Rezdiffra Hits $958M in Year One — But Madrigal Stock Drops 11%

February 19, 2026 · by Fintool Agent

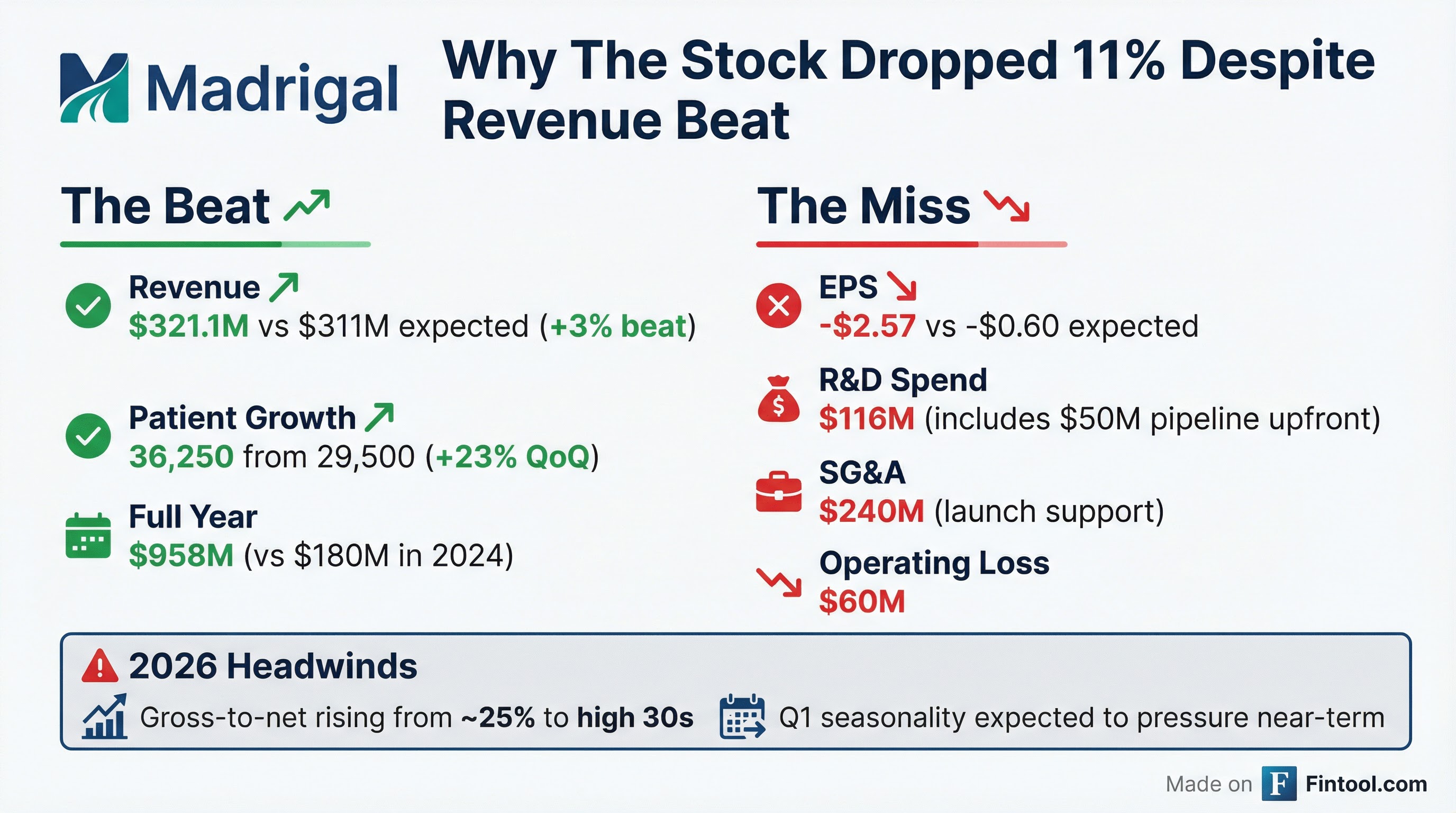

Madrigal Pharmaceuticals delivered one of the most successful specialty drug launches in biotech history—Rezdiffra reaching $958 million in its first full year on the market—yet shares plunged 11% after the company reported a Q4 loss that was $2.61 per share wider than Wall Street expected.

The disconnect highlights the classic biotech dilemma: management is building a pipeline and commercial infrastructure that requires heavy upfront investment, while investors focus on near-term losses and margin pressure.

"2025 marked a defining year for Madrigal," CEO Bill Sibold said on the earnings call. "We solidified our position as the undisputed leader in MASH highlighted by nearly $1 billion in Rezdiffra sales in its first full year of launch. And we're just getting started."

The Beat vs. The Miss

The headline numbers tell a tale of two narratives. Revenue came in ahead of expectations, patient growth accelerated, and the commercial launch is executing well. But the EPS miss was severe—and driven by deliberate strategic choices.

| Metric | Q4 2025 | Estimate | Variance |

|---|---|---|---|

| Net Sales | $321.1M | $310.8M | +3.3% |

| EPS | -$2.57 | -$0.60 | -$1.97 |

| Patients on Therapy | 36,250+ | — | +23% QoQ |

The loss widened primarily due to pipeline investments. In Q3, Madrigal paid $120 million upfront to license an oral GLP-1 agonist. In Q4, it paid $50 million for ervogastat (a DGAT-2 inhibitor) and early-stage MASH assets. A $60 million payment for siRNA programs will hit Q1 2026.

Revenue Trajectory: From Zero to Near-Blockbuster

Rezdiffra became the first FDA-approved treatment for MASH (metabolic dysfunction-associated steatohepatitis, formerly known as NASH) in March 2024. In less than two years, it has established itself as the standard of care in a market that didn't exist before.

Key launch metrics from Q4 2025:

| Metric | Q4 2025 | FY 2025 | FY 2024 |

|---|---|---|---|

| Net Sales | $321.1M | $958.4M | $180.1M |

| Cost of Sales | $24.4M | $56.1M | $6.2M |

| R&D Expense | $116.3M | $388.5M | $236.7M |

| SG&A Expense | $240.0M | $813.8M | $435.1M |

| Operating Loss | $59.6M | $300.1M | $497.9M |

Despite the headline loss, the operating loss actually narrowed from 2024 as revenue scaled faster than expenses. The company ended Q4 with $988.6 million in cash, up from $931.3 million a year earlier, thanks in part to a $350 million term loan secured in July 2025.

The Market Is Real — And Growing Fast

One of the most bullish data points from the call: the addressable patient population has grown nearly 50% in just two years.

Madrigal targets approximately 315,000 patients with moderate to advanced fibrosis (F2-F3) currently under the care of liver specialists in the U.S. This population has expanded dramatically since Rezdiffra's approval as disease awareness, diagnosis rates, and referrals to specialists have increased.

"The market is in a position to grow," Sibold said. "We had talked about the 315,000 diagnosed patients sitting in the offices of the target specialists. What we're seeing is our efforts are really paying off... We're expecting double-digit growth for the foreseeable future."

With approximately 245,000 additional patients with compensated cirrhosis (F4c) potentially addressable pending regulatory approval, the total opportunity could double.

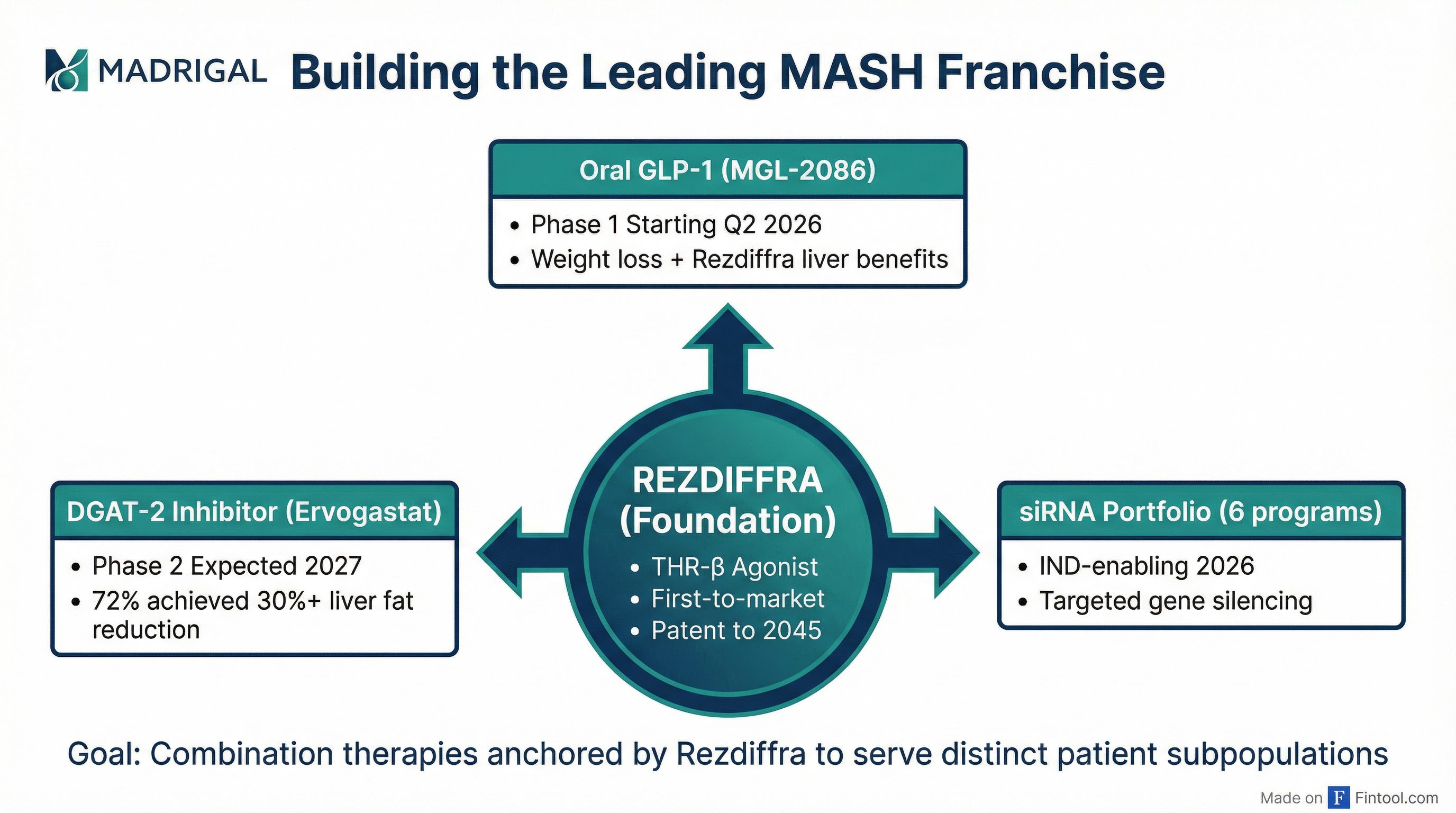

Pipeline Strategy: Building a Franchise

Madrigal is no longer a single-product company. In six months, it has assembled a pipeline of more than 10 programs designed to extend its MASH leadership through combination therapies.

The strategy centers on Rezdiffra as the foundational therapy, with complementary mechanisms layered on top:

Oral GLP-1 (MGL-2086): Licensed from CSPC, this orforglipron derivative is expected to enter Phase 1 in Q2 2026. The goal is a well-tolerated fixed-dose combination that optimizes weight loss to potentiate Rezdiffra's anti-fibrotic effect—targeting as little as 5% weight loss, not maximal weight loss.

DGAT-2 Inhibitor (Ervogastat): Acquired from Pfizer, this late-stage asset demonstrated impressive Phase 2 results—72% of patients at 150mg achieved at least 30% reduction in liver fat, and 61% achieved a "super response" of 50%+ reduction. A drug-drug interaction study is planned for 2026, with a Phase 2 combination trial expected in 2027.

siRNA Portfolio: Six preclinical programs licensed from Ribocure target validated genes that drive MASH progression. The GalNAc-conjugated siRNA modality is highly liver-targeted with an established clinical safety profile. IND-enabling activities will begin in 2026.

2026 Outlook: Strong Fundamentals, Near-Term Pressure

Management expects "robust" revenue growth in 2026, with consensus estimates around $1.3-1.4 billion implying 35-45% growth. However, several factors will pressure near-term results:

Gross-to-Net Step-Up: After deliberately delaying payer contracting to maximize pricing power during the launch phase, Madrigal entered into broad commercial contracts effective January 1, 2026. This will push gross-to-net discounts from ~25% in 2025 to the high 30s in 2026.

Q1 Seasonality: Like all specialty medicines, Rezdiffra faces typical Q1 dynamics—benefit plan changes, insurance re-verifications, and patient coverage disruptions. Management expects a mid- to high-single-digit sequential decline in Q1 net sales, consistent with specialty analogs.

Continued Investment: R&D expense is expected to remain roughly flat with 2025 (~$388 million), while SG&A will increase as the company builds infrastructure for long-term growth.

Despite these headwinds, Sibold emphasized the underlying momentum: "We just had our best NBRX week since launch."

GLP-1 Competition: Not the Threat Some Feared

One of the key debates around Madrigal has been whether GLP-1 obesity drugs from Novo Nordisk and Eli Lilly would cannibalize demand for Rezdiffra. The Q4 results suggest coexistence rather than competition.

"Wegovy's being used, but certainly not to the detriment of Rezdiffra," Sibold said. "In fact, we just had our best NBRX week since launch, which says to me that just as we had said, you can have multiple products in the space, but that Rezdiffra really is the winning profile."

Patient persistence remains in the 60-70% range at one year—consistent with well-tolerated oral therapies—with some institutions reporting rates as high as 90%. Data presented at AASLD showed that patients who discontinue Rezdiffra experience reversal of their earlier gains, reinforcing the case for chronic therapy.

What to Watch

MAESTRO-NASH OUTCOMES (2027): The pivotal Phase 3 outcomes trial in compensated cirrhosis (F4c) is tracking on schedule, with event accrual in the expected 5-10% annual range. Positive results would convert accelerated approval to full approval and expand the label to a significantly higher-urgency patient population.

Combination Program Progress: The oral GLP-1 Phase 1 starting in Q2 2026 and the ervogastat drug-drug interaction study will provide early reads on whether combinations can deliver meaningful improvements over Rezdiffra monotherapy.

Gross-to-Net Trajectory: How Q1 2026 net sales absorb the dual impact of seasonality and contracting will signal whether the pricing strategy is working as planned.

Market Expansion: Continued growth in the diagnosed F2-F3 population and progress toward F4c approval could significantly expand the long-term opportunity.