Klarna Crashes 25% as Q4 Loss Shatters Post-IPO Dreams

February 19, 2026 · by Fintool Agent

Klarna's stock cratered 25% Thursday after the Swedish buy-now-pay-later giant swung to a $26 million loss in Q4 and warned that growth would slow—a brutal wake-up call for investors who bet on Europe's largest fintech IPO just five months ago.

Shares plunged from $18.95 to $14.22 on volume of 22.9 million—more than triple the average. The stock has now collapsed 65% from its $40 IPO price and 69% from its first-day close of $45.82, erasing nearly $10 billion in market value.

The Numbers Behind the Crash

| Metric | Q4 2025 Result | Expectation | Beat/Miss |

|---|---|---|---|

| Revenue | $1.08B | $1.0B | Beat (+8%) |

| Net Income | -$26M | $0 (breakeven) | Miss |

| EPS | -$0.19 | -$0.03 | Miss (-$0.16) |

| Active Consumers | 180M | — | +28% YoY |

The revenue beat meant nothing. Investors zeroed in on the bottom line: Klarna promised profitability was imminent, and instead delivered a $26 million hole.

Management compounded the damage by warning that gross merchandise volume growth would decelerate in Q2 2026 due to tough year-over-year comparisons, and that new partnership rollouts would be "gradual" rather than explosive.

From IPO Darling to Cautionary Tale

The speed of Klarna's unraveling is remarkable:

| Date | Event | Price | Market Cap |

|---|---|---|---|

| Sept 2, 2025 | IPO Launch Announced | $40 (target) | $15B |

| Sept 10, 2025 | First Trading Day | $45.82 (close) | $17B |

| Feb 18, 2026 | Day Before Earnings | $18.95 | $9B |

| Feb 19, 2026 | Post-Earnings | $14.22 | $7.3B |

This was supposed to be different. Klarna's September IPO was the largest fintech listing of 2025, raising $1.37 billion and pricing above the expected range at $40 per share. Goldman Sachs, JPMorgan, and Morgan Stanley led the offering. Sequoia, an early investor, generated a $2.65 billion return on paper.

The BNPL Reckoning

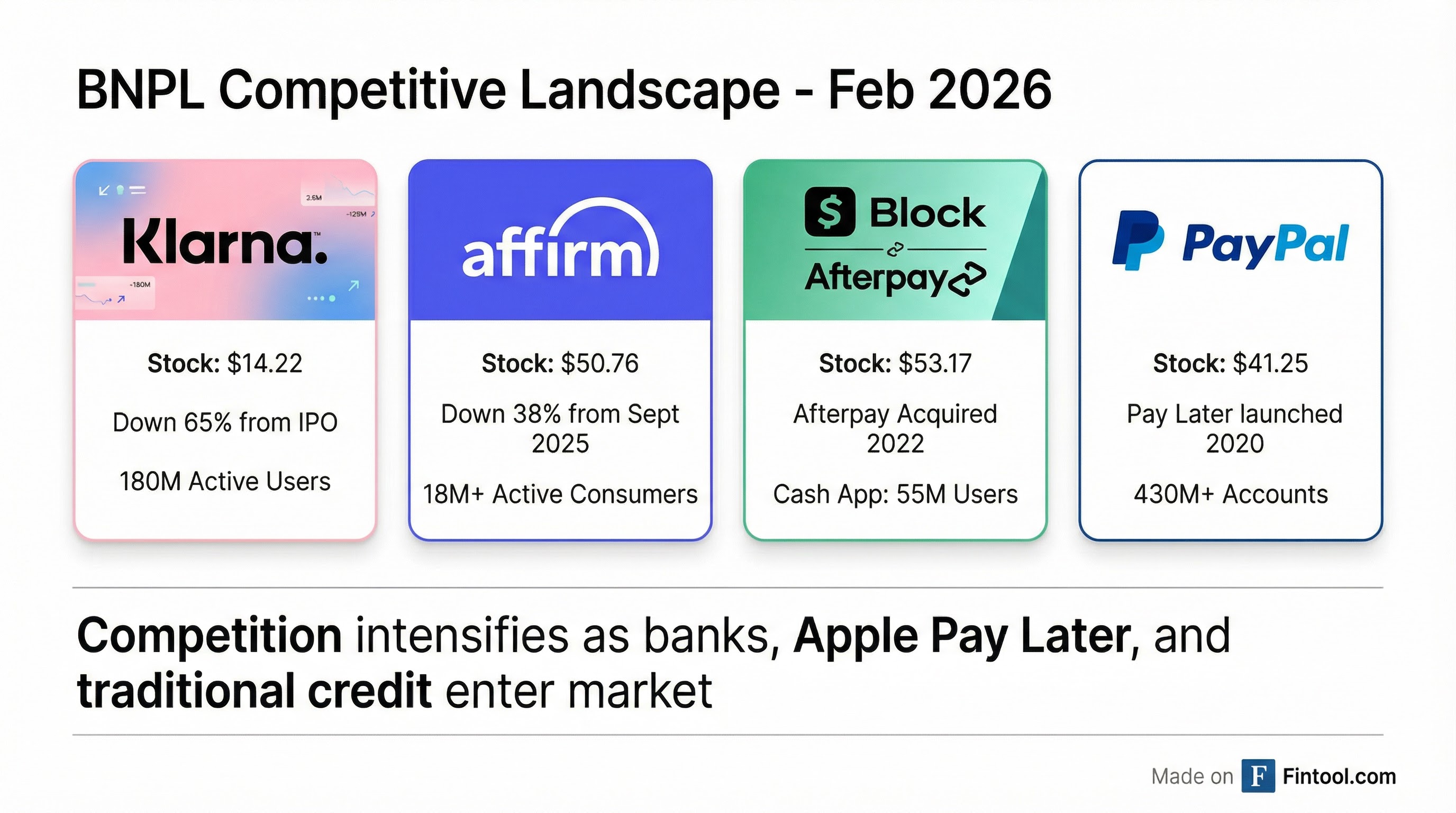

Klarna isn't falling alone. The entire buy-now-pay-later sector is under pressure as the market questions whether these companies can ever achieve sustainable profitability in a higher-rate environment.

| Company | Ticker | Price | Market Cap | Change (Since Sept '25) |

|---|---|---|---|---|

| Klarna | KLAR | $14.22 | $7.3B | -65% |

| Affirm | AFRM | $50.76 | $16.9B | -38% |

| Block | XYZ | $53.17 | $32.4B | -35% |

| Paypal | PYPL | $41.25 | $37.6B | -39% |

Affirm fell nearly 2% in sympathy on Thursday. Block and PayPal also traded lower. The message from markets: BNPL skepticism is sector-wide, not Klarna-specific.

The competitive landscape has intensified dramatically. Apple launched Apple Pay Later, traditional banks have entered with their own installment products, and regulatory scrutiny has increased in both the US and UK. Klarna's moat—first-mover advantage and brand recognition among Gen Z—is under siege.

What Went Wrong

Three factors explain Klarna's post-IPO collapse:

1. Profitability Mirage Klarna reported a $21 million profit in 2024, its first full-year gain since 2019. Management framed this as proof that the business had turned a corner. But Q2 2025 swung to a $50 million loss, and now Q4 adds another $26 million in red ink. The "path to profitability" narrative has evaporated.

2. Competitive Moat Erosion With 180 million active consumers—10x Affirm's user base—Klarna still has scale. But user growth has slowed, and the company is spending heavily on expansion beyond BNPL into banking (debit cards, deposit accounts) without clear evidence that diversification improves margins.

3. Valuation Reset At its $45.6 billion peak valuation in 2021, Klarna traded at roughly 40x revenue. Today, at $7.3 billion, it trades at less than 2x revenue—but investors still aren't convinced that's cheap enough given the profitability uncertainty.

What to Watch

Near-term Catalysts:

- Q1 2026 earnings (late April): Will losses persist or narrow?

- New partnership announcements: Management emphasized gradual rollouts—any acceleration would help sentiment

- Klarna Card adoption: The company has 700,000 US card customers with 5 million on the waitlist

Risks:

- Continued credit losses as consumer balance sheets weaken

- UK regulatory tightening (new BNPL oversight rules pending)

- Further competition from Apple, banks, and Affirm

The Bottom Line

Klarna's 25% crash is more than an earnings miss—it's a referendum on whether BNPL's growth story can translate into profit. The Swedish fintech still has the largest user base in the industry, strategic partnerships with Stripe and Walmart, and ambitions to become a full-service digital bank.

But at $14.22, down 65% from its IPO price and 69% from its first-day pop, investors are demanding proof. A sector that was worth $45 billion to Klarna alone in 2021 is now valued at a combined $64 billion across four major players—and even that may be too generous until someone proves BNPL can consistently make money.

Related: