Conagra Declares 'Return to Growth' at CAGNY 2026, Raises Free Cash Flow Outlook

February 17, 2026 · by Fintool Agent

Conagra Brands (CAG) delivered what CEO Sean Connolly called a "bit of positivity" at the 2026 Consumer Analyst Group of New York (CAGNY) conference on Tuesday, claiming the $12 billion packaged food company has returned to growth after a challenging period.

The market wasn't buying it. Shares fell 3.4% to $19.13, hitting an intraday low of $19.04—near where the stock traded at its 52-week low of $15.96. The skepticism comes despite management reaffirming full-year guidance and raising free cash flow conversion expectations to 100% from the prior 90% target.

The Numbers: Guidance Reaffirmed, Cash Flow Upgraded

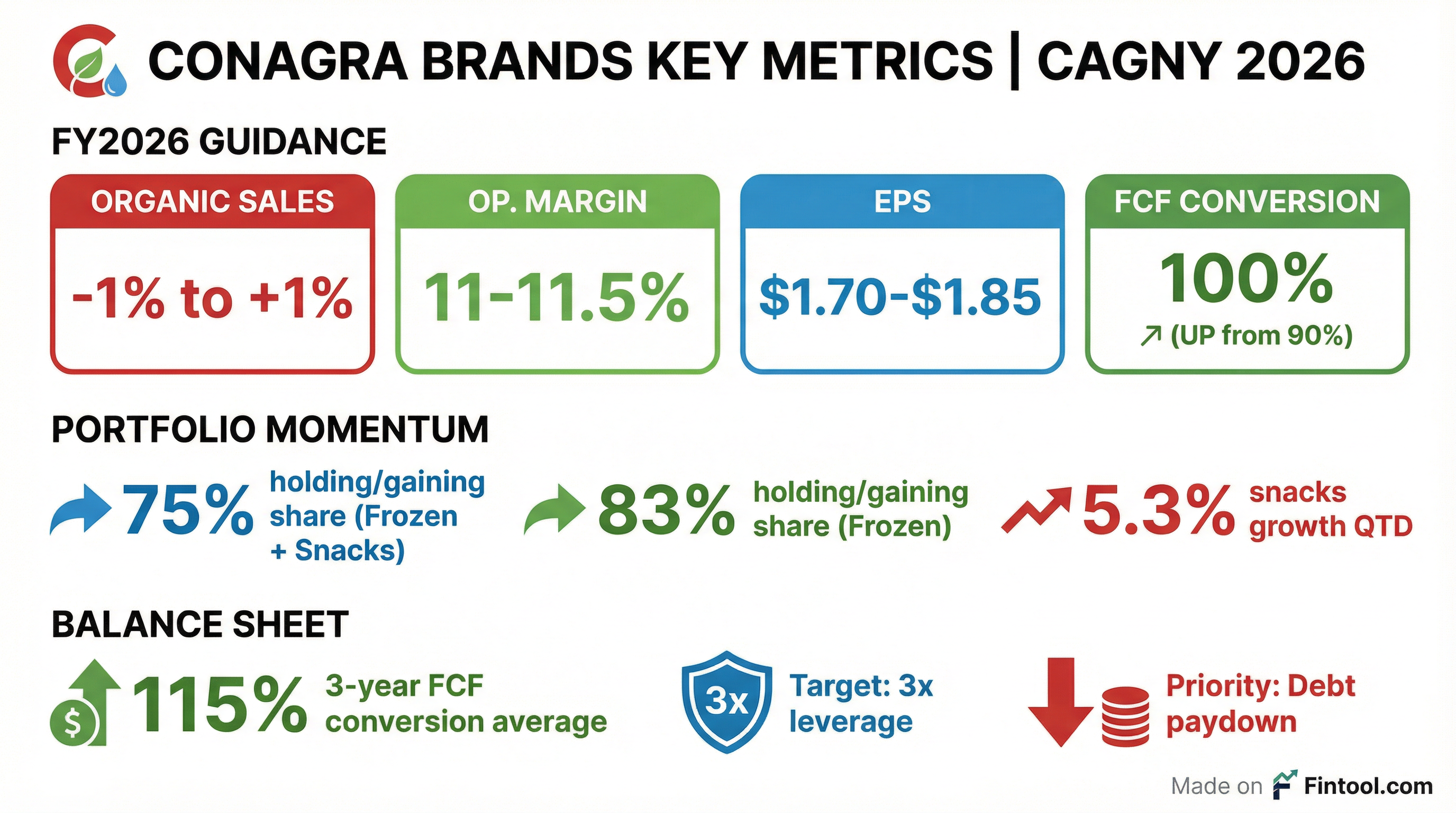

Ahead of the CAGNY presentation, Conagra filed an 8-K reaffirming fiscal 2026 guidance:

| Metric | FY2026 Guidance |

|---|---|

| Organic Net Sales | -1% to +1% vs FY2025 |

| Adjusted Operating Margin | 11.0% - 11.5% |

| Adjusted EPS | $1.70 - $1.85 |

| Free Cash Flow Conversion | 100% (raised from 90%) |

CFO Dave Marberger highlighted that the company's three-year free cash flow conversion now averages 115%—a figure he called "industry-leading." The improvement stems from inventory reduction, better cash efficiency at Ardent Mills (Conagra's flour milling joint venture), and improved cash tax management.

The Growth Narrative: 75% of Portfolio Holding or Gaining Share

Connolly's central message: after "the fellowship of the miserable" at last year's CAGNY, Conagra is back on offense.

Portfolio momentum metrics:

| Metric | Performance |

|---|---|

| Frozen + Snacks holding/gaining share | 75% of portfolio (last 13 weeks) |

| Frozen portfolio holding/gaining share | 83% of portfolio |

| Snacks growth | 5.3% quarter-to-date |

The company's growth domains—frozen and snacks—represent roughly 70% of revenue, while the staples segment (center store grocery) generates high-margin cash flow to fund innovation.

Recent Financial Performance

| Metric | Q2 2025 | Q3 2025 | Q4 2025 | Q1 2026 | Q2 2026 |

|---|---|---|---|---|---|

| Revenue ($B) | $3.20 | $2.84 | $2.78 | $2.63 | $2.98 |

| EBITDA Margin | 18.6%* | 17.6%* | 17.1%* | 15.5%* | 14.7%* |

| Net Debt ($B) | $8.43 | $8.10 | $8.24* | $7.58 | $7.58 |

*Values retrieved from S&P Global

The Q2 2026 net income was impacted by a significant write-down, resulting in a net loss of $664 million —explaining why the headline EPS figures look distorted.

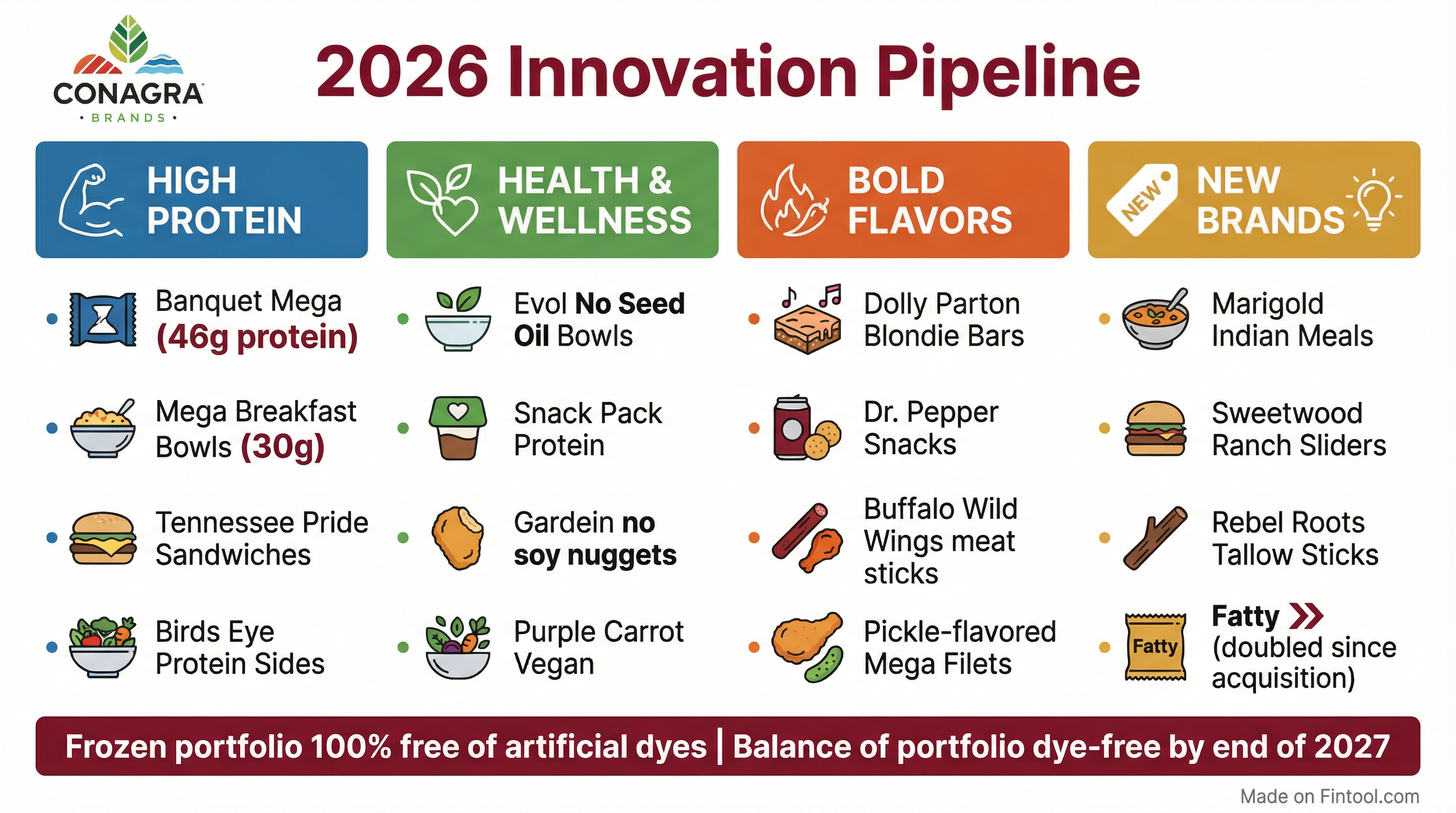

Innovation Blitz: From Dolly Parton to Dr. Pepper

SVP of Growth Science Bob Nolan unveiled an aggressive innovation pipeline targeting four consumer megatrends: high protein, health & wellness, bold flavors, and new brand creation.

Standout launches for 2026:

- Banquet Mega lineup: Up to 46 grams of protein, targeting younger consumers with QSR-inspired flavors

- Dr. Pepper Snacks: Taking the #2 soda brand into the portable snacking category

- Dolly Parton Blondie Bars: Celebrity partnership in the baking aisle

- Rebel Roots Tallow Sticks: Capitalizing on the tallow fat and "no seed oils" trend

- Marigold Indian Meals: New brand developed with leading Indian chefs across North America

- Fatty meat sticks: Has doubled in size since acquisition just over a year ago

Nolan emphasized that Conagra's frozen portfolio is already 100% free of artificial dyes, with the balance of the portfolio going dye-free by end of 2027.

GLP-1: A Tailwind, Not a Headwind

Unlike some packaged food peers worried about weight-loss drugs suppressing snacking, Conagra positioned itself as a beneficiary.

Nolan noted GLP-1 penetration remains under 8% but expects it to reach "double digits in the very near term." For users on these medications, "every calorie has to work harder to deliver the nutrition you need," creating demand for:

- Portion-controlled frozen meals

- High-protein options

- Fiber-rich products

- Nutrient-dense snacks

"Overall, in the data we've been analyzing around GLP-1 users, we've seen certainly advantages in the frozen space," Nolan said. "A lot more portion control in meals with protein, a lot more frozen appetizers, and certainly a lot more nutrient-dense snacks."

Project Catalyst: The AI Card

CFO Marberger teased "Project Catalyst," a multi-year initiative leveraging AI to modernize operations. The company has invested in a single ERP platform globally and data foundations for years—now it's ready to layer AI on top.

"We look at Catalyst as being able to leverage that in order to leverage today's AI capabilities, so that we can drive this financial performance... We have a multi-year effort starting, with senior leadership involved, looking at our work processes end to end to see how we can leverage AI to drive performance."

Management promised more details with Q4 earnings when FY2027 guidance is released.

FY2027 Preview: Top-Line Momentum to Continue

While not providing formal FY2027 guidance, Marberger outlined expectations:

- Top-line momentum to continue

- Margin recovery opportunities from productivity gains and normalizing inflation

- Free cash flow strength to persist

- 4% annual cost savings as a long-term target (5% this year including 1% from tariff mitigation)

The company's long-term algorithm—not explicitly quantified at CAGNY—remains unchanged.

Analyst Estimates

Wall Street is modeling modest growth ahead:

| Metric | Q3 2026E | Q4 2026E | Q1 2027E | Q2 2027E |

|---|---|---|---|---|

| Revenue ($M) | $2,761* | $2,869* | $2,642* | $3,004* |

| EPS | $0.40* | $0.47* | $0.41* | $0.49* |

| Target Price | $19.05* | - | - | - |

*Values retrieved from S&P Global

The consensus target price of $19.05 implies essentially no upside from current levels—suggesting analysts remain cautious despite management's growth narrative.

The Bottom Line

Conagra's CAGNY 2026 presentation painted an optimistic picture: supply chain restored to 98%+ service levels, 75% of the growth portfolio gaining share, a robust innovation pipeline, and improving cash generation.

But the stock's 3.4% decline tells a different story. The market may be skeptical that:

- Flat organic sales growth (-1% to +1%) represents a true "return to growth"

- EBITDA margins have compressed from ~20% to ~15% over the past two years*

- Debt levels remain elevated at $7.6 billion, even after prioritizing paydown

The real test comes with Q3 earnings and FY2027 guidance. Until then, the question remains whether Conagra's "superior relative provocativeness"—the conference's central theme—can translate into share price appreciation.