JPMorgan Chase Bets $1B+ on Physical Banking With 160+ New Branches in 2026

February 18, 2026 · by Fintool Agent

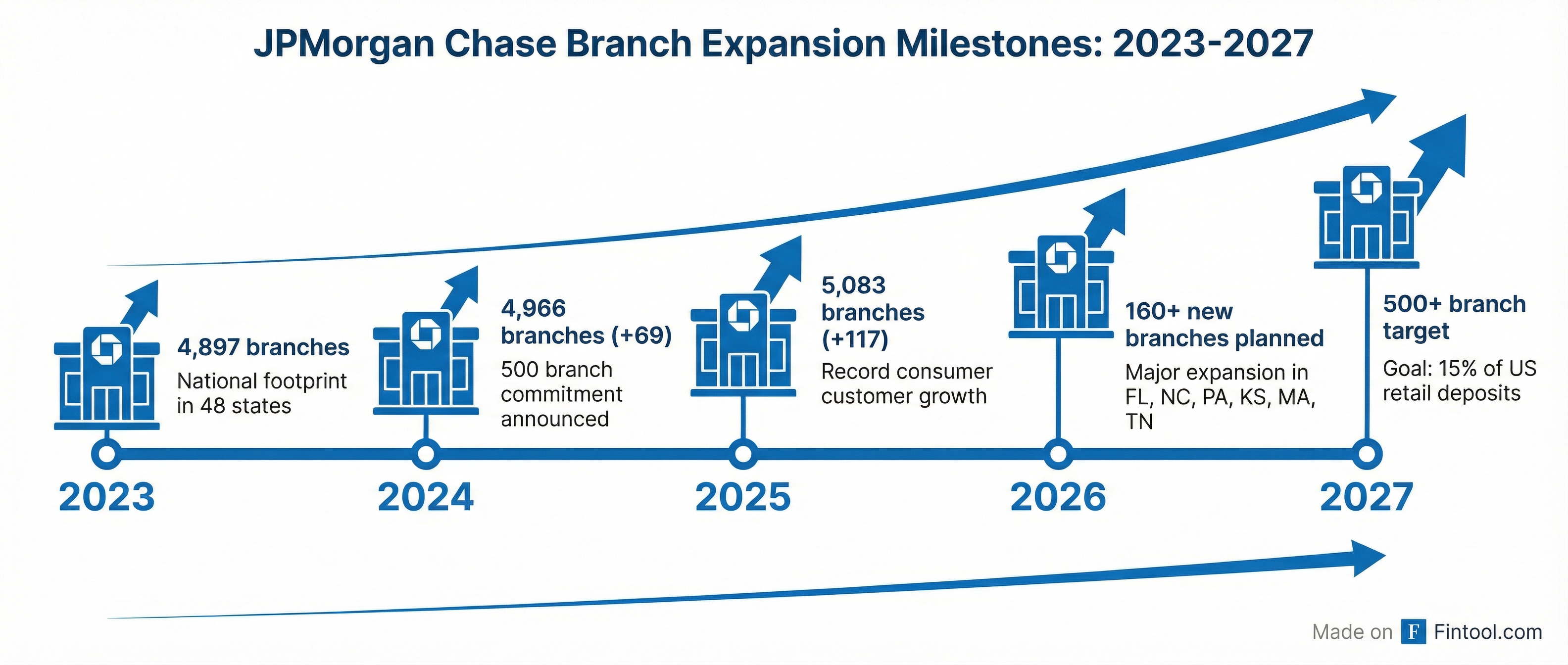

JPMorgan Chase is doubling down on brick-and-mortar banking, announcing plans to open more than 160 new branches across 30+ states in 2026 as part of a multibillion-dollar investment in its physical network.

The expansion—which targets Florida, North Carolina, South Carolina, Pennsylvania, Kansas, Massachusetts, and Tennessee—marks the largest single-year branch push in the bank's recent history and runs counter to the global trend of bank branch closures.

"We know that building branches and getting into markets is a critical part of getting that deposit share," Jennifer Roberts, CEO of Chase consumer banking, told the Financial Times. The bank is targeting 15% of all US retail deposits.

The Contrarian Bet

While UK banks are shuttering branches amid the shift to digital banking, America's largest bank is moving in the opposite direction. The 160+ branch target for 2026 is part of a 2024 commitment to open more than 500 branches within three years.

JPMorgan's data backs the strategy. New branches are reaching profitability "months sooner" than the four-year target, driven by strong growth in deposits, credit card accounts, and wealth management clients.

By the Numbers: The Consumer Banking Machine

JPMorgan's Consumer & Community Banking segment is a profit engine. The division generated $76 billion in net revenue in FY2025, up 6% year-over-year, with net income of $18.2 billion and a 32% return on equity.

The branch network has grown steadily alongside digital adoption:

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Number of Branches | 4,897 | 4,966 | 5,083 |

| Consumer Customers (millions) | 82.1 | 84.4 | 86.6 |

| Active Digital Customers (millions) | 67.0 | 70.8 | 74.6 |

| Active Mobile Customers (millions) | 53.8 | 57.8 | 61.7 |

| Client Investment Assets ($B) | $951 | $1,088 | $1,270 |

Source: JPMorgan Chase FY2025 10-K

The data shows that digital and physical banking aren't mutually exclusive—JPMorgan added 2.2 million consumer customers in 2025 while growing both branch count and digital engagement.

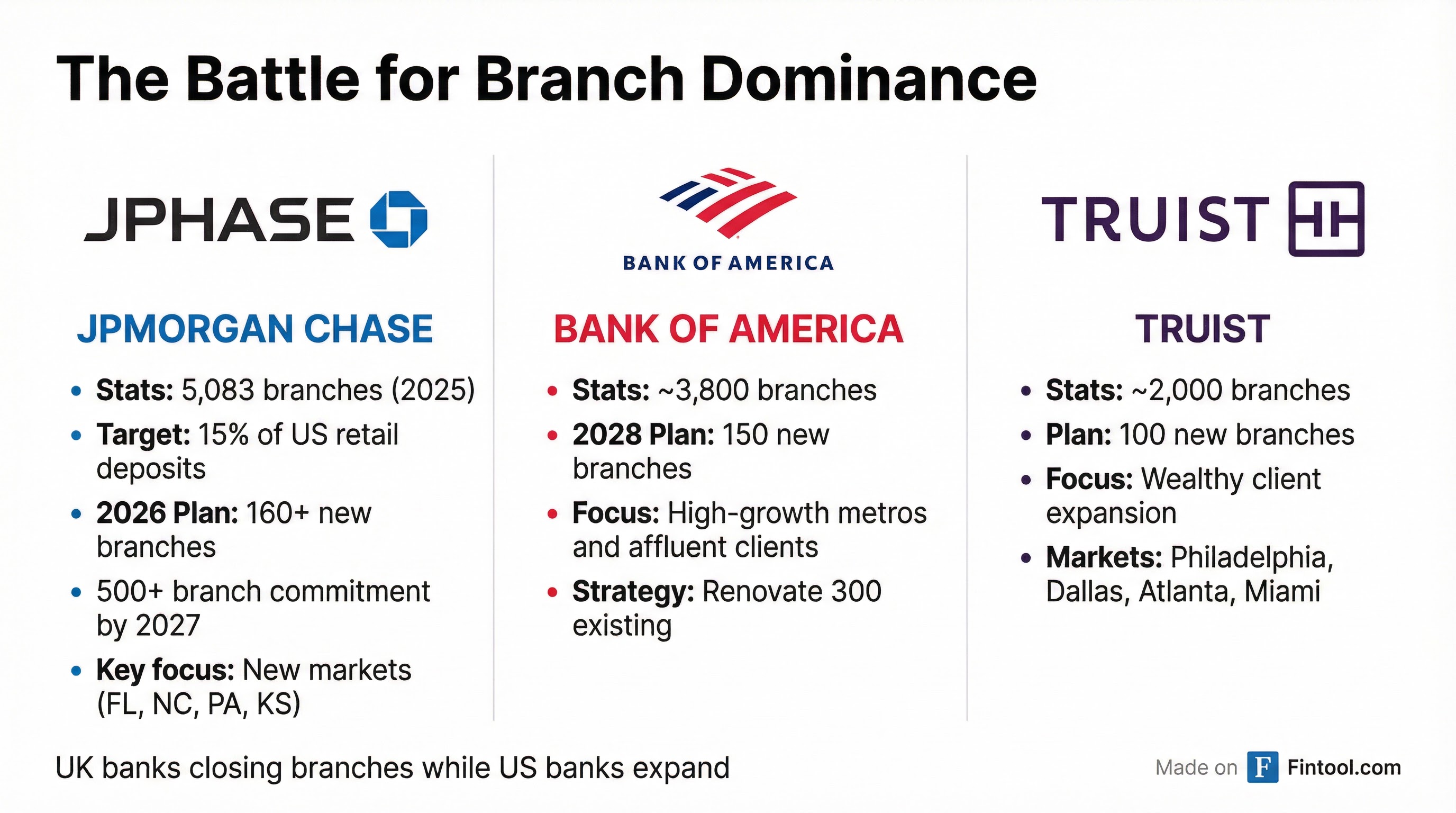

The Competitive Landscape

JPMorgan isn't alone in betting on branches. Bank of America announced plans in 2025 to open 150 new branches by 2028, while Truist committed to 100 new locations targeting affluent clients in Philadelphia, Dallas, Atlanta, Austin, Miami, and Washington.

"Physical and human advisory still matters," Truist Chief Consumer and Small Business Banking Officer Dontá Wilson told Bloomberg. "We're big enough to afford and invest in all the digital technology capabilities. But we also operate in these community-oriented ways that are deeply relational."

JPMorgan's scale advantage is substantial. With $4.4 trillion in assets and a $816 billion market cap, the bank can outspend competitors on both digital innovation and physical infrastructure.

| Bank | Market Cap | Total Assets | Est. Branches | Branch Strategy |

|---|---|---|---|---|

| JPMorgan Chase | $816B | $4.4T | 5,083 | +500 by 2027 |

| Bank of America | $379B | $3.4T | 3,800 | +150 by 2028 |

| Truist | $58B | $530B | 2,000 | +100 planned |

The Strategic Logic

The branch expansion reflects a broader strategy to dominate US retail banking. JPMorgan currently operates in 48 of 50 states (excluding only Hawaii and Alaska), and the new branches will deepen its presence in high-growth markets.

The bank's Consumer & Community Banking division serves three customer bases through its branch network:

-

Banking & Wealth Management ($42.9B revenue in FY2025): Deposits, investments, cash management, and J.P. Morgan Wealth Management services

-

Home Lending ($5.0B revenue): Mortgage origination increased to $52.8 billion in 2025, up from $40.8 billion in 2024

-

Card Services & Auto ($28.2B revenue): 10.4 million new credit card accounts opened in 2025, bringing cards in force to 116.5 million

The cross-sell opportunity is key. A single branch customer often becomes a mortgage borrower, credit card holder, and wealth management client—multiplying the lifetime value far beyond what's possible through digital-only acquisition.

What to Watch

Near-term catalysts:

- Q1 2026 earnings (April) for early branch opening metrics

- Deposit share data from FDIC annual survey (June)

- Competitor branch announcements

Risks:

- Economic downturn reducing demand for new branches

- Digital-first competitors gaining share with younger demographics

- Higher-than-expected construction and staffing costs

The expansion comes as JPMorgan posted strong Q4 2025 results, with net income of $13.0 billion and total assets of $4.4 trillion. The bank's Consumer & Community Banking segment continues to deliver a 32% return on equity, validating the branch-centric model.

Related