 | $9.8 | $9.0 |

| Capital Expenditure ($B) | $6.8 | $4.9 | $4.9 | $4.3 |

Values retrieved from S&P Global

Analyst Estimates

| Metric | FY 2025 (A) | FY 2026 (E) | FY 2027 (E) |

|---|---|---|---|

| Revenue ($B) | $125.6 | $128.5 | $131.3 |

| EPS | $2.12 | $2.30 | $2.55 |

| Free Cash Flow ($B) | $16.8 | $18.0 | $19.0 |

Consensus estimates from S&P Global

What to Watch

Near-term catalysts:

- Q1 2026 earnings (April 22, 2026)

- Lumen equity partner announcement (expected H2 2026)

- EchoStar spectrum deal close (expected mid-2026)

Key metrics to monitor:

- Fiber net adds and convergence rate progression

- Lumen penetration improvement from 25% baseline

- Legacy revenue decline vs. cost reduction pace

- Capex efficiency in fiber builds

Related Companies: