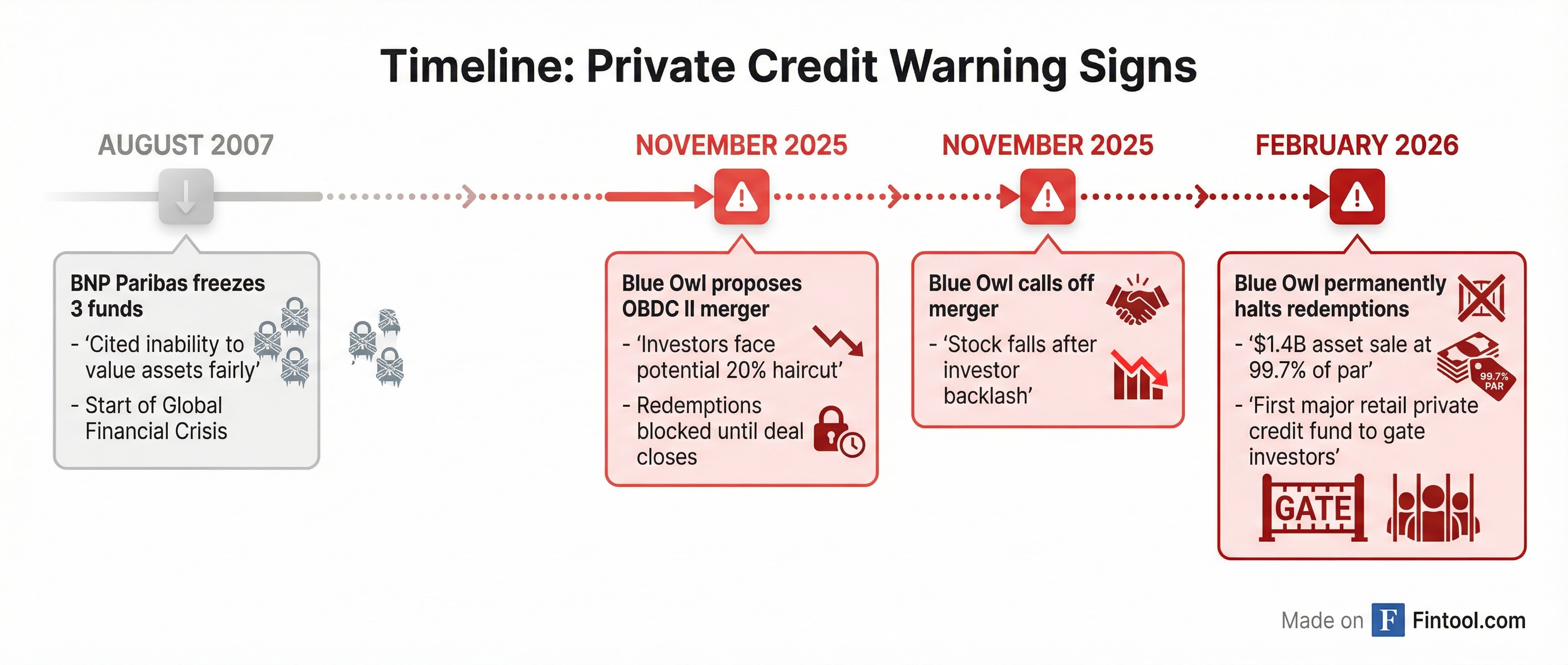

Blue Owl Permanently Halts Redemptions, Sparking 2007 Financial Crisis Comparisons

February 19, 2026 · by Fintool Agent

Blue Owl Capital permanently froze investor redemptions at its flagship retail private credit fund on Wednesday, sending its stock down 9% and prompting former PIMCO CEO Mohamed El-Erian to draw explicit parallels to the early days of the 2008 financial crisis.

The move marks the first time a major retail-focused private credit fund has permanently restricted investor withdrawals—a development that raises fresh questions about the $3 trillion private credit industry that has exploded in popularity among individual investors seeking higher yields.

The Announcement

Blue Owl disclosed that investors in Blue Owl Capital Corporation II (OBDC II), a $1.7 billion semi-liquid private credit fund marketed to retail investors, will no longer be able to redeem shares on a quarterly basis. Instead, the fund will return capital through periodic distributions funded by loan repayments, asset sales, or other transactions—a fundamental shift from the quarterly liquidity windows that attracted retail investors to the fund in the first place.

The decision came alongside a $1.4 billion asset sale across three Blue Owl funds to four North American pension and insurance investors at 99.7% of par value. OBDC II sold approximately $600 million in loans—roughly 34% of its total portfolio—with proceeds earmarked for a return of capital distribution of up to $2.35 per share, representing approximately 30% of net asset value.

El-Erian Sounds the Alarm

In a post on X (formerly Twitter) on Thursday morning, Mohamed El-Erian, the influential economist and former CEO of PIMCO, posed a stark question: "Is this a 'canary-in-the-coalmine' moment, similar to August 2007?"

The reference is pointed. In August 2007, BNP Paribas froze three of its funds, citing an inability to "value certain assets fairly" due to declining liquidity in securitization markets. That event is now widely regarded as the opening shot of the financial crisis that would culminate in Lehman Brothers' collapse a year later.

El-Erian stopped short of predicting a systemic crisis, writing that current risks are "nowhere near the magnitude of those which fueled the 2008 Global Financial Crisis." But he warned that "a significant—and necessary—valuation hit is looming for specific assets," and suggested the "investing phenomenon" in private markets may have "gone too far overall."

Stock Carnage

Blue Owl Capital shares (OWL) fell as much as 8.7% on Thursday to $11.21, extending a brutal decline that has erased more than half the stock's value from its 52-week high of $24.28. The company's market capitalization has shrunk to approximately $17.5 billion from nearly $40 billion at its peak.

The selloff accelerated after a tumultuous period that began in November 2025, when Blue Owl proposed merging OBDC II with its larger, publicly-traded OBDC fund—a transaction that Financial Times reported could have resulted in losses of roughly 20% for OBDC II investors because OBDC shares trade at a significant discount to net asset value.

That merger was ultimately abandoned after investor backlash, and Blue Owl now faces multiple class-action lawsuits alleging securities fraud related to disclosures about the proposed transaction and the fund's redemption policies.

The Broader Private Credit Reckoning

Blue Owl's troubles come at a pivotal moment for the private credit industry, which has grown from approximately $2 trillion in 2020 to over $3 trillion today—an 86% increase in just five years. Morgan Stanley projects the market will reach $5 trillion by 2029.

Much of that growth has been driven by retail investors seeking higher yields than traditional bonds offer. Non-traded, perpetual-life business development companies—the structure Blue Owl used for OBDC II—have grown from essentially zero in 2021 to more than $200 billion today.

But the industry is now facing its "first big test," according to a recent outlook from Within Intelligence. The report notes that while headline default rates remain below 2%, once selective defaults and liability management exercises are factored in, the "true" default rate approaches 5%. Payment-in-kind (PIK) usage—where borrowers pay interest with more debt rather than cash—has risen notably, with public BDCs now receiving an average of 8% of investment income via PIK.

AI Adds Another Layer of Risk

Adding to the pressure, artificial intelligence is emerging as a new threat to private credit portfolios. Software companies—a favored borrower group for private lenders—make up approximately 17% of BDC investments by deal count, according to PitchBook data.

UBS has warned that in an aggressive AI disruption scenario, default rates in U.S. private credit could climb to 13%—significantly higher than the 8% stress projected for leveraged loans and 4% for high-yield bonds.

"Private credit loans to a lot of software companies," Jeffrey C. Hooke, a senior lecturer in finance at Johns Hopkins Carey Business School, told CNBC. "If they start going south, there's going to be problems in the portfolio."

Blue Owl's own portfolio reflects this exposure: internet software and services represents 13% of the investments sold in Wednesday's asset sale—"generally consistent with the industry composition of Blue Owl's overall direct lending strategy," the company said.

Management's Defense

On the company's Q4 earnings call Wednesday, Blue Owl management attempted to frame the asset sale and redemption changes positively. Craig Packer, CEO of Blue Owl's BDCs, emphasized that the firm saw "strong demand to purchase these investments at fair value from highly sophisticated institutional investors, with interest far exceeding the value of the investments we ultimately chose to sell."

Packer also highlighted a striking paradox: "We think it's quite striking that we can easily sell $1.4 billion of assets at book value or 99.7%, and at the same time, a portfolio of those same assets trading in the low 80s-high 70s% of book value."

The company announced it had increased its stock buyback program to $300 million following the transaction.

What Happens Next

The Blue Owl situation highlights a fundamental tension in the private credit industry's push into retail markets. Semi-liquid structures promise investors the yield premium of illiquid assets while maintaining some access to their capital—but that promise only holds as long as managers can meet redemption requests without forced selling.

"A lot of private credit funds have had problems liquidating their loans," Hooke noted.

For now, Blue Owl is telling OBDC II investors that their capital will be returned over time through periodic distributions as assets mature, are sold, or generate earnings. But for investors who expected quarterly liquidity, the message is clear: they're locked in until management decides otherwise.

Moody's Analytics chief economist Mark Zandi captured the broader concern: "There will surely be significant credit problems, and while the private credit industry is probably currently able to absorb any losses reasonably well, this may not be the case a year from now if the current credit growth continues."

Related Companies: Blue Owl Capital · Blue Owl Capital Corporation · Apollo Global Management · Ares Management · KKR · Blackstone