Wells Fargo CFO Details Post-Asset Cap Growth Playbook at UBS Conference

February 10, 2026 · by Fintool Agent

Eight months after the Federal Reserve lifted its $1.95 trillion asset cap, Wells Fargo is executing on a growth strategy that CFO Mike Santomassimo described as "a continuation of what we've seen now for a number of quarters" at today's UBS Financial Services Conference in New York.

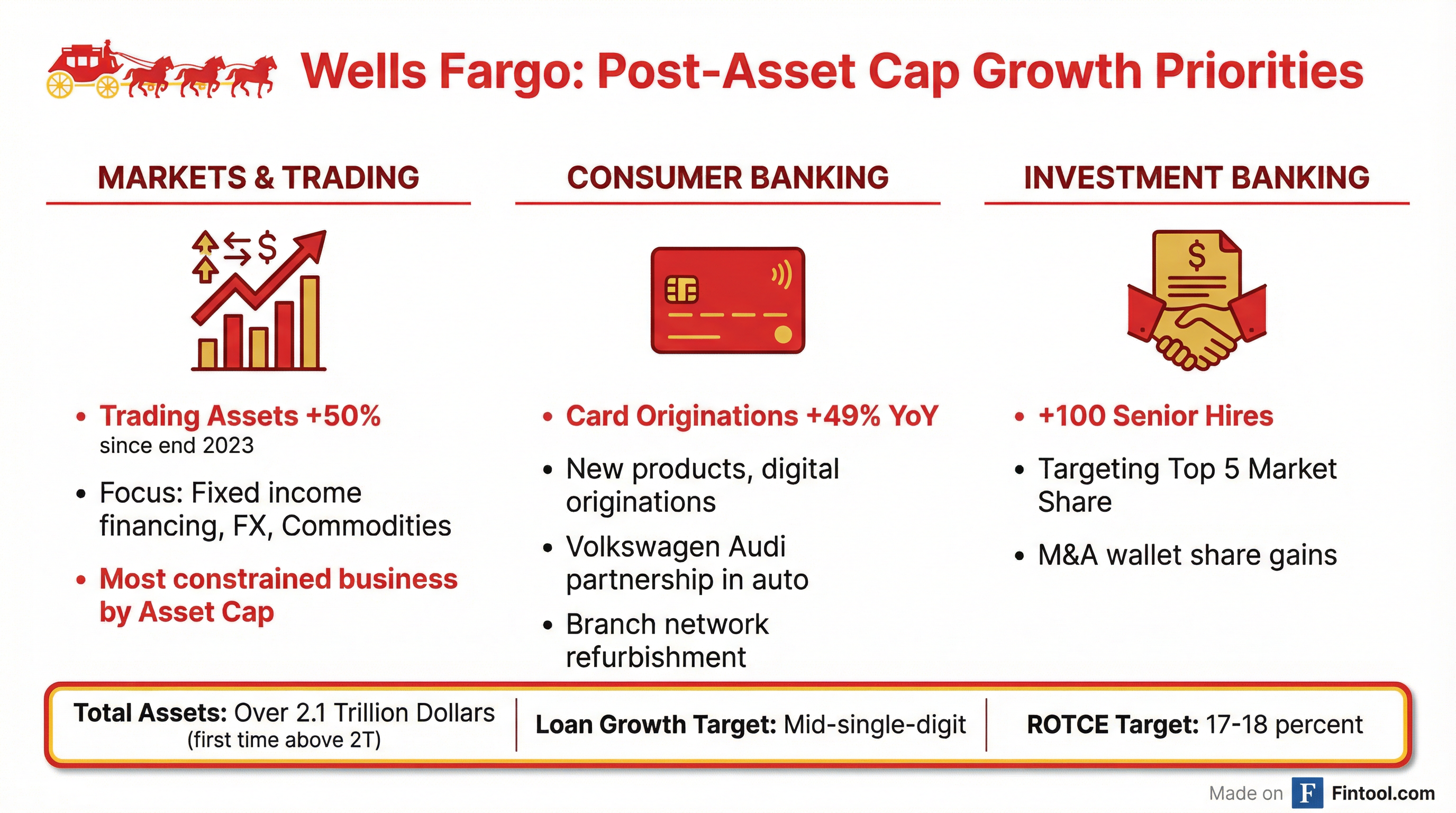

The nation's fourth-largest bank is projecting mid-single-digit average loan growth for Q4 2026 versus Q4 2025, with expansion led by the markets business that was most constrained during the seven-year regulatory restriction. The stock has rallied 26.5% since the June 3, 2025 asset cap removal, trading near $94.49 this morning.

The Growth Thesis: "Strategy Hasn't Changed"

Santomassimo was clear that Wells Fargo isn't pursuing a dramatically new direction post-asset cap—rather, it's finally able to execute on investments made "four, five, six years ago."

"The strategy hasn't changed at all," Santomassimo told the UBS audience. "A lot of where we're seeing growth are the areas that we started investing in... On the consumer side, it's places like card, it's in our retail footprint across the core consumer banking space. On the commercial side, it's in places like investment banking, the markets business."

The markets business has been the standout beneficiary. Trading-related assets in the corporate investment bank are up 50% since the end of 2023, driven primarily by financing activity—high-quality collateral, low-risk, low-RWA business that serves as a gateway to broader client relationships.

"With the business, by far the most impacted by the Asset Cap... what you've seen so far, in large part, is growth in a lot of the financing trade," Santomassimo explained. "That'll come, over a period of time, but I think we're very, we're very pleased with what we're seeing come through so far."

Loan Growth: Where the Opportunities Are

Santomassimo walked through the loan portfolio with granular detail, signaling where investors should expect balance sheet expansion:

Credit Cards: New account originations were up 49% year-over-year in Q3 2025, driven by products launched since 2021 that are now hitting their third-year profitability inflection point. The bank is targeting its wealth management clients with new card products launching in 2026.

"We saw a big uptick in new account origination in the credit card business in the second half of last year," Santomassimo said. "And we're very pleased with what's going on there."

Auto Lending: Volumes more than doubled year-over-year in Q3 2025 following the Volkswagen Audi preferred partnership and a modest expansion down the credit spectrum—though Santomassimo emphasized "a little more full spectrum... I wouldn't say we're going all the way down into deep subprime in any way."

Commercial Banking: Utilization rates on commercial revolvers remain low on a historical basis—a potential upside catalyst if the investment cycle picks up. "People aren't utilizing the revolvers more significantly than they had," Santomassimo noted. "I think that's an opportunity as people continue to get more and more comfortable with where the economy's going."

| Segment | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 |

|---|---|---|---|---|

| Revenue ($B) | $8.96 | $9.49 | $9.11 | $8.65 |

| Net Income ($B) | $5.36 | $5.59 | $5.49 | $4.89 |

| ROE (%) | 11.9% | 12.3% | 12.1% | 10.6% |

| Total Assets ($T) | $2.15 | $2.06 | $1.98 | $1.95 |

Mortgage: The only consumer business not growing—balances have declined and will remain "relatively flat throughout the year."

Markets Revenue: Higher NII, Lower Fees—But Growing Overall

Santomassimo clarified a point that had confused some investors on the Q4 earnings call: while geography will shift between net interest income and fee income in the markets business due to rate movements, total markets revenue is expected to grow year-over-year in 2026.

"If revenue was flat year-over-year, you would see a geography change of higher NII, lower fees," he explained. "But we're saying overall revenue should grow. How much? We'll see, right? A lot of that's going to be based on the volatility that's there and the activity levels in the overall market."

The FX business serves as the template for expansion: built from a corporate payments base into an institutional platform, it now hits record volumes every quarter. The playbook is being applied to rates, fixed income financing, and equities.

Investment Banking: "First Top Five, Then We'll See"

Wells Fargo has hired roughly 100 senior investment bankers over the past several years and is seeing market share gains—over 120 basis points in U.S. M&A since 2022, the most of any investment bank. The Q3 2025 quarter was the bank's highest investment banking fee quarter ever.

"The goal is to, you know, continue to see more progress, and I think the most visible way you see that progress is through market share and wallet share increases," Santomassimo said. "We feel like we can compete with anybody."

The target: crack the top five U.S. investment banks.

Wealth Management: Attrition at Lows, Recruiting Strong

The wealth business showed improved momentum in the second half of 2025:

- Total hires increasing

- Attrition declining to multi-year lows

- Net asset flows accelerating

- Direct recruiting from wirehouses and independent platforms picking up

The Wells Fargo Premier channel—advisors in branches serving affluent clients with $250,000+ in assets—has particular upside. Santomassimo cited 6-8 million customers with $6-8 trillion in assets either with Wells Fargo or elsewhere.

The Efficiency Story Continues

Headcount has declined for 21-22 consecutive quarters, down approximately 70,000 from the 276,000 peak in 2020 to roughly 206,000 today. The bank has achieved approximately $15 billion in gross expense saves since Scharf arrived, funding both regulatory remediation and growth investments.

"We still have a lot more to do," Santomassimo said. "And that's before you even get to the benefits of things like AI."

On regulatory spend, he noted that the $2.5 billion+ invested in risk and control infrastructure won't come out quickly: "It just takes time to do that, and so that'll happen over a bit of a longer period of time."

M&A: "The Bar is High"

When pressed on inorganic growth—a recurring investor question given the favorable regulatory environment—Santomassimo reiterated CEO Charlie Scharf's stance:

"We have a really enviable position, right? We've got scale in all of our key businesses. We feel no pressure at all to, like, do acquisitions to grow. We've got a tremendous amount of organic opportunity to grow in every single one of the businesses in the best market in the world to do that. And so the bar is high."

What to Watch

Near-term catalysts:

- Commercial banking loan utilization—if the investment cycle picks up, revolver draws could accelerate

- Card vintage maturation—2021-2022 products hitting profitability inflection

- Markets revenue growth confirmation in Q1 2026 results

Regulatory factors:

- Basel III endgame and GSIB recalibration could provide additional capital flexibility

- CET1 target of 10-10.5% leaves significant buyback capacity

Analyst estimates project Wells Fargo earning $6.95 EPS in 2026 on revenues of approximately $88.8 billion, with consensus price targets around $101.*

| Forward Estimates | Q1 2026 | Q2 2026 | Q3 2026 | Q4 2026 |

|---|---|---|---|---|

| Revenue ($B) | $21.8* | $22.1* | $22.4* | $22.4* |

| EPS | $1.58* | $1.75* | $1.83* | $1.80* |

*Values retrieved from S&P Global

Related