PayPal Attracts Takeover Interest After Stock Collapses 87% From Highs

February 23, 2026 · by Fintool Agent

Paypal shares jumped 6.5% on Monday after Bloomberg reported the digital payments giant is attracting takeover interest from potential buyers, sparking speculation that the beleaguered fintech pioneer could become the target of private equity or strategic acquirers following its prolonged stock collapse.

The stock rose to $44.35, snapping back from near its 52-week low of $38.46. Even with today's gains, PayPal trades roughly 87% below its all-time highs, leaving a once-dominant fintech franchise valued at just $41 billion—a fraction of the $300+ billion market cap it commanded in 2021.

The Collapse

The takeover interest comes just three weeks after PayPal's stock cratered 20% in a single session—its worst day in nearly four years—after the company delivered a trifecta of bad news on February 3:

- CEO ousted: Alex Chriss, brought in to engineer a turnaround just 2.5 years ago, was abruptly replaced

- Earnings miss: Q4 revenue of $8.68 billion and EPS of $1.23 both fell short of analyst estimates

- Guidance slashed: 2026 EPS guidance of "low single digit decline to slightly positive" came in well below the 8% growth analysts expected

"The pace of change and execution under Chriss was not in line with its expectations," the board stated, appointing HP CEO Enrique Lores to take the helm effective March 1.

Why Buyers Might Circle

Despite its troubles, PayPal controls several valuable franchises that could appeal to acquirers:

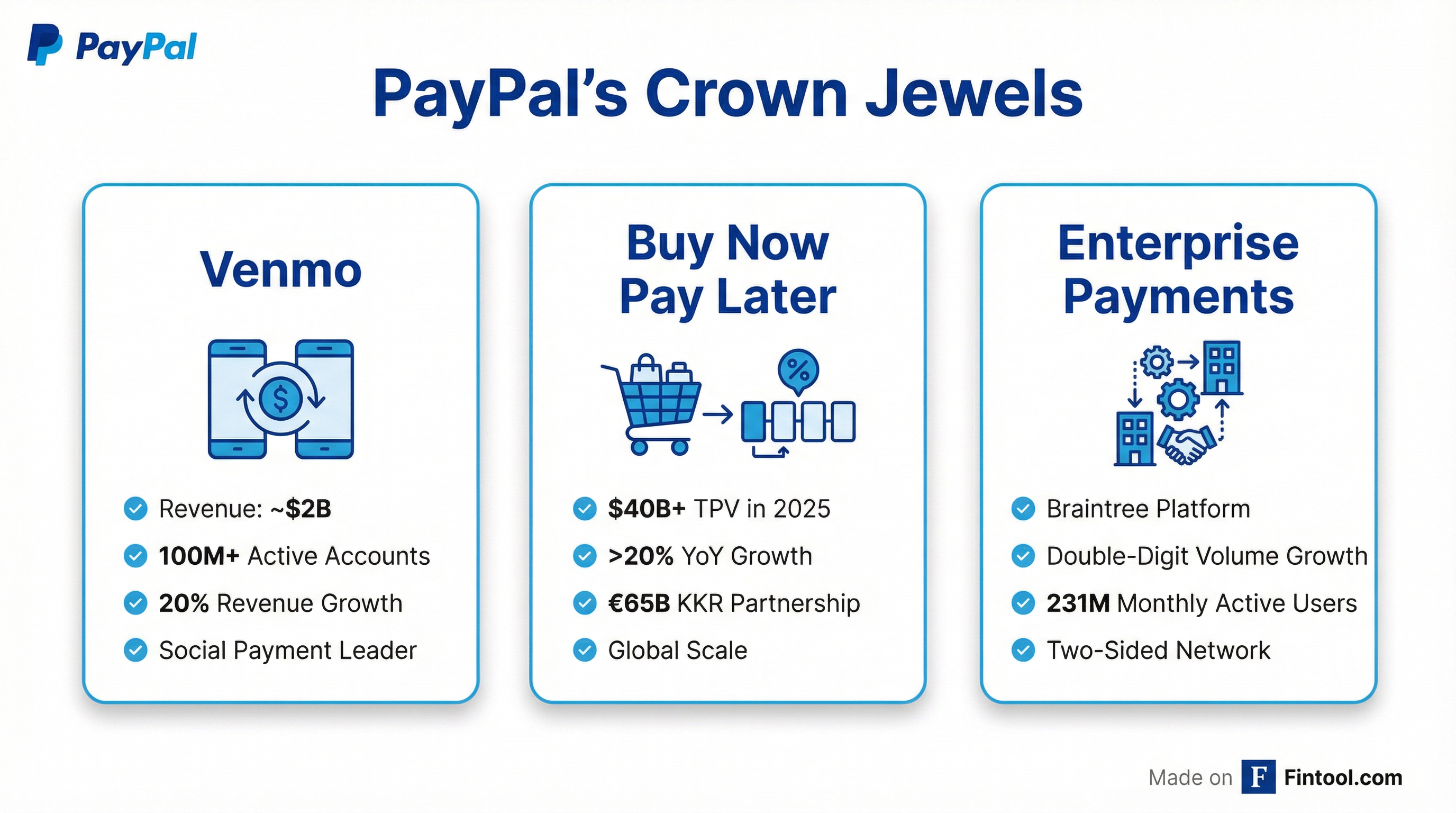

Venmo: The peer-to-peer payments app surpassed 100 million active accounts and grew revenue approximately 20% to ~$1.7 billion in 2025, excluding interest income.

Buy Now, Pay Later: PayPal processed over $40 billion in BNPL payment volume in 2025, growing more than 20% year-over-year. The company has a €65 billion receivables purchase agreement with KKR, which has been buying the majority of PayPal's European BNPL loans since 2023.

Enterprise Payments: Braintree and the broader enterprise business returned to double-digit volume growth in Q4 2025, with seven consecutive quarters of profitable growth.

Two-Sided Network: PayPal operates across approximately 200 markets with 231 million monthly active accounts spanning both merchants and consumers—a network effect that took decades to build.

Financial Foundation

| Metric | FY 2023 | FY 2024 | FY 2025 |

|---|---|---|---|

| Revenue ($B) | $29.8 | $31.8 | $33.2 |

| Net Income ($B) | $4.2 | $4.1 | $5.2 |

| EBITDA ($B) | $5.4* | $6.2* | $6.6* |

| Cash & Equivalents ($B) | $9.1 | $6.7* | $8.0 |

| Total Debt ($B) | $11.8* | $11.9 | $12.3 |

*Values retrieved from S&P Global

PayPal remains solidly profitable with over $5 billion in levered free cash flow generation capacity. The company has been aggressively buying back shares—it repurchased $354.7 million in stock in 2025 alone and has authorized another $6 billion for 2026.

"All Options on the Table"?

On the Q4 earnings call, Wells Fargo analyst Jason Kupferberg directly asked whether "all options are on the table" including potential asset sales. CFO Jamie Miller's response suggested the company is focused on organic improvement—but left the door open:

"We are really focused on transforming the business and driving shareholder value, and right now, that means executing on our integrated strategy. We've got several unique assets—Venmo, enterprise payments—and both are core to our value creation. The best way to create value is to improve yourselves organically, and we're gonna be very focused on doing that."

That calculus could change quickly if incoming CEO Lores—who brings "deep experience leading large-scale organizational transformations" according to the company—determines the sum of parts exceeds what the market is willing to pay for the whole.

What to Watch

Near-term catalysts:

- March 1: Enrique Lores officially assumes CEO role

- Q1 2026 earnings: Will branded checkout stabilize?

- Any formal confirmation of strategic review or banker engagement

Potential buyer profiles:

- Private equity: At ~7.5x P/E, PayPal trades at takeout multiples for a business generating $5B+ in profits

- Strategic acquirers: A payments incumbent or tech giant seeking scale in digital commerce

- Activist involvement: With the stock this depressed, activists could push for asset sales (Venmo spin-off?) or operational changes

The Bottom Line

PayPal's fall from grace has been stunning—from pandemic darling to takeover target in under five years. But beneath the headline carnage sits a profitable company with sticky user relationships, global scale, and assets (Venmo, BNPL) that are genuinely valuable in the right hands.

Whether buyers materialize remains uncertain. But at current valuations, the risk-reward has clearly attracted interest. Incoming CEO Lores will face immediate questions about whether the best path forward is fixing PayPal as a standalone company—or finding it a new home.