Starboard Pushes Riot Platforms to Accelerate AI Pivot, Sees $21 Billion Upside

February 18, 2026 · by Fintool Agent

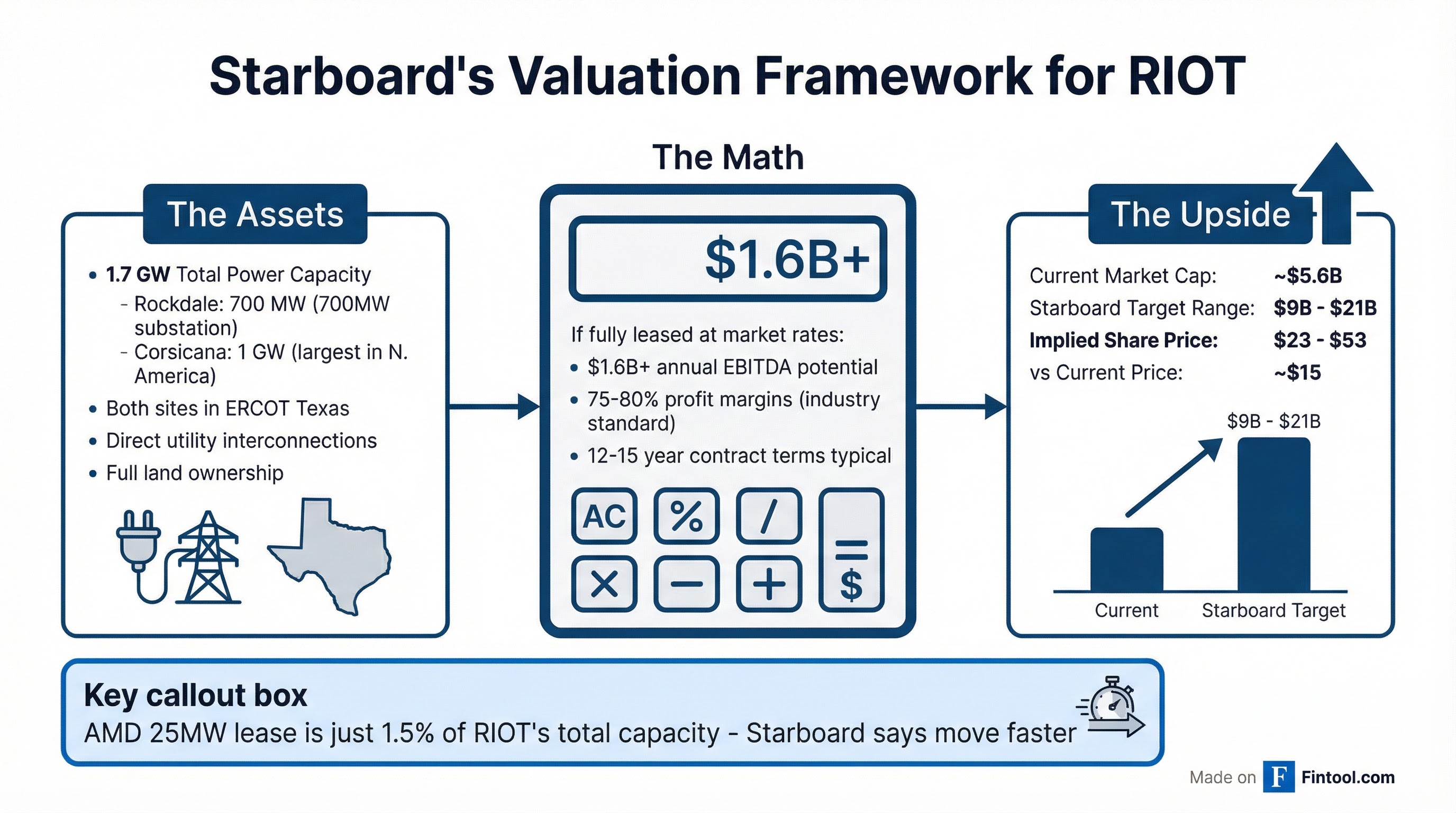

Activist investor Starboard Value is pressing Riot Platforms to move faster on AI data center deals, arguing the bitcoin miner's 1.7 gigawatts of Texas power capacity could be worth $9-21 billion—up to four times its current market value—if management accelerates execution.

Riot shares jumped approximately 5% in premarket trading following the letter's release.

The Starboard Thesis

In a letter to CEO Jason Les and Executive Chairman Benjamin Yi, Starboard Managing Member Peter Feld argued that Riot "must urgently seize this extraordinary opportunity" to capitalize on surging AI infrastructure demand.

Starboard owns approximately 12.7 million shares of Riot, making it one of the company's largest shareholders. The activist helped appoint new directors with data center experience to Riot's board last year.

The math is straightforward: If Riot monetizes its power capacity in line with recent industry transactions, Starboard estimates it could generate more than $1.6 billion in annual EBITDA. At comparable multiples to peers who have secured hyperscaler deals, that translates to an equity value of $9-21 billion—implying share prices of $23-53 versus the current ~$15.

Riot's 1.7 Gigawatt Advantage—And Why It's Underperforming

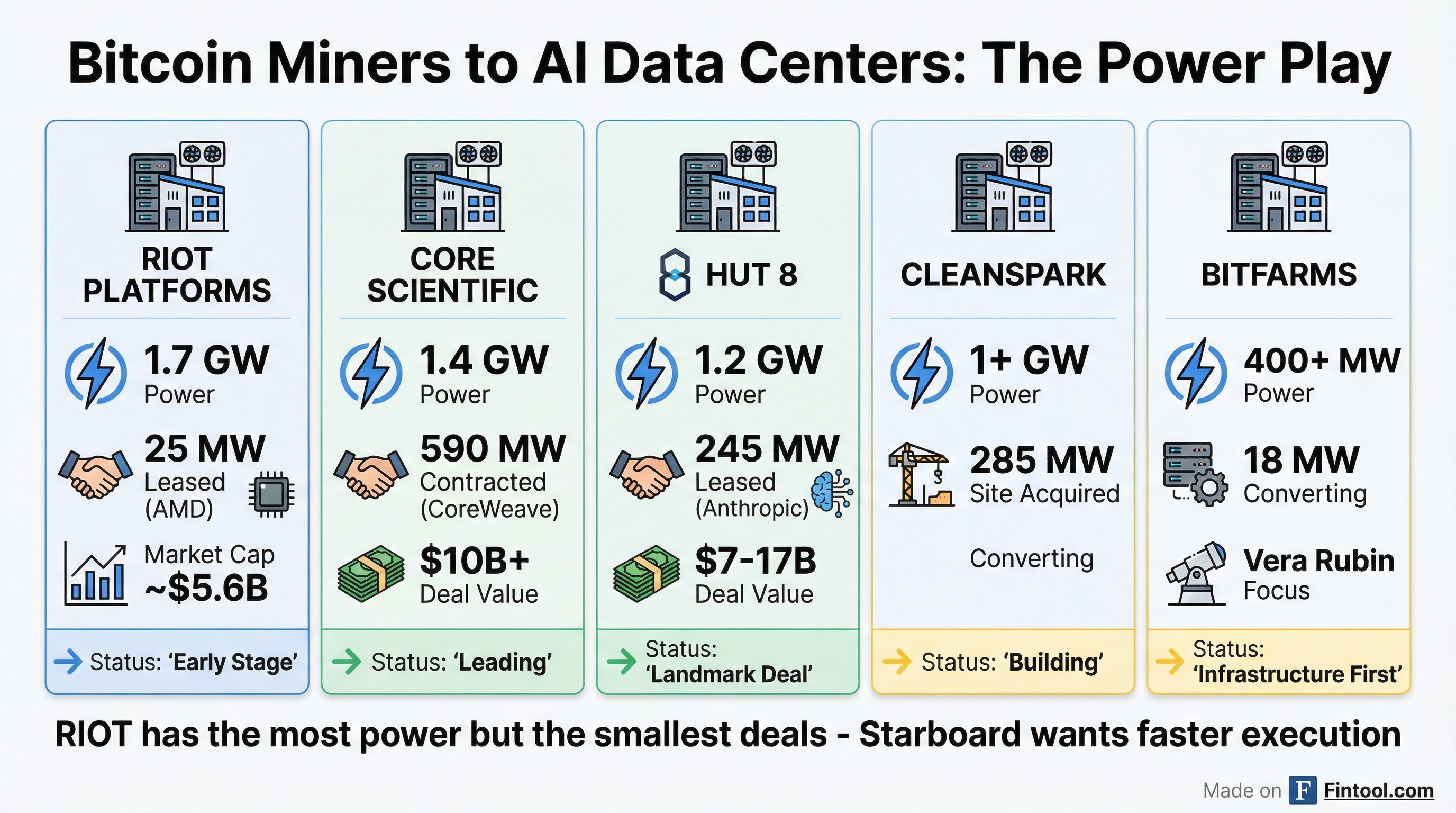

Riot controls two premier Texas sites: the Rockdale facility with 700 MW of fully approved power and the Corsicana facility with approximately 1 GW of developed capacity. Together, these represent 1.7 gigawatts of "immediately actionable" power—among the largest portfolios in the bitcoin mining industry.

Both sites feature direct, non-interruptible utility interconnections with no intermediaries, a critical advantage in a power-constrained market. Rockdale has 700 MW supported by an on-site substation, while Corsicana is positioned to be "one of the largest Bitcoin Mining facilities in North America, as measured by developed capacity."

The problem, according to Starboard: Riot has only leased 25 MW to Amd—just 1.5% of its total capacity.

| Metric | RIOT | CORZ | HUT |

|---|---|---|---|

| Total Power | 1.7 GW | 1.4 GW | 1.2 GW |

| AI/HPC Contracted | 25 MW (1.5%) | 590 MW (42%) | 245 MW (20%) |

| Major Tenant | AMD | CoreWeave | Fluidstack/Anthropic |

| Deal Value | $311M (10yr) | $10B+ (12yr) | $7-17B (15yr) |

The AMD Deal: A Starting Point, Not the Destination

In January, Riot announced its first data center lease—a 10-year agreement with AMD for 25 MW of critical IT load at Rockdale. The deal includes three five-year extension options, potentially extending the partnership to 25 years.

Key terms of the AMD lease:

- Initial capacity: 25 MW, delivered in two phases (5 MW in January, 20 MW in May 2026)

- Total contract value: $311 million over the 10-year base term

- Annual NOI: ~$25 million

- CapEx: Under $90 million (~$3.6M per IT MW vs. $10-13M industry greenfield cost)

- Expansion rights: 75 MW option + 100 MW right of first refusal = 200 MW total potential

Starboard characterized the AMD deal as a "positive signal" but "a small proof-of-concept deal." The activist wants Riot focused on "high-quality, investment-grade tenants, including hyperscalers, rather than simply chasing the highest lease rates."

To fund near-term development, Riot is selling Bitcoin from its treasury. The company sold approximately 1,080 BTC to fund the $96 million Rockdale land acquisition and plans to sell an additional ~3,134 BTC (17% of its holdings) to fund the AMD buildout and Corsicana shell development.

The Peer Gap: Why Core Scientific and Hut 8 Pulled Ahead

Riot's underperformance is stark when compared to peers who have secured transformational AI deals.

Core Scientific signed a 12-year contract with CoreWeave for approximately 590 MW of infrastructure, representing over $10 billion in revenue potential and 75-80% anticipated profit margins. The take-or-pay structure means CoreWeave is committed to paying for contracted capacity regardless of utilization, with no ability to unilaterally terminate. The company expects average annual revenue of ~$850 million from CoreWeave alone.

Hut 8 signed a landmark 15-year, triple-net lease with Fluidstack for 245 MW at its River Bend campus in Louisiana, valued at approximately $7 billion for the base term with a potential total contract value of up to $17.7 billion including renewal options. The facility will host high-performance compute clusters for Anthropic, with Google providing a financial backstop covering lease payments. HUT shares jumped 21-23% on the announcement.

Even smaller players are moving aggressively. Cleanspark secured a 285 MW site in Texas "with the explicit intent of building an AI factory for a high-quality tenant," plus a 250 MW site in Sandersville, Georgia with "immediate opportunity to host a large-scale tenant."

Bitfarms is taking a different approach—waiting for higher rates while building infrastructure for NVIDIA's next-generation Vera Rubin GPUs. "With Vera Rubin GPUs expected to begin shipping in Q4 of 2026 and the infrastructure requirements to support them largely incompatible with facilities designed for Blackwell GPUs, we believe Vera Rubin infrastructure will be in the greatest demand and shortest supply in 2027," CEO Ben Gagnon said.

What Management Says

Riot management has touted the AMD deal as validation of its execution capabilities and a foundation for larger partnerships.

"This transaction is the foundation that establishes Riot as the partner of choice for leading data center tenants," CEO Jason Les said in January. "The speed, flexibility, and capital efficiency we demonstrated with AMD—namely customizing infrastructure to their specific needs, providing a rapid path to quickly energize 25 IT megawatts, and providing a clear path to 200 megawatts of expansion—makes Riot uniquely attractive to demanding tenants."

The company has also aligned executive compensation with the data center strategy. Effective January 1, 2026, Riot's Compensation Committee eliminated the "Bitcoin Yield" metric from its annual incentive plan "as it no longer reflects a primary key performance indicator." New metrics include "Data center revenue" (15% weighting) and "Data Center NOI" (15% weighting).

Management has outlined a potential $1.6-$2.1 billion in annualized NOI upon full buildout of its 1.2 GW of potential critical IT load capacity. But the question—and Starboard's core critique—is timing.

The Consolidation Risk

Starboard's letter carries an implicit threat: move faster, or become a target.

The activist noted that Riot could "draw consolidation interest" if it fails to capitalize quickly on AI infrastructure demand. In an industry where power is the scarce resource, Riot's 1.7 GW portfolio makes it an attractive acquisition candidate for well-capitalized tech companies or infrastructure investors.

The bitcoin mining sector has already seen significant consolidation. CoreWeave, which now has ~$30 billion in AI infrastructure contracts across multiple providers, proposed acquiring Core Scientific in October 2025 before the deal was rejected. Microsoft, Amazon, and Google have all been expanding data center partnerships with power-rich operators.

What to Watch

Near-term catalysts for Riot:

- Hyperscaler lease announcements beyond AMD

- Corsicana Tier 3 core and shell development progress

- Project financing terms for the AMD buildout

- Q4 earnings (expected late February) with data center pipeline updates

Industry benchmarks:

- Monthly lease rates per MW (current market: $15-25k/MW for AI-ready capacity)

- Financing terms (80% loan-to-cost becoming standard for investment-grade tenants)

- Time-to-energize (Core Scientific targeting 590 MW by early 2027)

Starboard's campaign puts pressure on Riot to accelerate what management has called its "ongoing evolution into a leading digital infrastructure platform." The activist's math suggests enormous value creation potential—if execution catches up to the opportunity.

Related Company Profiles: