Novo Nordisk Slashes Wegovy and Ozempic Prices by Up to 50%—One Day After CagriSema Trial Failure

February 24, 2026 · by Fintool Agent

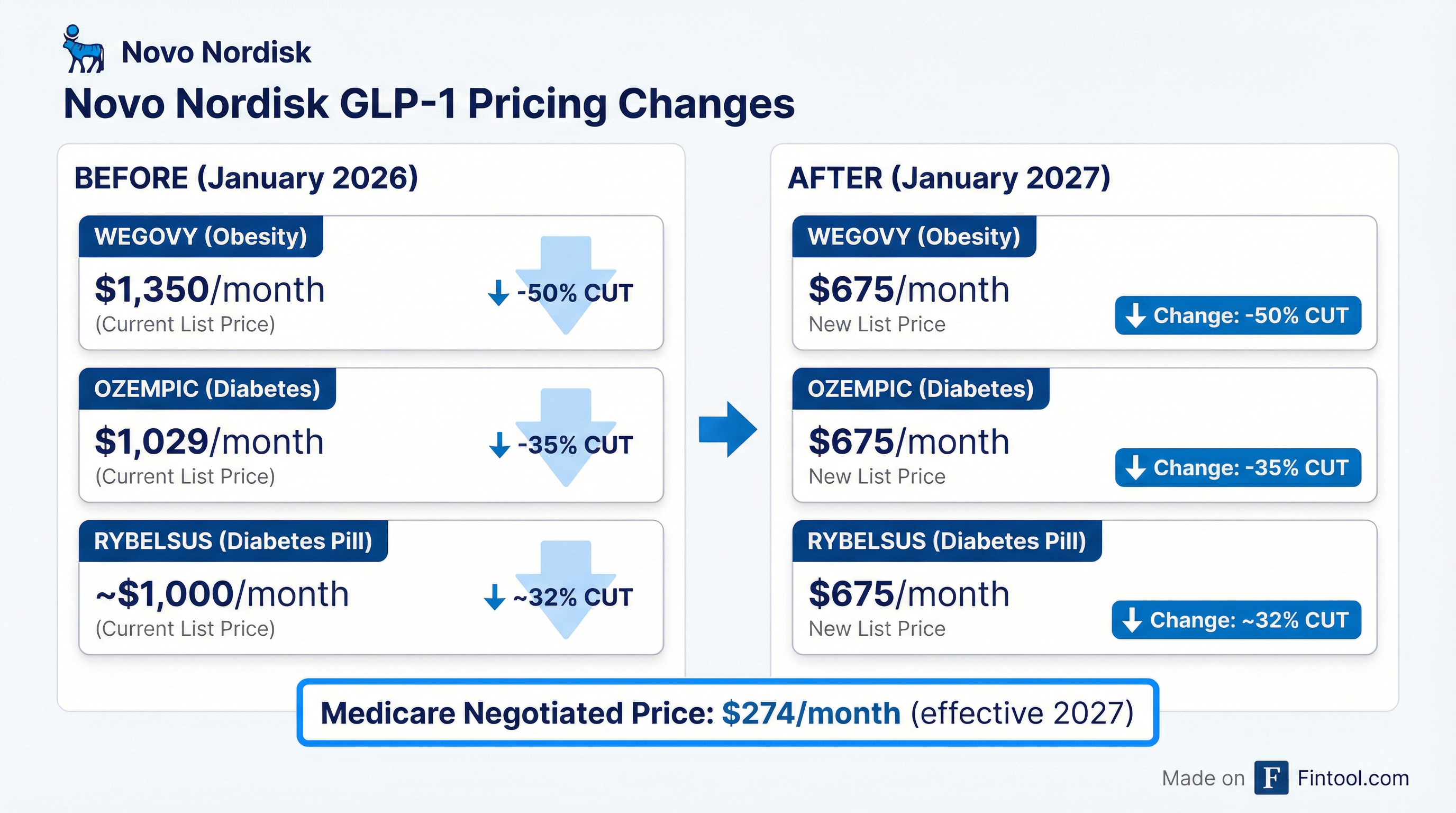

Novo Nordisk announced Tuesday it will slash U.S. list prices for its blockbuster obesity drug Wegovy by 50% and diabetes treatment Ozempic by 35%—less than 24 hours after disappointing clinical trial data dealt another blow to the Danish drugmaker's efforts to catch rival Eli Lilly.

The new list price for all three semaglutide medicines—Wegovy, Ozempic, and the oral diabetes drug Rybelsus—will be $675 per month effective January 1, 2027. That marks a 50% cut from Wegovy's current list price and a 35% reduction for Ozempic.

Novo shares fell another 3% on Tuesday, extending Monday's 16% plunge to a four-year low—a two-day decline that wiped billions from the company's market capitalization and brought 12-month losses to 60%.

The Price Cuts

"Private and public payers, as well as patients, want access and have been calling for lower list prices," said Jamey Millar, Novo Nordisk's head of U.S. operations. "Our actions today answer that call and remove cost barriers so the value of Wegovy and Ozempic can be realized by more patients."

The move coincides with new, lower Medicare prices taking effect for Novo's drugs in 2027 following negotiations under the Inflation Reduction Act. Medicare will pay just $274 per month—roughly 60% below the new list price for insured patients.

| Drug | Indication | Current Price | New Price (2027) | Cut |

|---|---|---|---|---|

| Wegovy | Obesity | $1,350/mo | $675/mo | -50% |

| Ozempic | Diabetes | $1,029/mo | $675/mo | -35% |

| Rybelsus | Diabetes (Oral) | $1,000/mo | $675/mo | 32% |

The CagriSema Setback

The price cuts come just one day after Novo revealed its next-generation obesity drug CagriSema failed to match Eli Lilly's Zepbound in a head-to-head Phase 3 trial—a result analysts called a "gigantic own goal."

CagriSema helped patients lose an average of 23% of their body weight over 84 weeks, compared with 25.5% for those taking Zepbound. The difference was significant enough that CagriSema could not be declared "non-inferior" to Lilly's treatment—the minimum threshold Novo needed to meet.

At least seven analysts cut their price targets on Novo Nordisk following the data:

- Deutsche Bank downgraded to Hold, slashed price target to DKK 275 from DKK 400

- Barclays cut CagriSema peak sales estimates from $12 billion to $2 billion—an 80% reduction

- JPMorgan: "It would now be difficult for Novo to dislodge market share from Lilly, with Zepbound well entrenched"

Barclays concluded that Novo is left with "little to compete on apart from price."

Price Is the Strategy Now

CEO Mike Doustdar acknowledged as much on Novo's February 5 earnings call, stating bluntly that "price is an important element of how much volume gets untangled in this business."

He pointed to the threat from compounders—pharmacies that sell knockoff versions of GLP-1 drugs—as a wake-up call: "The reason people were picking up a compounding knockoff product was not because they don't want the original. It's because they couldn't afford the original."

The Wegovy pill, launched in January 2026 at a direct-to-consumer price of $149, provides a template. Doustdar said the pill generated 50,000 new prescriptions in its first month—15 times more than the Wegovy injection at launch and twice the first-month performance of Lilly's Zepbound.

"We believe with what we have announced that it's worth the short-term pain because the volumes were easily bypassed," Doustdar said. "You have to price double the volume, you break even. If I didn't think you do much, much better than doubling the volume, we would not go in this direction."

Lilly's Widening Lead

The competitive backdrop could hardly be worse for Novo. While the Danish company projects sales and profits declining 5-13% in 2026, Eli Lilly guided for revenue of $80-83 billion—representing 25% growth.

The divergence is playing out in real-time:

| Metric | Novo Nordisk | Eli Lilly |

|---|---|---|

| Q4 2025 Revenue | $12.4B* | $19.3B |

| 2026 Revenue Guidance | DOWN 5-13% | UP 25% to $80-83B |

| Stock (12-Month) | DOWN 60% | Near all-time highs |

| Flagship Drug Efficacy | Wegovy: 15-21% weight loss | Zepbound: 25.5% weight loss |

| Next-Gen Drug | CagriSema: 23% (failed trial) | Retatrutide: 28.7% in trials |

Lilly's Zepbound revenue surged 122% year-over-year to $4.2 billion in Q4 2025, while Wegovy sales actually fell 2% in the U.S.—reversing years of strong growth.

"This obesity market, now two years into deep competitiveness element of it with Lilly as well as compounders, has taught Novo Nordisk it's first and foremost about the magnitude of weight loss," Doustdar acknowledged on the February earnings call. "I think kidney matters, heart matters, liver matters, but not if you are perceived to have a lower weight loss than your competition."

What to Watch

Volume response: Novo is betting that halving list prices will more than double volumes. The company will need to demonstrate this trade-off works in 2027.

Medicare uptake: With negotiated Medicare prices of $274/month, government coverage could expand significantly. How quickly beneficiaries switch to branded drugs from compounders will be critical.

Lilly's oral GLP-1: Eli Lilly's orforglipron pill is expected to gain FDA approval in April 2026, creating direct competition for Novo's first-mover advantage with the Wegovy pill.

CagriSema's fate: Despite the trial miss, Novo filed for FDA approval in late 2025. A decision is expected in late 2026. Management argues the drug still has a path forward with competitive label data.

The Bottom Line

Novo Nordisk's price cuts represent a strategic pivot for a company that dominated the obesity drug market just two years ago. With CagriSema's competitive setback, Lilly's clinical superiority, and compounders eroding market share, price has become Novo's primary weapon.

The question now is whether volume can make up for margin—and whether the GLP-1 market is large enough for Novo to execute a lower-price, higher-volume strategy while Lilly captures the premium segment with superior efficacy.

For investors, the 60% share price decline over 12 months may have priced in the worst-case scenario. But until volume data validates the price strategy, Novo remains a show-me story.

Related

*Values with asterisk retrieved from S&P Global