Snap Hits $1 Billion Subscription Milestone as Snapchat+ Tops 25 Million

February 18, 2026 · by Fintool Agent

Snap's direct revenue business has crossed the billion-dollar threshold, with the company announcing Wednesday that its subscription portfolio has reached a $1 billion annualized revenue run rate—driven by more than 25 million Snapchat+ subscribers. The milestone validates paid monetization in social media and comes as rival Meta prepares to test its own premium subscription offerings across Instagram, Facebook, and WhatsApp.

Shares of Snap rose 2.9% on Wednesday to close at $4.87, with aftermarket trading pushing the stock to $4.90.

From Experiment to Revenue Engine

What began as a $3.99-per-month early-access program in late 2022 has scaled into a meaningful business pillar for Snap. Subscriber growth accelerated 71% year-over-year in Q4 2025, reaching 24 million at quarter-end before surpassing 25 million this month.

"Snapchat+ has become one of the fastest-growing consumer subscription services globally, with subscriber growth every quarter," Snap said in a blog post. "What started as an early-access program for our most engaged Snapchatters has quickly scaled into a meaningful business—one that now represents a strong and growing revenue stream alongside our ads business."

The company's "Other Revenue" segment—which houses subscription revenue—grew 63% year-over-year to $745 million in fiscal 2025, up from $458 million in 2024 and just $198 million in 2023. This segment now represents approximately 13% of Snap's total annual revenue of $5.9 billion.

A Multi-Tier Subscription Strategy

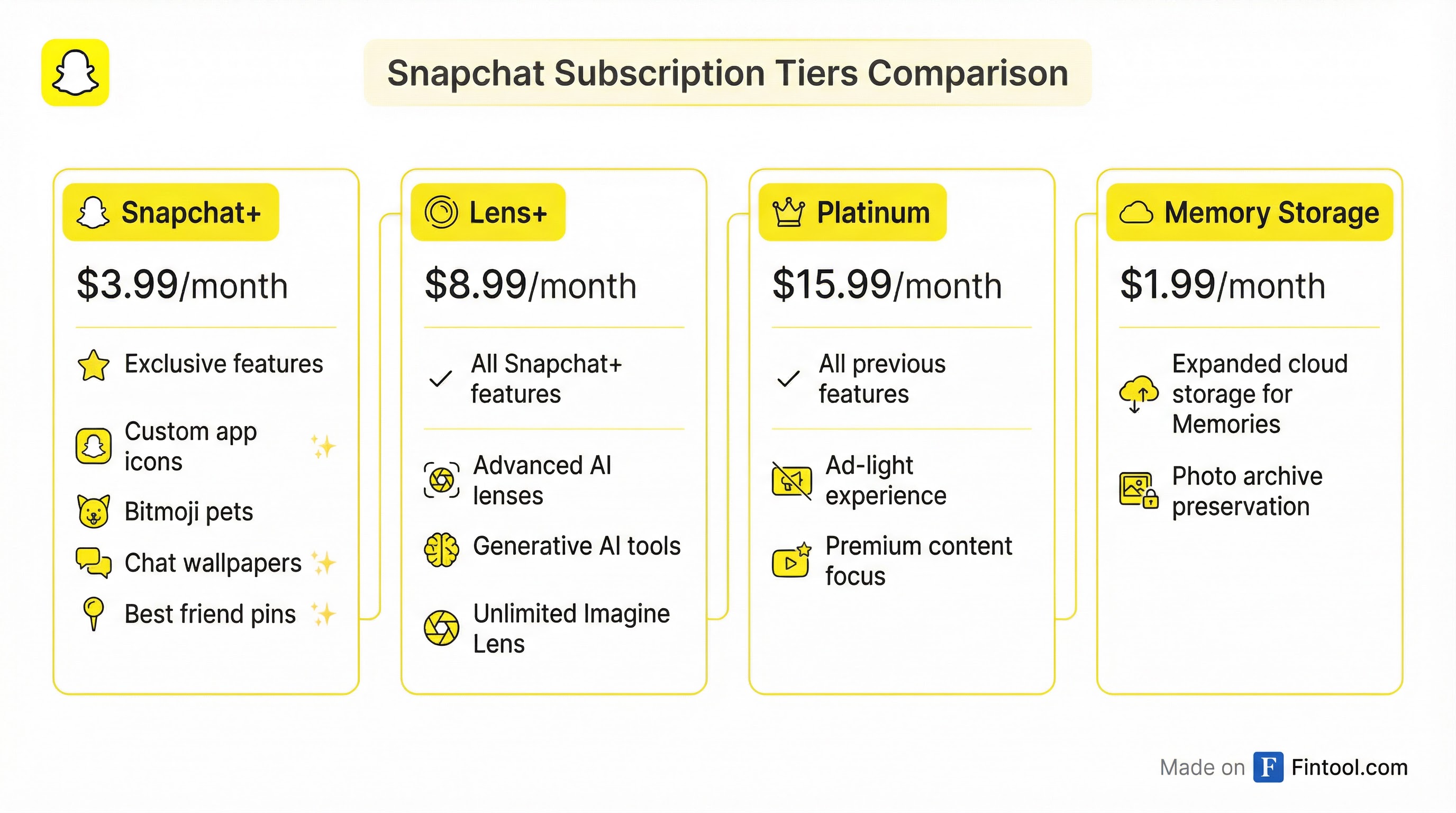

Snap has expanded well beyond the core Snapchat+ offering to create a tiered subscription ecosystem:

| Tier | Price | Key Features |

|---|---|---|

| Snapchat+ | $3.99/month | Custom icons, Bitmoji pets, chat wallpapers, best friend pins, early access to features |

| Lens+ | $8.99/month | All Snapchat+ features plus advanced AI lenses, generative AI tools, unlimited Imagine Lens |

| Platinum | $15.99/month | Ad-light experience, premium content focus |

| Memories Storage | $1.99/month | Expanded cloud storage for photo/video archive |

CEO Evan Spiegel highlighted memory storage plans as a "big driver" of recent subscriber growth, noting they've also improved retention rates.

"We've got some other great features on deck coming up this year for the direct pay segment of our business," Spiegel said on the Q4 earnings call. "So, really excited about that overall, and I think really helps support our efforts to diversify our revenue."

Snap also announced it's expanding opportunities for creators with Creator Subscriptions, a new product allowing fans to subscribe directly to creators for exclusive content, priority engagement, and an ad-free experience within creators' Stories.

Why It Matters: The Pivot to Profitability

The subscription milestone is central to Snap's "Crucible Moment" strategy, articulated by Spiegel last fall. The company is deliberately prioritizing profitable growth over raw user expansion, accepting potential headwinds to engagement in exchange for higher-margin revenue streams.

Key strategic shifts include:

- Reduced community growth marketing spend to focus resources on monetizable markets

- Cost-to-serve calibration based on each market's monetization potential

- Expanded paid features even when they create friction with free engagement

"Over the past 3 years, our community growth has really outpaced our revenue growth, and ARPU has actually declined while we've simultaneously increased the cost to serve, which has put downward pressure on our margins," Spiegel acknowledged.

The results are showing: Snap achieved a 59% gross margin in Q4 2025, approaching its near-term goal of 60%, and believes there's "a clear path to exceed this goal in 2026." The company posted net income of $45 million in Q4 2025, compared to just $9 million in Q4 2024.

| Metric | Q4 2024 | Q4 2025 | Change |

|---|---|---|---|

| Revenue | $1.56B | $1.72B | +10.2% |

| Net Income | $9.1M | $45.2M | +397% |

| Cash from Operations | $231M | $270M | +17% |

| Subscribers | 14M | 24M+ | +71% |

Meta Takes Notice

Snap's success has not gone unnoticed. In January 2026, Meta confirmed plans to test premium subscriptions for Instagram, Facebook, and WhatsApp that would unlock exclusive features and expanded AI capabilities.

Meta said the new offerings will "unlock more productivity and creativity" while keeping core services free. The company plans to integrate features from Manus, an AI agent startup it acquired for $2 billion in December, into the subscription offerings.

"Meta is taking a two-fold approach to Manus," TechCrunch reported. "The company is going to integrate Manus into Meta products, while continuing to sell standalone subscriptions to businesses."

The timing suggests Meta is responding to Snap's proof of concept. With Meta's platforms reaching billions of users—far exceeding Snap's 946 million monthly active users—even modest subscription penetration could generate substantial revenue.

What to Watch

Several catalysts could determine whether Snap maintains its subscription leadership:

Near-term:

- Specs AR glasses launch (2026) — Consumer AR could become a premium hardware extension of the subscription ecosystem

- Creator Subscriptions rollout — Could accelerate subscriber growth if creators drive adoption

- Meta subscription launch — Competitive pressure could commoditize premium social features

Longer-term:

- Regulatory environment — Age verification requirements (Snap removed 400,000 accounts in Australia in Q4) could impact user growth

- Path to 1 billion MAU — Snap is close to its goal with 946 million monthly active users, but has deliberately slowed growth marketing

For investors, the key question is whether subscription revenue can scale fast enough to offset the company's acceptance of slower user growth. At $4.87 per share and an $8.2 billion market cap, Snap trades at roughly 8x its $1 billion subscription run rate—suggesting the market is waiting to see if this pivot can deliver sustained profitability.

Related: