Hartford CEO Swift at BofA Conference: AI Foundation Built, Now It's Time to 'Go Faster Than Most'

February 10, 2026 · by Fintool Agent

The Hartford CEO Christopher Swift delivered a confident message to investors at the BofA Securities Financial Services Conference in Miami today: a decade of disciplined technology investment has positioned the insurer to accelerate AI adoption faster than competitors.

"AI for us isn't at experimentation. We've been doing it for two years, in thoughtful ways," Swift told Bank of America analyst Josh Shanker. The Hartford's stock closed Monday at $139.38 before today's presentation, trading within striking distance of its 52-week high of $144.50, up 86% over the past three years compared to 59% for Travelers and 48% for Chubb.

The Platform Foundation: $250 Million and 15 Years in the Making

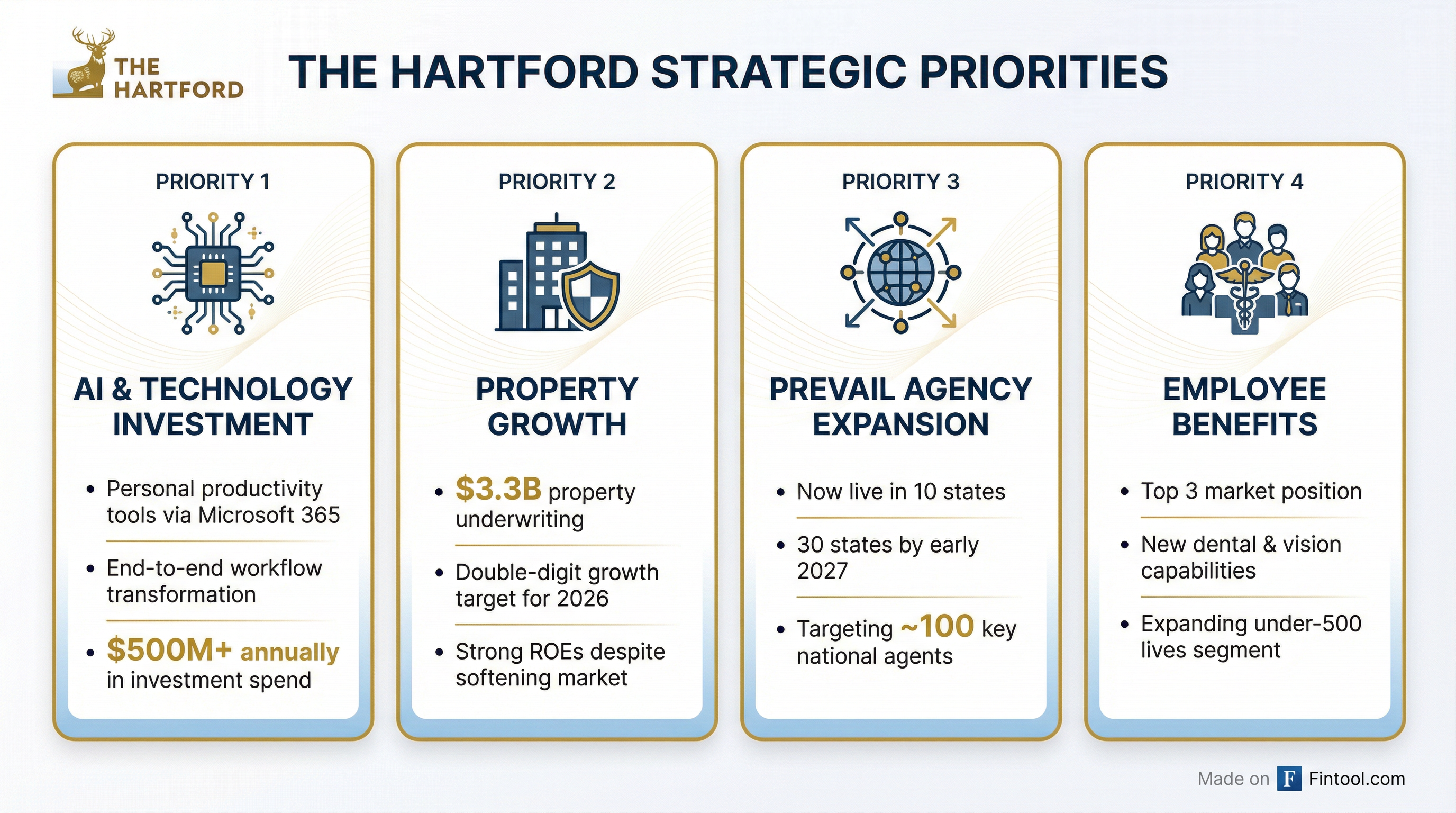

Swift traced Hartford's competitive advantage to a systematic platform rebuild that began in the aftermath of the financial crisis. The company consolidated claims platforms onto Guidewire, deployed new billing capabilities, and made a $250 million investment in Duck Creek for personal lines.

"The fortuitous nature of where we are today is if we hadn't really made those investments in platform to organize our data better, we wouldn't be in the position we are today in rolling out AI," Swift explained.

The company's annual technology "invest spend" has grown to over $500 million, up from approximately $350 million five to six years ago. CFO Beth Costello indicated this elevated investment level will continue, noting "there's plenty of areas for us to continue to invest."

AI Strategy: Personal Productivity and End-to-End Transformation

Swift outlined Hartford's two-pronged AI approach: personal productivity tools via Microsoft 365, and end-to-end workflow transformation across underwriting, operations, and claims.

"We want a better customer experience, the person that uses our product, and its advisors and agents. That's important. And then, you know, I would ultimately say we know there's productivity gains that will come long term," Swift said.

The company is 75-80% complete with its cloud migration to Amazon Web Services, with full completion expected by the end of 2027. This infrastructure positions Hartford to leverage AI capabilities across its data assets.

Prevail: Betting on the Agency Channel

Hartford is aggressively expanding its Prevail personal lines platform into the independent agency channel. Currently live in 10 states, the company targets 30 states by early 2027.

The strategy leverages Hartford's existing commercial relationships. "There's probably 100 agents in the personal lines area that really matter because they know us from small business. They know us from middle market," Swift said. Many agency executives have told Hartford, "We're so glad you're back."

The Prevail platform was originally built for Hartford's AARP partnership and repurposed for the agency channel. Key changes include eliminating the lifetime renewal guarantee in favor of six-month policies, allowing Hartford to better manage underwriting risk.

On the Q4 2025 earnings call, Head of Personal Lines Melinda Thompson noted that agency Prevail represents "a meaningful growth opportunity," though it currently accounts for about 20% of personal lines premium and "would take time to grow it to be the size of AARP's book."

Small Business Dominance: Seven-Year Digital Crown

Hartford retained its #1 ranking in small business digital capabilities from Keynova Group for the seventh consecutive year, maintaining "a double-digit lead in all categories" for functionality, ease of use, and agent support.

The small business unit delivered $6 billion in written premium with an 88.9 underlying combined ratio in 2025. Swift emphasized that Hartford's advantage comes from "speed, accuracy, predictability, consistency" that agents increasingly value as distribution consolidates.

| Metric | FY 2023 | FY 2024 | FY 2025 |

|---|---|---|---|

| Revenue* | $23.1B | $25.0B | $26.6B |

| Net Income* | $2.5B | $3.1B | $3.8B |

| ROE | 17.3% | 19.6% | 21.7% |

| EBITDA Margin | 15.2% | 16.3% | 18.7% |

*Values retrieved from S&P Global

Capital Allocation: $450 Million Quarterly Buybacks, M&A De-Prioritized

Hartford announced on its Q4 2025 earnings call that quarterly share repurchases will increase to $450 million beginning Q1 2026, up from $400 million, implying approximately $1.8 billion in annual repurchases. This is funded by $2.9 billion in expected dividends from operating companies, a 16% increase from 2025.

The company also raised its common dividend by 15% in 2025. Costello framed the increase as reflecting Hartford's higher earnings generation and "the stability that we see there."

On M&A, Costello was direct: "That's a low priority for us when we look at the capabilities that we have in-house and our ability to execute. Don't feel that we have a hole that we need to fill."

Property: Double-Digit Growth Despite Softening Prices

Despite moderating property pricing, Swift confirmed Hartford is targeting double-digit growth in property underwriting, currently at $3.3 billion across all business units.

"Even in the face of softening property prices, we still think the starting point is good. The returns are great," Swift said. The company recently issued a new catastrophe bond, increasing its Foundation Re program to $1.9 billion in total per-occurrence coverage for peak perils.

On early 2026 catastrophe activity, Swift noted that weather events in Texas, Tennessee, and the Mid-Atlantic represent "an event. It's not small. It's not major," suggesting Q1 catastrophe losses will be manageable.

Social Inflation: "It's Real"

When asked about whether social inflation was affecting commercial lines profitability, Swift was unequivocal: "Social inflation is showing up in the numbers."

He cited steady-to-increasing trends in representation rates, litigation rates, and settlement costs. "Awards are getting more expensive to settle. There's more lawyers involved earlier on," Swift said.

However, Hartford's renewal pricing remains above loss trends. Business insurance pricing excluding workers' comp was 6.1% in Q4 2025, with excess and umbrella in the double digits and commercial auto stable in the low double digits.

What to Watch

Near-term catalysts:

- Prevail agency expansion progress toward 30 states by early 2027

- Q1 2026 catastrophe loss disclosure

- Continued share repurchase execution at $450M quarterly pace

Key metrics to monitor:

- Small business market share gains and combined ratio stability

- Employee benefits quote activity trends (management noted "meaningfully above prior year")

- Personal lines policy count growth in the agency channel

Hartford next reports Q1 2026 earnings in late April.

Related Companies: The Hartford · Travelers · Chubb · Progressive

Source: BofA Securities Financial Services Conference, February 10, 2026