Earnings summaries and quarterly performance for MICROCHIP TECHNOLOGY.

Executive leadership at MICROCHIP TECHNOLOGY.

Board of directors at MICROCHIP TECHNOLOGY.

Research analysts who have asked questions during MICROCHIP TECHNOLOGY earnings calls.

Blayne Curtis

Jefferies Financial Group

9 questions for MCHP

Vivek Arya

Bank of America Corporation

9 questions for MCHP

Harlan Sur

JPMorgan Chase & Co.

8 questions for MCHP

Harsh Kumar

Piper Sandler & Co.

7 questions for MCHP

Joshua Buchalter

TD Cowen

6 questions for MCHP

Timothy Arcuri

UBS

6 questions for MCHP

Vijay Rakesh

Mizuho

6 questions for MCHP

William Stein

Truist Securities

6 questions for MCHP

Chris Caso

Wolfe Research LLC

5 questions for MCHP

Tore Svanberg

Stifel Financial Corp.

5 questions for MCHP

Christopher Rolland

Susquehanna Financial Group

4 questions for MCHP

James Schneider

Goldman Sachs

4 questions for MCHP

Janet Ramkissoon

Quadra Capital

4 questions for MCHP

Joseph Moore

Morgan Stanley

4 questions for MCHP

Christopher Caso

Wolfe Research

3 questions for MCHP

Christopher Danely

Citigroup Inc.

3 questions for MCHP

Quinn Bolton

Needham & Company, LLC

3 questions for MCHP

Chris Danely

Citi

2 questions for MCHP

Chris Stanley

Citi

2 questions for MCHP

Craig Ellis

B. Riley Securities

2 questions for MCHP

Joe Quatrochi

Wells Fargo

2 questions for MCHP

Matthew Prisco

Cantor Fitzgerald

2 questions for MCHP

Toshiya Hari

Goldman Sachs Group, Inc.

2 questions for MCHP

Chris Casso

Wolfe Research

1 question for MCHP

Joe Moore

Morgan Stanley

1 question for MCHP

Recent press releases and 8-K filings for MCHP.

- Management guides March-quarter revenue up 6.2% sequentially at the midpoint, citing normalized distribution inventory and continued end-customer destocking.

- Inventory sits at 200 days, with a target of 130–150 days; underutilization charges were $51 million in the December quarter and will unwind gradually over the next two years.

- Reiterates a 65% long-term gross-margin target, with 400 bps of improvement remaining, driven by better fab utilization and higher-margin products like PCIe Gen6, FPGA, and Ethernet switches.

- Highlights four PCIe Gen6 design wins (one > $100 million / year) and growth in precision timing, data-center power-management controllers, FPGA, and edge-AI software offerings.

- Commits to maintaining the dividend and using all excess free cash flow to pay down debt, following last March’s mandatory convertible preferred issuance to preserve investment-grade status.

- Microchip guided March quarter revenue up 6.2% sequentially; distribution inventory variance has collapsed from $100 m to $12 m, but total days inventory remains at 200 days versus a 130–150 days target

- Company targets a 65% long-term gross margin; Q3 midpoint is 61% non-GAAP, with $51 m of underutilization charges in the Dec quarter that require growth in internally produced products to improve fab utilization

- Data center momentum led by 3 nm PCIe Gen6 switch wins (4 confirmed, including one > $100 m annual spend) and imminent retimer launches; additional drivers include precision timing, security compute, digital power, and cesium clocks

- Capital allocation: dividend flat-lined, with 100% of excess free cash applied to debt reduction; net leverage remains elevated post-acquisitions and mandatory convertible preferred issuance to preserve investment-grade status

- Microchip guiding Q3 revenue up 6.2% sequentially on strong product momentum and inventory normalization.

- Distribution inventory has been cleaned up, with the distributor sell-in/through gap narrowing from ~$100 M to $12 M, while end-customer destocking continues to normalize.

- Long-term non-GAAP gross margin target remains 65%, with a 61% midpoint this quarter and 400 bps of upside from mix tailwinds in data center, PCIe Gen6 and FPGA products.

- Microchip is the only vendor with a 3 nm PCIe Gen6 switch, securing four design wins (one > $100 M/year) and planning a Gen7 release within 12 months.

- Rolling out a unified edge AI software/SaaS suite across MCUs and FPGAs, demonstrated by a 15% battery-life boost in a power drill via ML models without new hardware.

- On February 9, 2026, Microchip Technology announced its intention to offer $600 million aggregate principal amount of convertible senior notes due 2030 in a private placement to qualified institutional buyers under Rule 144A, with an option for initial purchasers to acquire up to an additional $90 million.

- The notes will be senior, unsecured obligations bearing interest semi-annually in arrears, with the interest rate, conversion rate and other terms to be determined at pricing; upon conversion, Microchip may pay cash up to the principal amount and cash, shares or a combination thereof for the remainder.

- Microchip expects to use a portion of the net proceeds to fund capped call transactions and the remainder to repay outstanding commercial paper.

- J. Wood Capital Advisors, serving as financial advisor, intends to purchase up to $25 million of common stock concurrently with the offering, and capped call transactions are intended to reduce dilution on note conversion.

- Microchip reported that channel inventory has largely normalized, with December quarter book-to-bill above 1 and March quarter revenue guidance of +6.2%, exceeding the typical 2–3% seasonal growth forecast.

- Data center now represents 19% of FY revenue, driven by high-speed connectivity products including 3nm PCIe Gen6 switches, flash controllers, and HDD controllers.

- Automotive growth is increasingly driven by transitioning from legacy CAN to Ethernet (10BASE-T1S), PCIe switching, and the new Automotive SerDes Alliance (ASA) standard, positioning Microchip for long-cycle in-vehicle networking wins.

- The company reiterated a path to 65% gross margin, targeting a ~50 bps improvement in the March quarter and steady progress through calendar year 2026.

- With net debt/EBITDA at 4.18×, priority is on debt reduction and sustaining the dividend; no share buybacks are planned in the near term.

- Distribution normalized with $12 M sell-through/sell-in gap and book-to-bill >1, driving 6.2% QoQ growth guidance for March vs. typical 2–3%

- Data center accounts for ~19% of FY revenue, led by 3 nm Gen6 PCIe switches, flash controllers and HDD controllers—supporting both scale-up and scale-out deployments

- Automotive expansion beyond MCUs into touch controllers, car-access solutions and in-vehicle networking (CAN, LIN, MOST, 10BASE-T1S Ethernet) plus ASA standard and PCIe switches

- Manufacturing footprint is 37–40% internal/60% external; advanced-node lead times and substrate tightness create $50–51 M underutilization headwind, with gradual fab-loading planned toward a 65% gross-margin target

- Financial priorities: March quarter gross margin guided at 61% (+50 bps QoQ); net debt/EBITDA at 4.18×, focusing on debt paydown, dividend sustained and no buybacks near term

- Distribution channel largely normalized with a $12 million sell-in/sell-through gap, booking momentum with book-to-bill > 1, and 6.2% Q2-FY26 revenue growth guidance versus a typical 2–3% seasonal uptick.

- Data center now represents ~19% of FY2025 revenue, led by PCIe Gen 6 switches for high-speed connectivity and supporting flash/HDD controllers; FPGA sales are also expanding across defense, industrial, auto, and data center markets.

- Automotive is broadening beyond MCUs into in-vehicle networking (10BASE-T1S Ethernet, PCIe switches, Automotive SerDes Alliance), car-access systems, and touch interfaces, positioning connectivity as a key growth driver.

- Financial priorities shifted to debt reduction (net debt/EBITDA at 4.18x) with dividends maintained and share buybacks deferred; gross margin projected to improve toward 65% by next calendar year through mix and factory utilization gains.

- $800 M Offering: Microchip upsized its private Rule 144A offering of Convertible Senior Notes due 2030 from $600 M to $800 M, expected to settle on February 11, 2026, generating approximately $785.1 M in net proceeds.

- Terms: The notes are senior, unsecured, bear no regular interest or accretion, mature on February 15, 2030, and are redeemable at par starting February 20, 2029 under specified conditions.

- Conversion: Initial conversion rate of 9.5993 shares per $1,000 principal (≈$104.17 per share), representing a 40% premium to the February 9, 2026 closing price of $74.41.

- Use of Proceeds: Approximately $60.5 M allocated to capped call transactions; remaining net proceeds to repay commercial paper.

- Microchip intends a private offering of $600 million in Convertible Senior Notes due 2030, with an initial purchaser option for an additional $90 million.

- The notes will be senior, unsecured obligations with semi-annual interest payments; final interest and conversion terms to be set at pricing.

- Net proceeds will fund capped call transactions to limit dilution and repay outstanding commercial paper.

- J. Wood Capital Advisors LLC plans to purchase up to $25 million of common stock concurrently, while option counterparties will hedge via share purchases and derivatives, potentially affecting market price.

- The offering is exclusively to qualified institutional buyers under Rule 144A and the notes (and any shares upon conversion) are unregistered.

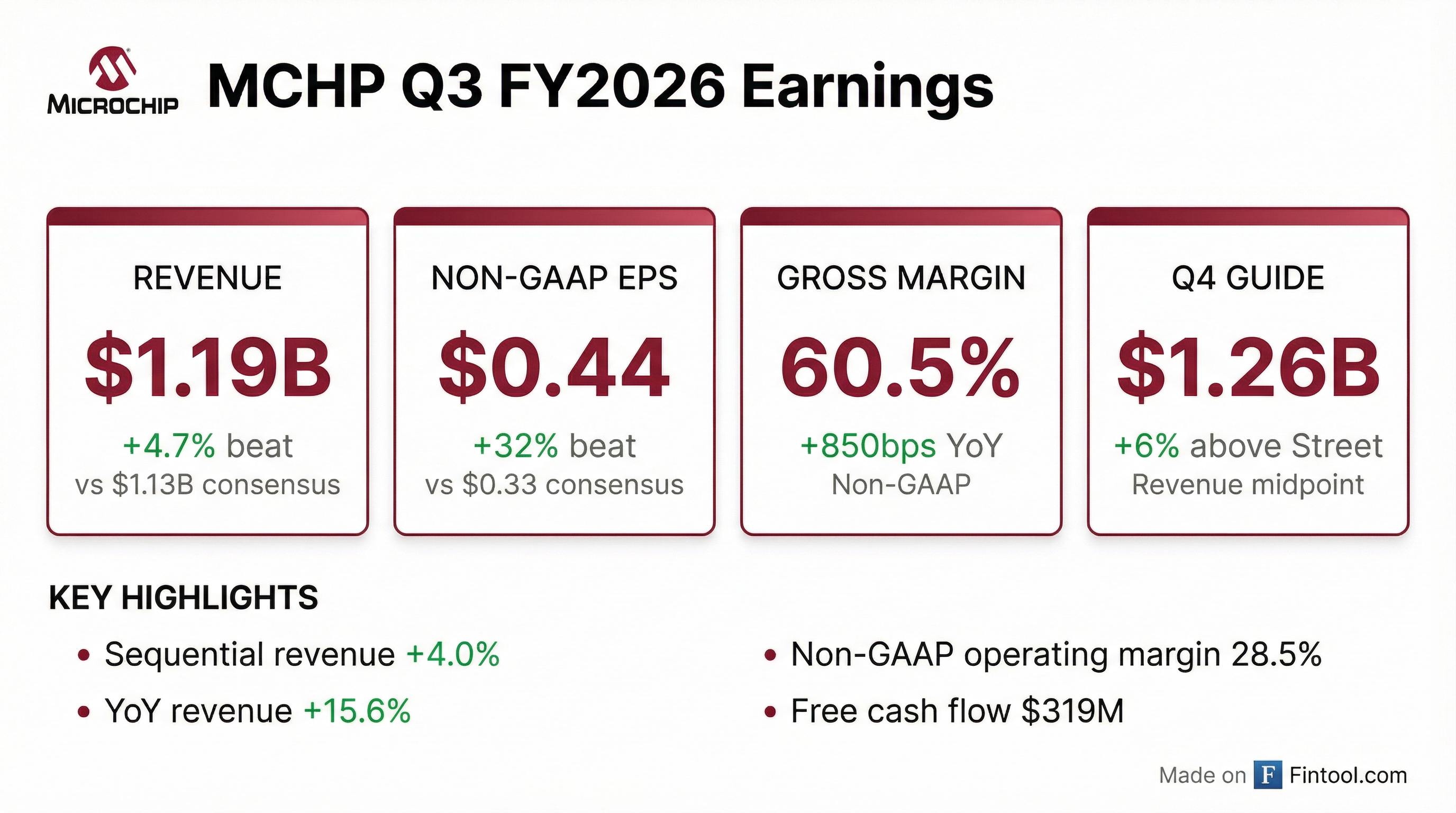

- Net sales were $1.186 billion, up 4% sequentially and 15.6% year-over-year; non-GAAP gross margin was 60.5% and non-GAAP EPS was $0.44.

- Operating cash flow was $341.4 million and adjusted free cash flow was $305.6 million; net debt to adjusted EBITDA improved to 4.18×.

- Q4 FY2026 guidance: net sales of $1.26 billion ± $20 million (+6.2% seq, +29.8% YoY), non-GAAP EPS of $0.48–$0.52, and gross margin of 60.5–61.5%.

- Announced three design wins for its Gen 6 PCIe switch, including a >$100 million revenue opportunity in calendar 2027.

Quarterly earnings call transcripts for MICROCHIP TECHNOLOGY.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more