Earnings summaries and quarterly performance for MCKESSON.

Executive leadership at MCKESSON.

Brian Tyler

Chief Executive Officer

Britt Vitalone

Executive Vice President and Chief Financial Officer

LeAnn Smith

Executive Vice President and Chief Human Resources Officer

Michele Lau

Executive Vice President and Chief Legal Officer

Thomas Rodgers

Executive Vice President and Chief Strategy and Business Development Officer

Board of directors at MCKESSON.

Bradley Lerman

Director

Deborah Dunsire

Director

Dominic Caruso

Director

Donald Knauss

Independent Chair of the Board

James Hinton

Director

Julie Gerberding

Director

Kathleen Wilson-Thompson

Director

Kevin Ozan

Director

Lynne Doughtie

Director

Maria Martinez

Director

Roy Dunbar

Director

Research analysts who have asked questions during MCKESSON earnings calls.

Charles Rhyee

TD Cowen

8 questions for MCK

Daniel Grosslight

Citigroup

8 questions for MCK

Eric Percher

Nephron Research

8 questions for MCK

Lisa Gill

JPMorgan Chase & Co.

8 questions for MCK

Allen Lutz

Bank of America

7 questions for MCK

Elizabeth Anderson

Evercore ISI

7 questions for MCK

Erin Wright

Morgan Stanley

7 questions for MCK

George Hill

Deutsche Bank

7 questions for MCK

Kevin Caliendo

UBS

7 questions for MCK

Brian Tanquilut

Jefferies

6 questions for MCK

Michael Cherny

Leerink Partners

6 questions for MCK

Stephen Baxter

Wells Fargo

3 questions for MCK

Eric Coldwell

Robert W. Baird & Co.

2 questions for MCK

Stephen Baxter

Wells Fargo & Company

2 questions for MCK

Steven Valiquette

Mizuho

2 questions for MCK

Glenn Santangelo

Barclays

1 question for MCK

Glen Santangelo

Jefferies

1 question for MCK

Recent press releases and 8-K filings for MCK.

- Gold surged to $5,552/oz as central banks added 755 tonnes to reserves

- G7 issued formal guidance treating quantum threats to current encryption as a systemic concern

- FDA cleared a record 295 AI-powered medical devices in 2025, highlighting regulatory momentum

- The functional wellness market is accelerating toward $179 billion as consumers shift to precision delivery formats

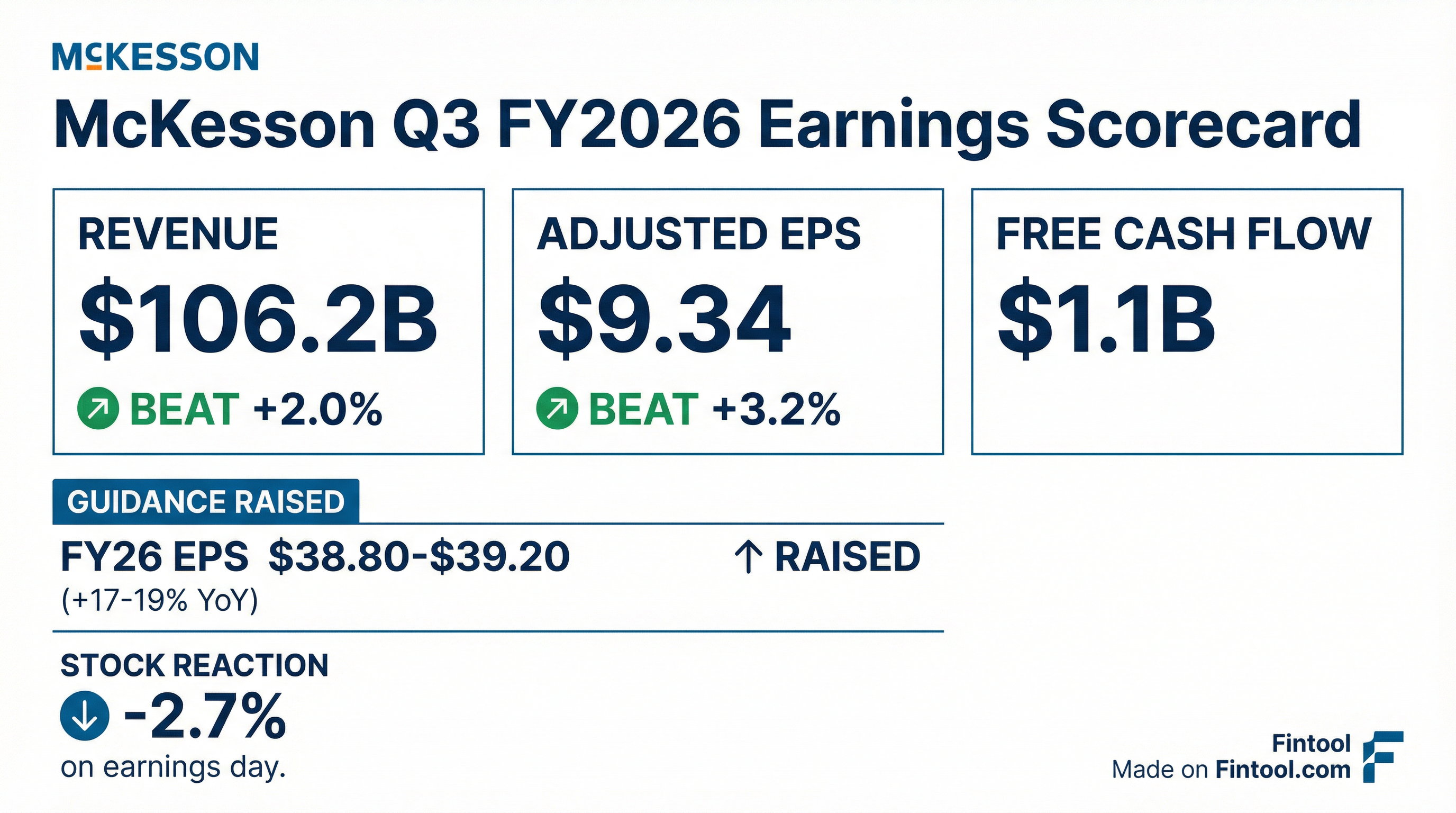

- Consolidated revenues of $106.2 billion, up 11% YoY; adjusted EPS of $9.34, up 16% YoY

- Raised FY2026 EPS guidance to $38.80–$39.20 (+17–19%) and revenue growth outlook to 12–16%

- North American Pharma revenue of $88.3 billion (+9%), including $14 billion in GLP-1 distribution (+26%); oncology & multispecialty revenue $13 billion (+37%); prescription technology solutions revenue $1.5 billion (+9%)

- Q3 free cash flow of $1.1 billion (TTM $9.6 billion); returned $781 million to shareholders via $680 million in share repurchases and $101 million in dividends

- Completed divestiture of Norway operations and advanced separation of the medical-surgical business, targeting IPO in H2 2027

- McKesson delivered $106.2 billion in consolidated revenue, up 11% y/y, and $9.34 EPS, up 16% y/y in Q3 2026.

- Oncology & multispecialty segment revenues rose 37% to $13 billion, with operating profit up 57% to $366 million; Prism Vision and Core Ventures added ~13% to segment revenue growth.

- Completed divestiture of Norway retail and distribution businesses on January 30, 2026, contributing $0.05 to adjusted EPS via held-for-sale accounting.

- Raised fiscal 2026 adjusted EPS guidance to $38.80–$39.20 (+17%–19%), revenue growth to 12%–16%, and operating profit growth to 13%–17%.

- Returned $781 million to shareholders in Q3 (including $680 million in share repurchases and $101 million in dividends); Q3 free cash flow was $1.1 billion.

- McKesson raised its fiscal 2026 EPS guidance to $38.80–$39.20, expecting 12–16% revenue growth and 13–17% operating profit growth.

- Q3 performance underpins segment outlook: North American Pharma revenue up 10–14%, Oncology & Multispecialty revenue up 29–33%, and Prescription Technology Solutions revenue up 9–13%.

- Investments in automation and AI improved productivity, with each full-time employee supporting 120 more patients in the annual verification season and a 75% reduction in escalated Drug Supply Chain Security Act inquiries.

- Portfolio actions advance: transition service agreements in place for the Medical-Surgical separation with an IPO targeted by H2 2027, and the Norwegian business divestiture completed, marking full exit from Europe.

- Revenue: Q3 FY 2026 revenue of $106.2 billion, up 11% year-over-year.

- Adjusted EPS: Q3 FY 2026 adjusted earnings per diluted share of $9.34, a 16% increase YoY.

- Guidance Update: Raised and narrowed fiscal 2026 adjusted EPS outlook to $38.80–$39.20, implying 17–19% growth.

- Segment Performance: North American Pharmaceutical revenue of $88.3 billion, +9% ; Oncology & Multispecialty revenue of $13.0 billion, +37%.

- Strategic Update: Closed sale of Norway retail and distribution businesses, fully exiting European operations.

- Third-quarter revenue of $106.2 billion, up 11% year-over-year.

- Adjusted EPS of $9.34, a 16% increase versus prior year.

- Cash flow from operations of $1.2 billion and Free Cash Flow of $1.1 billion generated in the quarter.

- Raised fiscal 2026 adjusted EPS guidance to $38.80–$39.20, implying 17–19% growth.

- McKesson reaffirmed its long-term financial targets of 13%–16% adjusted EPS growth, driven by 5%–8% North America distribution, 13%–16% oncology/multispecialty, and 10%–13% biopharma services growth.

- Fiscal 2026 guidance includes $38.35–$38.85 adjusted EPS, 12%–16% adjusted operating profit growth, and 16%–18% EPS growth versus prior year.

- The company plans ~$2.5 billion in share repurchases for fiscal 2026, with over $6 billion of authorization remaining as of September 2025.

- Integration of Florida Cancer Specialists and Core Ventures is on track, with year-one accretion of $0.40–$0.60 and $1.40–$1.60 by year three.

- McKesson has delivered a 5-year Adjusted EPS CAGR of 18% and targets 13%–16% long-term Adjusted EPS growth, driven by its strategic priorities in oncology, biopharma services, and North American distribution.

- The oncology platform spans 3,300 providers, treats 1.4 million patients, operates in a $115 billion market, and anticipates oncology drug spend to grow 60% over five years.

- Its biopharma services business enabled 100 million patient transactions, generated $10 billion in out-of-pocket savings, and prevented 12 million prescription abandonments last year via connectivity to 1 million providers and 50,000 pharmacies.

- For fiscal 2026, McKesson expects Adjusted EPS of $28.35–$28.85, 12%–16% adjusted operating profit growth, 16%–18% EPS growth, and plans $2.5 billion in share repurchases with $6 billion of authorization remaining.

- McKesson delivered an 18% adjusted EPS CAGR over the past five years, has more than tripled ROIC, and guides FY 2026 adjusted EPS of $28.35–$28.85 with adjusted operating profit growth of 12%–16% and EPS growth of 16%–18%.

- Its oncology platform now serves 3,300 providers and 1.4 million patients in a $115 billion market, with recent acquisitions of Florida Cancer Specialists and Core Ventures enhancing scale and on track for expected synergy accretion.

- The biopharma services unit enabled over 100 million patient interactions, delivered $10 billion in out-of-pocket savings, and prevented 12 million prescription abandonments via connectivity to 1 million providers and 50,000 pharmacies.

- Maintains disciplined capital allocation with $2.5 billion in share repurchases planned for FY 2026 and over $6 billion of authorization, alongside dividend growth aligned with earnings following targeted M&A and portfolio optimization.

- Lemongrass completed a strategic partnership with SAP under the PartnerEdge (PE) Build program for its Clean Core AI Accelerator solution.

- The program grants full access to SAP APIs, tools, and services, plus technical enablement, certification opportunities, and go-to-market support.

- Lemongrass achieved SAP Gold Partner status, holds advanced competencies in SAP Cloud ERP Private Edition and BTP, and participates in SAP advisory councils.

- The firm manages over 750,000 SAP users across 20+ countries and serves major brands including McKesson, Cintas, and Heineken.

Fintool News

In-depth analysis and coverage of MCKESSON.

Quarterly earnings call transcripts for MCKESSON.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more