Cleveland-Cliffs Stock Crashes 19% as Revenue Miss Overshadows Beat on Earnings

February 9, 2026 · by Fintool Agent

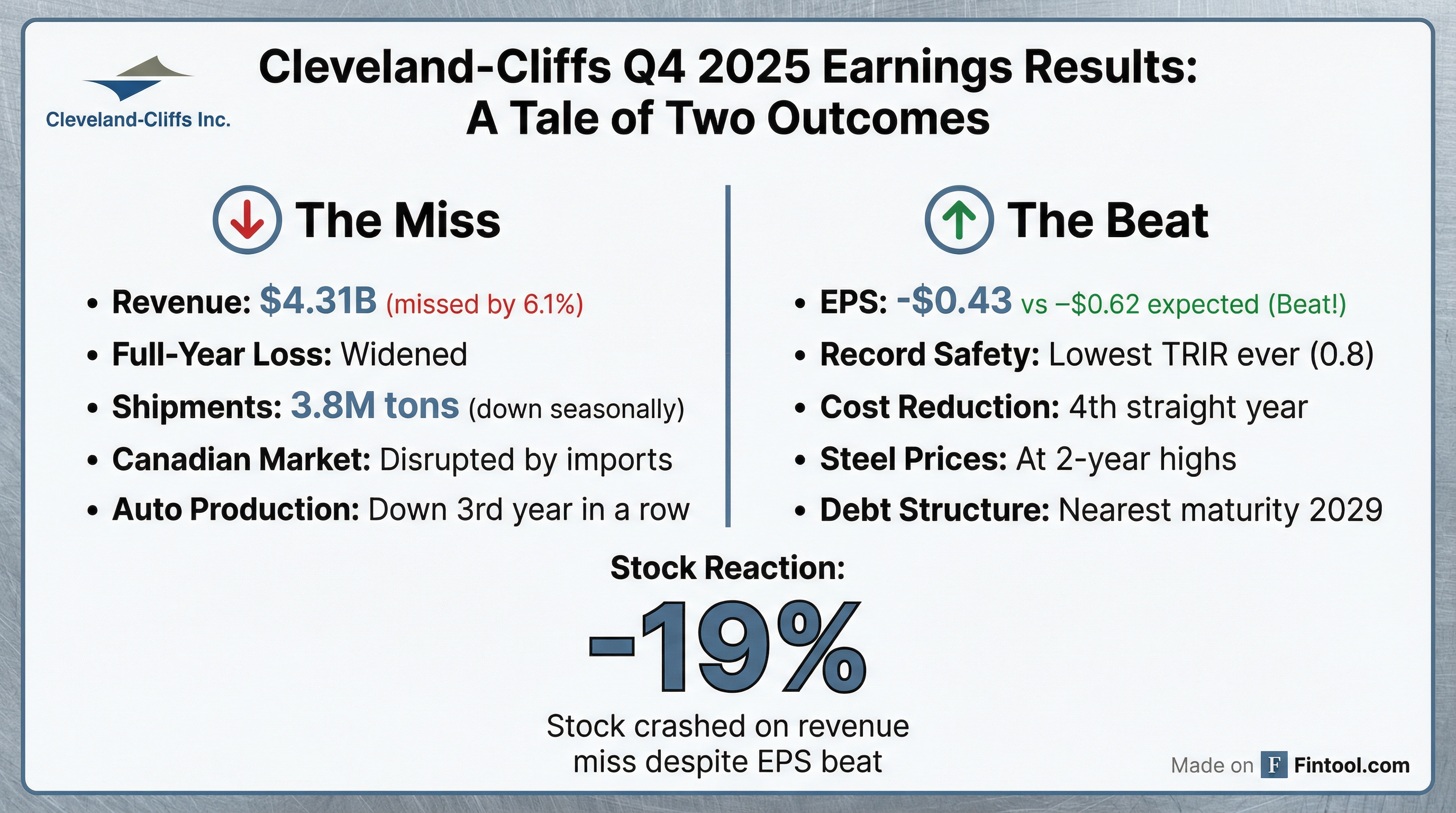

Cleveland-cliffs (CLF) shares plummeted 19% Monday morning after the integrated steelmaker reported fourth-quarter revenue of $4.31 billion, missing Wall Street expectations of $4.59 billion by 6.1%. The decline marks one of the steepest single-day drops for the stock in recent memory, erasing gains from a rally that had pushed shares to a 52-week high of $16.18 in October.

The revenue miss overshadowed what should have been good news: adjusted EPS of -$0.43 beat consensus estimates of -$0.62, narrowing the loss by 31%.

"The factors that weighed on our performance in 2025 were well-known and addressable," CEO Lourenco Goncalves declared on the earnings call, maintaining his characteristically bullish tone despite posting the company's fourth consecutive quarterly loss. "Fortunately, as we started 2026, these negative situations have all improved."

A Year of Headwinds

Cleveland-Cliffs' 2025 performance was battered by a perfect storm of challenges that management spent the earnings call explaining—and promising to overcome.

Weak Automotive Demand: U.S. vehicle production declined for the third consecutive year, directly impacting Cliffs' core end market. The company's automotive volumes fell in Q4, contributing to the revenue miss.

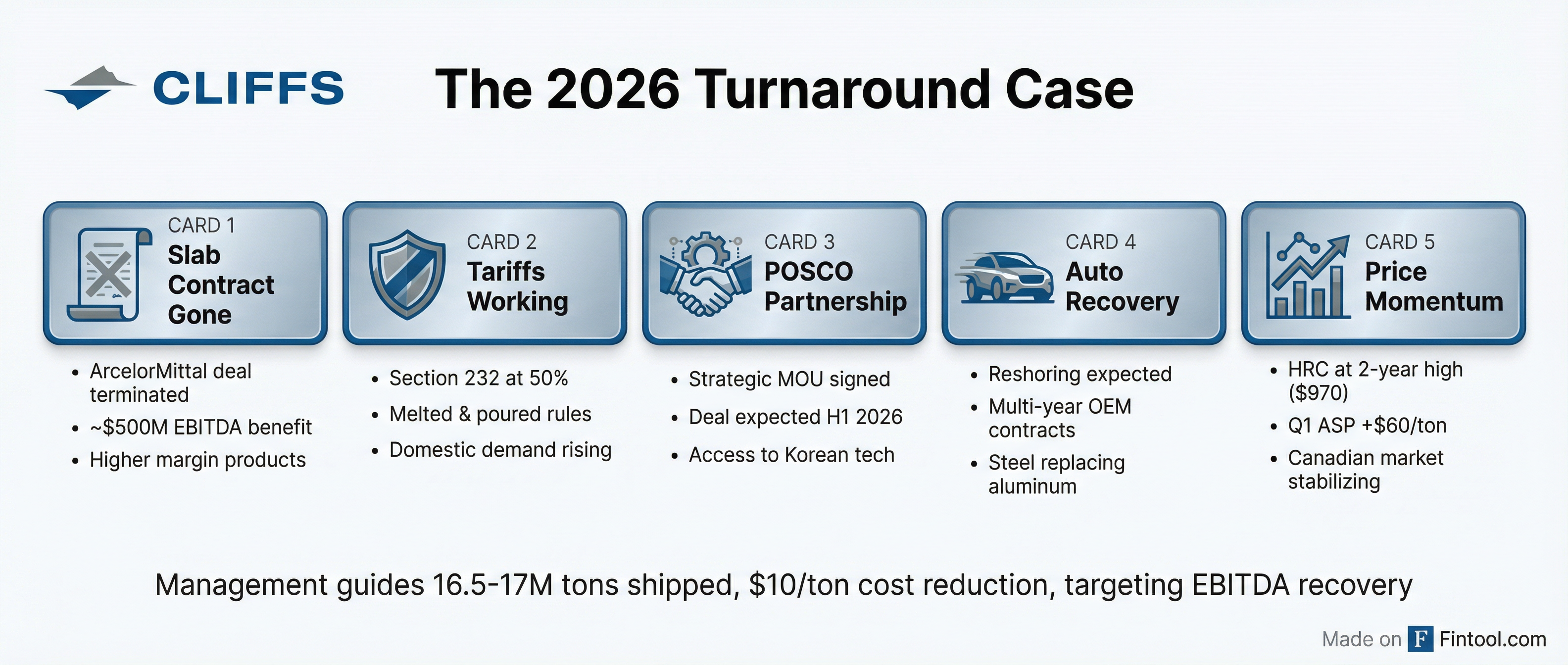

The "Disastrous" Slab Contract: A supply agreement with Arcelormittal that linked slab prices to Brazilian indices became, in Goncalves' words, "very onerous in its final year when the Brazilian slab price index unnaturally separated from the U.S. finished steel prices." The contract has now expired, which management frames as a major positive catalyst for 2026.

Canadian Market Disruption: The company's $2.5 billion acquisition of Stelco, completed just days before President Trump's 2024 election, ran into headwinds when Canada became a "dumping ground for producers trying to avoid U.S. tariffs." Canadian pricing decoupled from U.S. pricing, pressuring Stelco's margins.

The $500 Million EBITDA Swing

The headline catalyst for 2026 is the termination of the ArcelorMittal slab contract. When asked to quantify the benefit, Goncalves provided a number that investors should note:

"If I can put a number on the gain, the EBITDA number by itself is to the order of $500 million just by replacing the slabs with higher margin... That's just the benefit on us, not the fact that competition for automotive business became automatically weaker when you don't make our slabs available to a competitor."

CFO Celso Goncalves added color: with hot-rolled coil prices at approximately $970/ton and the slab price having been around $485, the company sees roughly $700 million in revenue improvement at current prices, offset by approximately $150 million in additional conversion costs.

| Metric | Q4 2024 | Q3 2025 | Q4 2025 | Q1 2026E |

|---|---|---|---|---|

| Revenue | $4.33B | $4.73B | $4.31B* | $5.0B |

| Net Income | -$447M | -$251M | -$280M* | Improving |

| EPS (Actual) | -$0.68 | -$0.45 | -$0.43* | -$0.07 (est) |

| ASP/ton | $1,040 | $1,033 | $993 | $1,053 |

| Shipments | 4.0M tons | 4.0M tons | 3.8M tons | 4.0M tons |

*Q4 2025 values from company earnings release; Values retrieved from S&P Global

POSCO Partnership: The Strategic Wild Card

Perhaps the most intriguing development is Cleveland-Cliffs' memorandum of understanding with POSCO, Korea's largest steelmaker and the world's third-largest outside of China. The partnership would allow POSCO to serve its U.S. customers while meeting "melted and poured" domestic content requirements.

"They came to us. We did not look for them," Goncalves emphasized. "We feel like they need us probably much more than we need them."

A definitive agreement is targeted for the first half of 2026, though the CEO stressed the Cleveland-Cliffs board will only approve a deal that is "accretive to our shareholders."

The POSCO negotiations have also put larger asset sales on hold. Management has interest in selling Toledo HBI and FPT assets, which would be incremental to the $425 million in proceeds expected from selling idled plants.

The Aluminum Replacement Opportunity

Beyond the near-term catalysts, Goncalves highlighted a potentially significant long-term opportunity: replacing aluminum with steel in automotive applications.

"We proved our point that stamping aluminum or stamping steel for the type of steels that we Cleveland-Cliffs produce is the same thing," he said. "We proved that at this point with three different OEMs... The best-selling vehicle in the United States has a lot of aluminum in the outside. We are starting to produce parts for that vehicle."

The aluminum supply chain's vulnerability was exposed by "a succession of fire events" that demonstrated its weakness compared to domestic steel production, according to Goncalves.

The Balance Sheet Question

Despite the optimistic guidance, Cleveland-Cliffs carries substantial debt—$8.1 billion in total debt as of Q3 2025 —a legacy of acquisitions including the $2.5 billion Stelco deal and earlier purchases.

The CFO acknowledged: "From a pure dollar perspective, our leverage remains too elevated for my liking." However, he emphasized the "shape and format" of the debt structure provides flexibility, with the nearest bond maturity now in 2029 and total liquidity of $3.3 billion.

All expected free cash flow in 2026 will be directed toward debt reduction.

2026 Guidance Summary

Management provided the following outlook for 2026:

| Metric | Guidance |

|---|---|

| Shipment Volume | 16.5-17.0 million net tons |

| Q1 ASP Increase | +$60/ton from Q4 |

| Unit Cost Reduction | -$10/ton vs 2025 |

| CapEx | $700 million |

| Slab Contract Benefit | $500M EBITDA |

What to Watch

-

Q1 2026 Results: Management's guidance for $60/ton higher ASP and 4 million tons shipped will be the first real test of the turnaround thesis.

-

POSCO Definitive Agreement: Targeted for H1 2026, the structure and terms of this deal could significantly alter Cliffs' strategic position.

-

U.S. Auto Production: The reshoring narrative depends on domestic vehicle production recovering from three years of decline.

-

Steel Prices: With HRC at a two-year high of approximately $970/ton, any softening would pressure the 2026 outlook.

-

Canadian Market: Whether the Canadian government's recent restrictions on steel imports prove sufficient to stabilize Stelco's performance.

The 19% single-day plunge suggests investors remain skeptical that Cleveland-Cliffs can execute on what amounts to a highly optimistic turnaround narrative after a difficult 2025. The next few quarters will determine whether Goncalves' confidence is justified or whether the stock's reaction reflects deeper structural concerns.

Related: