Westlake CFO Steve Bender to Retire After 19 Years as Company Navigates Chemical Trough

February 23, 2026 · by Fintool Agent

Westlake Corporation is losing the financial architect who guided it through nearly two decades of transformation—from a regional chemical company to a diversified $12 billion enterprise—at a moment when his successor will inherit one of the most challenging operating environments in the company's history.

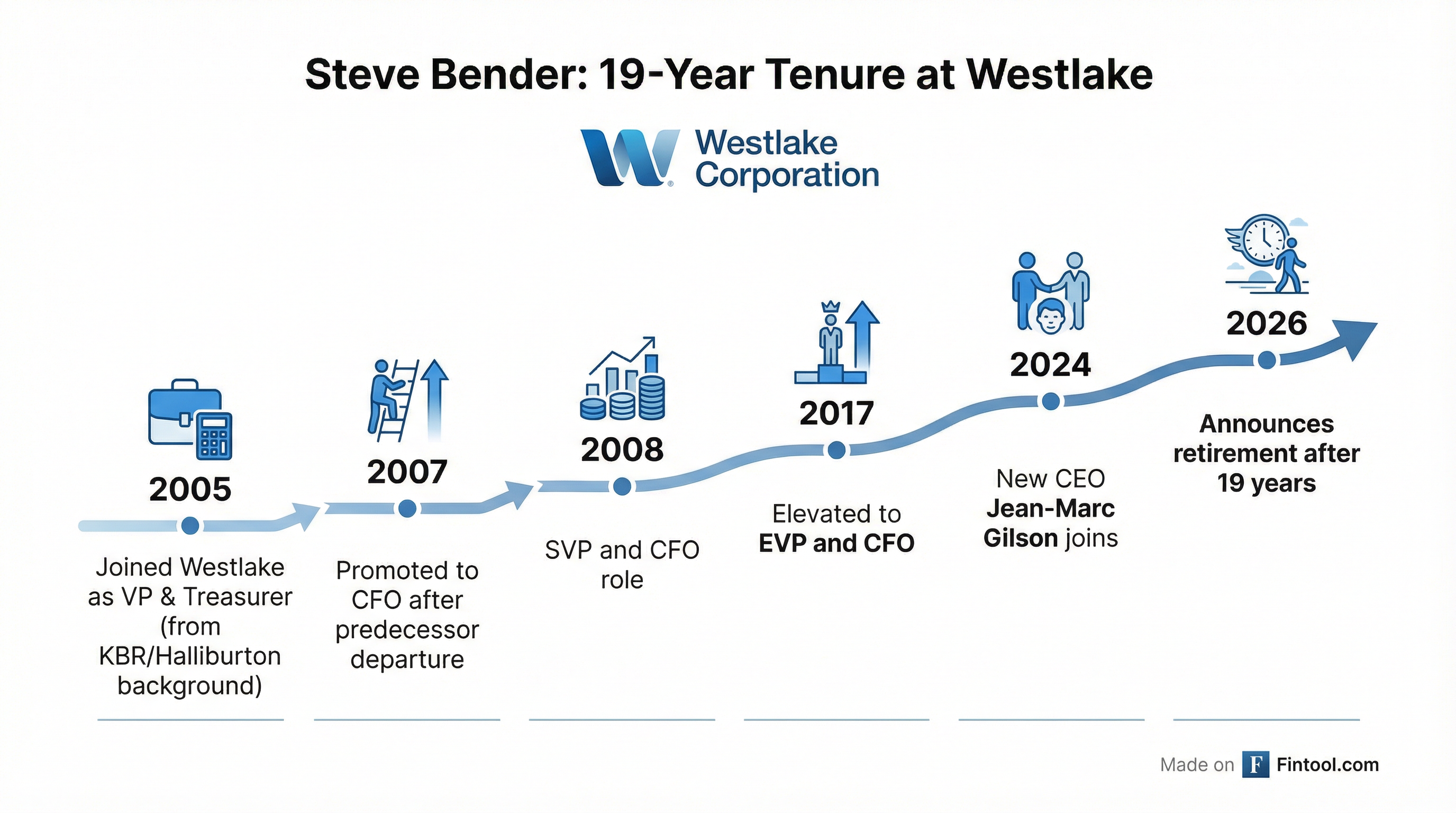

M. Steven Bender, 69, announced his intention to retire as Executive Vice President and Chief Financial Officer on February 19, effective upon the appointment of his successor . The departure comes just eight months after the Chao family implemented its first-ever CEO succession plan, handing the reins to Jean-Marc Gilson, a seasoned chemicals industry executive who now joins the board alongside former Lyondellbasell CEO Bob Patel .

The timing is notable: Bender's exit arrives as Westlake faces a prolonged trough in its Performance and Essential Materials (PEM) segment, mounting quarterly losses, and an S&P credit downgrade to BB with a negative outlook. The company is expected to report a loss of $1.40 per share when it announces Q4 results on February 24—the fourth consecutive unprofitable quarter .

A Two-Decade Legacy

Bender joined Westlake in 2005 as Vice President and Treasurer, bringing treasury and financial management experience from KBR (a Halliburton subsidiary) and Texas Eastern Corporation . He was promoted to CFO in February 2007 after his predecessor departed for another public company, and subsequently elevated to Senior Vice President (2008) and Executive Vice President (2017).

During his tenure, Westlake transformed from a primarily ethylene and polymer producer into a diversified materials company. The 2016 acquisition of Axiall Corporation for $3.8 billion added chlor-alkali and building products capabilities, while the 2022 purchase of Boral Industries' North American business for $2.15 billion expanded its Housing and Infrastructure Products (HIP) segment into roofing and stone veneer.

The financial results speak to the transformation: annual revenue grew from approximately $2.8 billion in 2007 to $12.1 billion in FY 2024 , while net income peaked at $2.25 billion in FY 2022 during the post-pandemic commodity supercycle.

| Metric | FY 2021 | FY 2022 | FY 2023 | FY 2024 |

|---|---|---|---|---|

| Revenue | $11.8B | $15.8B | $12.5B | $12.1B |

| Net Income | $2.0B | $2.2B | $479M | $602M |

| Total Debt | $5.7B | $5.5B | $5.6B | $5.4B |

| Cash | $1.9B | $2.2B | $3.3B | $2.9B |

Values from S&P Global

The Chemicals Trough Deepens

Bender's final months have been marked by an unforgiving operating environment. Westlake's PEM segment—which includes polyethylene, PVC, and chlor-alkali—has been battered by overcapacity, weak global manufacturing activity, and compressed margins.

The numbers are stark: Westlake posted net losses of $40 million in Q1 2025 , $142 million in Q2 2025 , and a staggering $782 million loss in Q3 2025 . EBITDA margins collapsed from 21% in Q2 2024 to below 10% by Q3 2025.*

| Quarter | Revenue | Net Income | EBITDA | EBITDA Margin |

|---|---|---|---|---|

| Q2 2024 | $3.21B | $313M | $689M* | 21.5%* |

| Q3 2024 | $3.12B | $108M | $536M* | 17.2%* |

| Q4 2024 | $2.84B | $7M* | $202M* | 7.1%* |

| Q1 2025 | $2.85B | ($40M) | $258M | 9.1%* |

| Q2 2025 | $2.95B | ($142M) | $301M* | 10.2%* |

| Q3 2025 | $2.84B | ($782M) | $281M* | 9.9%* |

Values from S&P Global

On the Q4 2024 earnings call, Bender defended the company's position, noting that "an investor today is actually getting the PEM side of the business, frankly, for free" given Westlake's valuation relative to its HIP segment earnings . He pointed to upcoming price initiatives and argued the market was "underestimating the earnings leverage that we have in the PEM side of the business" .

That leverage cuts both ways. S&P Global downgraded Westlake to BB in early 2026, citing expectations that "FFO to debt will remain below 30% over at least the next few quarters due to the weaker demand and margins in its PEM segment" .

Board Refresh Signals Strategic Intent

The simultaneous board appointments suggest Westlake is preparing for a more active phase of capital deployment and strategic repositioning.

Bob Patel brings unmatched petrochemical credibility. As LyondellBasell's CEO from 2015-2022, he led one of Westlake's largest competitors through the same commodity cycles . His subsequent roles at Standard Industries and W.R. Grace demonstrate experience with building materials—directly relevant to Westlake's HIP segment. Patel will serve on the Audit, Compensation, Corporate Risk and Sustainability, and Nominating and Governance committees .

Jean-Marc Gilson's board seat formalizes what had been an unusual arrangement: an outside CEO without board representation. Executive Chairman Albert Chao noted that "his presence on the board is expected to further enhance communication and strategic alignment between management and the board" .

The 14-member board now includes deeper chemicals expertise at a time when the company is actively pursuing M&A. On recent calls, Bender indicated "good dialogue" with asset owners looking to divest, with a bias toward HIP acquisitions that would generate "stronger, earlier contribution" than PEM deals .

Cost Cuts and Restructuring Ahead

CEO Gilson has outlined aggressive cost reduction targets: $150-175 million in savings by end of 2025, with an additional $200 million targeted by 2026 . The company plans to close its Pernis facility in the Netherlands in 2026 to improve profitability.

Bender's final guidance called for maintaining the $0.53 quarterly dividend and preserving the company's investment-grade rating—though S&P's downgrade to BB has technically moved Westlake below that threshold .

His departure leaves approximately $5.8 million in Westlake stock on the table. SEC filings show Bender holds roughly 61,842 shares directly, with recent transactions limited to routine RSU vesting and tax withholding—no significant open-market sales.

| Recent Insider Activity | Date | Type | Shares | Price |

|---|---|---|---|---|

| RSU Vesting | Feb 19, 2026 | Award | 1,777 | $0 |

| Tax Withholding | Feb 20, 2026 | Disposition | 445 | $94.10 |

| RSU Conversion | Feb 17, 2026 | Exercise | 4,751 | $0 |

| Tax Withholding | Feb 18, 2026 | Disposition | 1,209 | $98.95 |

What to Watch

Tomorrow's earnings call (February 24) will be Bender's final as CFO. Investors will press for:

- Timeline and criteria for CFO search

- Updated cost reduction progress

- Q4 results and FY 2026 guidance

- PEM pricing trajectory and demand signals

- M&A pipeline activity

Consensus estimates show Wall Street expecting a rough near-term but gradual recovery:

| Metric | FY 2025E | FY 2026E | FY 2027E |

|---|---|---|---|

| Revenue | $11.2B* | $11.2B* | $11.8B* |

| EPS | ($2.24)* | $0.72* | $2.38* |

| Target Price | $85.79* | — | — |

Estimates from S&P Global

The analyst community remains cautiously positioned. Mizuho downgraded WLK from Buy to Hold on February 9, noting the stock had "rallied approximately 60% from November lows despite the weakening outlook" . The mean price target of $85.79 implies roughly 8% downside from Friday's close of $93.02.

Bender's successor will inherit a company at an inflection point: a strong balance sheet with $2.9 billion in cash , a recession-resistant building products business, but a chemicals segment still searching for a bottom. The board refresh with Patel and Gilson suggests Westlake is positioning for opportunistic moves—whether that means acquisitions, further restructuring, or the segment separation that analysts have periodically floated.

For now, the man who helped build Westlake into a $12 billion enterprise is stepping back. The next CFO will have to navigate the other side of the cycle.

Related: