Earnings summaries and quarterly performance for UNISYS.

Executive leadership at UNISYS.

Michael Thomson

Chief Executive Officer and President

Chris Arrasmith

Executive Vice President and Chief Operating Officer

Debra McCann

Executive Vice President and Chief Financial Officer

Kristen Prohl

Senior Vice President, General Counsel, Secretary and Chief Administration Officer

Teresa Poggenpohl

Senior Vice President and Chief Marketing Officer

Board of directors at UNISYS.

Deborah Lee James

Director

John Kritzmacher

Director

Matthew Desch

Director

Nathaniel Davis

Lead Independent Director

Paul Martin

Director

Peter Altabef

Chair of the Board

Philippe Germond

Director

Regina Paolillo

Director

Roxanne Taylor

Director

Troy Richardson

Director

Research analysts who have asked questions during UNISYS earnings calls.

Anja Soderstrom

Sidoti & Company, LLC

6 questions for UIS

Rod Bourgeois

DeepDive Equity Research

6 questions for UIS

Arun Seshadri

BNP Paribas

3 questions for UIS

Ana Goshko

Bank of America

2 questions for UIS

Joseph Vafi

Canaccord Genuity - Global Capital Markets

2 questions for UIS

Maggie Nolan

William Blair

2 questions for UIS

Mayank Tandon

Needham & Company, LLC

2 questions for UIS

Kellen D'Alleva

Jefferies

1 question for UIS

Recent press releases and 8-K filings for UIS.

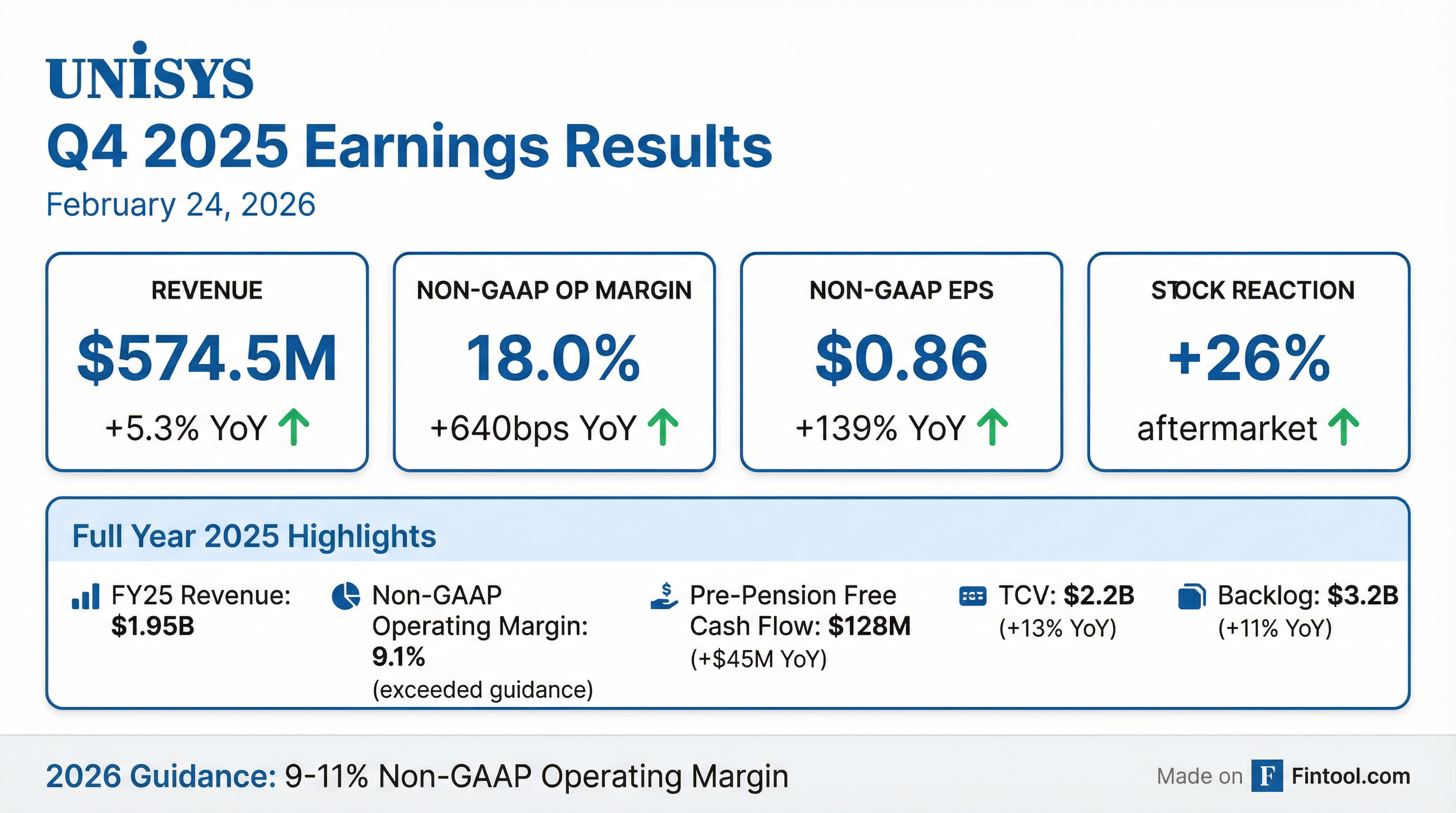

- Unisys reported Q4 2025 revenue of $575 million, an increase of 5.3% year-over-year, and full year 2025 revenue of $1.95 billion, a decrease of 2.9%. The company achieved a non-GAAP operating margin of 18% in Q4 and 9.1% for the full year, exceeding its upwardly revised projections.

- The company significantly advanced its pension removal strategy, reducing global pension deficits by $300 million-$450 million at year-end 2025 and removing approximately $320 million of gross US defined benefit pension liabilities through an annuity purchase. This contributed to a strong liquidity position with $414 million in cash at year-end and an improved net leverage ratio of 2.8x.

- Unisys secured $1.7 billion in renewal Total Contract Value (TCV) for the full year 2025, with over $1 billion signed in Q4, and ended the year with a backlog of $3.2 billion, an 11% increase from the prior year. The company is also positioning artificial intelligence as a powerful long-term demand driver, investing in AI-enabled solutions like the Service Experience Accelerator.

- For full year 2026, Unisys expects total company revenue to decline between 6.5% and 4.5% in constant currency and projects a non-GAAP operating profit margin of 9% to 11%. Full year free cash flow is anticipated to be approximately -$25 million, translating to $67 million of pre-pension free cash flow.

- Unisys reported Q4 2025 revenue of $575 million, an increase of 5.3% year-over-year, contributing to a full-year 2025 revenue of $1.95 billion. The company achieved a full-year non-GAAP operating margin of 9.1% and generated $128 million in full-year pre-pension free cash flow, up 55% from the prior year.

- The company significantly de-risked its pension obligations, reducing its global GAAP pension deficit by $300 million to approximately $450 million by December 31, 2025, and improved net leverage to 2.8x from 3.0x at the end of 2024.

- Unisys secured $1.7 billion in renewal Total Contract Value (TCV) for the full year 2025, with over $1 billion signed in the fourth quarter. The company also gained recognition as a global leader in Gartner's Outsourced Digital Workplace Services Magic Quadrant and was named to Forbes' list of America's Best Midsize Employers in 2026.

- Artificial intelligence is viewed as a powerful long-term demand driver, with Unisys investing in solution development and delivery skills, including the launch of Service Experience Accelerator (SEA) in 2025, an agentic AI framework for Next-Generation Service Desk.

- For 2026, Unisys expects total company revenue to decline between 6.5% and 4.5% in constant currency and projects a non-GAAP operating profit margin between 9% and 11%.

- For Full-Year 2025, Unisys reported $1,950 million in revenue, a 2.9% year-over-year decrease, and achieved a 9.1% Non-GAAP Operating Margin, exceeding its upwardly-revised guidance range.

- The company significantly enhanced its financial position in 2025, with Pre-Pension Free Cash Flow of $128 million and a $300 million reduction in the Global Pension GAAP deficit to $450 million by year-end. Net leverage improved to 2.8x compared to 3.0x a year ago.

- Unisys issued Full-Year 2026 financial guidance, projecting constant currency revenue growth of (6.5%) to (4.5%) and a Non-GAAP Operating Profit Margin of 9.0% to 11.0%. The company also expects Free Cash Flow of approximately ($25 million) for 2026.

- Unisys reported Q4 2025 revenue growth of 5% year-over-year and a full-year 2025 non-GAAP operating margin of 9.1%, exceeding projections.

- The company generated $128 million in full-year pre-pension free cash flow in 2025, a 55% increase from the prior year, and ended the year with a strong cash balance of $414 million.

- Unisys significantly advanced its pension removal strategy, reducing its global GAAP pension deficit by $300 million to $450 million at year-end 2025, and executed an annuity purchase removing approximately $320 million of US defined benefit pension liabilities.

- For 2026, Unisys expects total company revenue to decline between 6.5% and 4.5% in constant currency, with a non-GAAP operating profit margin between 9% and 11%.

- The company secured $1.7 billion in renewal TCB for 2025 and is leveraging AI as a key driver for future demand and efficiency, with Unisys recognized as a global leader in Outsourced Digital Workplace Services by Gartner.

- Unisys reported Q4 2025 revenue of $574.5 million, up 5.3% year-over-year, and full-year 2025 revenue of $2.0 billion, a 2.9% decrease year-over-year.

- The company's non-GAAP operating profit margin increased to 18.0% in Q4 2025 (up 640 bps YoY) and 9.1% for full-year 2025 (up 30 bps YoY), exceeding its upwardly revised guidance.

- For full-year 2025, cash used for operations was $140.0 million, including a $250 million discretionary pension contribution, while cash and cash equivalents stood at $413.9 million at year-end. The defined benefit pension funding deficit improved by $301.7 million to $448.5 million.

- Unisys provided full-year 2026 guidance, projecting revenue growth in constant currency of (6.5)% to (4.5)% and a non-GAAP operating profit margin of 9.0% to 11.0%.

- Unisys reported full-year 2025 revenue of $1,950.1 million, a 2.9% decrease year-over-year, with a GAAP operating profit margin of 4.0% and a non-GAAP operating profit margin of 9.1%. The company experienced a net loss attributable to Unisys Corporation of ($339.8 million) for the full year, which included a $227.7 million non-cash pension settlement loss and $55.0 million in goodwill impairment charges. In the fourth quarter of 2025, revenue increased 5.3% year-over-year to $574.5 million, with a non-GAAP operating profit margin of 18.0%, exceeding upwardly revised guidance.

- The company ended 2025 with a strong liquidity position, reporting $413.9 million in cash and cash equivalents as of December 31, 2025. Cash provided by operations in Q4 2025 was $104.9 million, and pre-pension and postretirement free cash flow for the full year 2025 increased to $127.7 million. Unisys also significantly improved its defined benefit pension plans funding deficit by $301.7 million to $448.5 million at year-end 2025, partly due to a $250 million discretionary contribution.

- For the full year 2026, Unisys has issued financial guidance expecting constant currency revenue growth to be in the range of (6.5)% to (4.5)% and a non-GAAP operating profit margin between 9.0% and 11.0%.

- The ECS (ClearPath) segment is expected to maintain a 70% margin range and generate approximately $400 million per annum revenue, with AI viewed as a benefit driving consumption and minimal competition.

- The IT services segments (DWS and CANI) have a margin profile in the low- to mid-20s, with CANI having a larger Total Addressable Market (TAM) of ~$600 billion and a higher expected CAGR growth of 10%-12% compared to DWS's ~$150 billion TAM and 5%-8% CAGR.

- Unisys targets a normalized total company CAGR growth of 3%-5% in the medium term, despite current short-term macro challenges.

- The company has significantly reduced pension liability by $2.5 billion over the last five years, including a recent $320 million annuity in July, and anticipates full defeasance of the pension within three to five years, which is expected to improve net leverage to 2.5x or 2x.

- Management believes the ECS/L&S business alone is potentially worth more than the current market capitalization, and that resolving pension volatility and continued EBITDA improvement will significantly uplift the stock.

- Unisys reported FY24 revenue of ~$2 billion, Adjusted EBITDA of ~$290 million, and Free Cash Flow of ~$55 million.

- The company is targeting ~150 basis points annual gross margin expansion for its Tech-Enabled Services (Ex-L&S) segment, having achieved >600 basis points expansion from 2022 to 2024.

- In June 2025, Unisys issued $700 million in new senior secured notes and contributed $250 million to U.S. pension plans; by September 2025, it transferred $320 million in U.S. pension liabilities as part of a strategy to remove $600 million in U.S. pension liabilities by year-end 2026.

- As of September 30, 2025, Unisys reported total debt of $1,218.3 million, cash of $321.9 million, and a net leverage ratio of 3.7x.

- The ClearPath (L&S) segment is expected to maintain 70% margins and generate $400 million per annum revenue, with AI seen as a benefit and no significant competition.

- The IT services segments (DWS and CANI) are projected to have mid-20s margins, with Cloud, Applications & Infrastructure (CANI) having a larger Total Addressable Market (TAM) of $600 billion and a higher CAGR growth of 10%-12% compared to Digital Workplace Solutions (DWS).

- Unisys expects a total company CAGR growth of 3%-5% in the medium term and has an 80% recurring revenue mix. The company has improved its margin profile by 600 basis points over the last couple of years.

- Unisys has made significant progress in mitigating pension liability, removing $2.5 billion over the past five years and recently completing a $320 million annuity. The company anticipates full pension defeasance within three to five years, which is expected to normalize net leverage to 2.5x, potentially down to 2x.

- The CEO believes Unisys is significantly undervalued, with the ClearPath business alone potentially worth more than the current market cap, attributing this to market hesitancy regarding pension volatility and a lack of appreciation for the ClearPath business.

- Unisys's ClearPath Forward (ECS/L&S) segment is expected to maintain a 70% margin range and generate approximately $400 million per annum revenue, with AI seen as a benefit and minimal competition.

- The IT Services segments (DWS and CA&I) are projected to have a mid-20s margin profile, with CA&I offering a larger Total Addressable Market (TAM) of $600 billion and higher Compound Annual Growth Rate (CAGR) of 10%-12%.

- Unisys targets a total company 3%-5% CAGR growth in the medium term.

- The company has reduced its pension liability by $2.5 billion over the last five years and anticipates full defeasance within three to five years, which could enable a return of capital to shareholders, such as a buyback program.

Quarterly earnings call transcripts for UNISYS.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more