Amazon Stuns Wall Street With $200 Billion AI Bet—Largest Corporate Capex in History

February 5, 2026 · by Fintool Agent

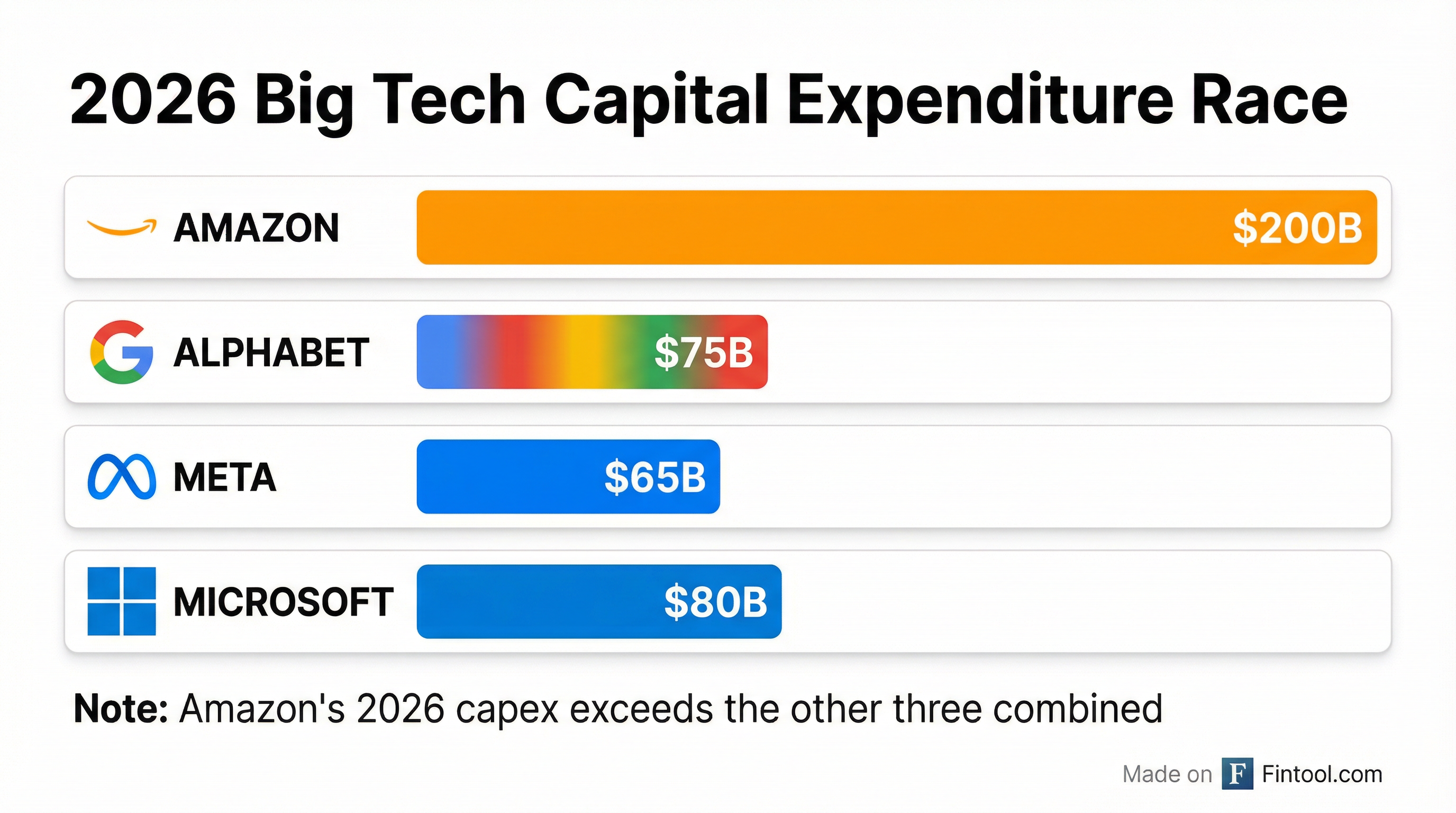

Amazon just dropped the biggest capital spending bomb in corporate history. In its fourth-quarter earnings release, CEO Andy Jassy announced the company expects to invest $200 billion in capital expenditures in 2026—a 53% increase from the roughly $131 billion spent in 2025 and more than the combined capex projections of Alphabet, Microsoft, and Meta.

Shares fell more than 4% to $222.69 following the announcement, erasing roughly $100 billion in market value despite the company beating revenue estimates. The message from investors is clear: this is an extraordinary bet on AI infrastructure with uncertain returns.

The Numbers That Matter

Amazon's Q4 2025 results were solid. Revenue rose 14% year-over-year to $213.4 billion, beating consensus estimates of $211 billion. Net income climbed to $21.2 billion, or $1.95 per diluted share, just shy of the $1.97 analyst estimate. Full-year 2025 revenue hit $716.9 billion with net income of $77.7 billion.

| Metric | Q4 2024 | Q4 2025 | YoY Change |

|---|---|---|---|

| Revenue | $187.8B | $213.4B | +14% |

| Operating Income | $21.2B | $25.0B | +18% |

| Net Income | $20.0B | $21.2B | +6% |

| EPS (Diluted) | $1.86 | $1.95 | +5% |

| AWS Revenue | $28.8B | $35.6B | +24% |

But the headline number wasn't earnings—it was capex. Amazon spent $131.8 billion on property and equipment in 2025, up 59% from $83 billion in 2024. And that was just the appetizer.

$200 Billion: Unpacking the Bet

"With such strong demand for our existing offerings and seminal opportunities like AI, chips, robotics, and low earth orbit satellites, we expect to invest about $200 billion in capital expenditures across Amazon in 2026, and anticipate strong long-term return on invested capital," Jassy said.

To put this in perspective:

The $200 billion figure dwarfs anything previously seen in corporate America. For context:

- Amazon's 2025 capex ($131.8B) was already the largest in the company's history

- Alphabet's 2026 projection is approximately $75 billion

- Microsoft's 2026 projection is approximately $80 billion

- Meta's 2026 projection is approximately $60-65 billion

Combined, the other three hyperscalers are spending roughly $220 billion. Amazon alone is approaching that figure.

AWS: The Engine Behind the Investment

The capex surge is inseparable from AWS's accelerating momentum. AWS revenue hit $35.6 billion in Q4, growing 24% year-over-year—its fastest growth rate in 13 quarters. Segment operating income reached $12.5 billion with a 35% margin.

| AWS Metric | Q4 2024 | Q4 2025 | YoY Change |

|---|---|---|---|

| Revenue | $28.8B | $35.6B | +24% |

| Operating Income | $10.6B | $12.5B | +18% |

| Operating Margin | 36.9% | 35.0% | -1.9pp |

For the full year, AWS generated $128.7 billion in revenue (+20%) and $45.6 billion in operating income (+15%).

The cloud business has become a flywheel: Amazon announced new AWS agreements with OpenAI, Visa, the NBA, BlackRock, Perplexity, Lyft, United Airlines, DoorDash, Salesforce, the U.S. Air Force, Adobe, Thomson Reuters, AT&T, S&P Global, HSBC, CrowdStrike, and more.

The Custom Silicon Advantage

Perhaps the most significant signal in the earnings release was the explosive growth of Amazon's custom chip business. Trainium and Graviton now have a combined annual revenue run rate exceeding $10 billion and are growing at triple-digit percentages year-over-year.

The chips roadmap is aggressive:

-

Trainium2: Fully subscribed with 1.4 million chips deployed, powering the majority of inference on Bedrock (used by 100,000+ companies) and Project Rainier—the world's largest operational AI compute cluster with 500,000+ Trainium2 chips used by Anthropic to train Claude

-

Trainium3: Now delivering production workloads with nearly all supply expected to be committed by mid-2026

-

Trainium4: Expected in 2027 with 6x the FP4 compute performance, 4x more memory bandwidth, and 2x more high-bandwidth memory capacity than Trainium3

-

Graviton5: The most powerful AWS CPU for broad cloud workloads, used by over 90% of the top 1,000 AWS customers, delivering up to 40% better price-performance than leading x86 processors

This vertical integration—designing chips purpose-built for AI workloads—gives Amazon a cost and performance advantage that competitors using primarily Nvidia silicon cannot easily replicate.

The Free Cash Flow Problem

The capex surge has consequences. Amazon's trailing twelve-month free cash flow collapsed to just $11.2 billion in 2025, down 71% from $38.2 billion the prior year. Operating cash flow remains strong at $139.5 billion (+20%), but nearly all of it is being plowed back into infrastructure.

| Cash Flow Metric | TTM Q4 2024 | TTM Q4 2025 | YoY Change |

|---|---|---|---|

| Operating Cash Flow | $115.9B | $139.5B | +20% |

| Capex (Net) | $77.7B | $128.3B | +65% |

| Free Cash Flow | $38.2B | $11.2B | -71% |

Jassy explicitly flagged "investment in artificial intelligence" as the primary driver of the capex increase. The bet is that AI infrastructure will generate outsized returns—but those returns are years away, while the cash goes out the door today.

Q1 2026 Guidance: More Investment Ahead

Amazon's first-quarter outlook signals no slowdown in the investment pace:

- Revenue: $173.5-$178.5 billion (11-15% growth)

- Operating Income: $16.5-$21.5 billion vs. $18.4 billion in Q1 2025

The guidance includes approximately $1 billion of higher year-over-year costs from Amazon Leo (Project Kuiper satellite constellation) as the company scales its low-earth orbit satellite business, plus investments in quick commerce and sharper international pricing.

The company also flagged supply chain risks, noting "resource and supply volatility, including for memory chips" as a factor that could affect results—a nod to the global HBM shortage that's constraining AI chip production across the industry.

Beyond AWS: The Broader Business

The retail and advertising segments continued their steady performance:

Advertising grew 23% year-over-year to $21.3 billion in Q4, making it one of Amazon's fastest-growing and highest-margin businesses.

North America stores posted operating income of $11.5 billion on revenue of $127.1 billion, a 9% operating margin—a dramatic improvement from the margin squeeze of 2022-2023.

Subscription services (Prime, streaming, etc.) grew 14% to $13.1 billion.

Rufus, Amazon's AI shopping assistant, was used by over 300 million customers and drove nearly $12 billion in incremental annualized sales.

Thursday Night Football on Prime Video had its most-watched season ever, averaging 15+ million viewers with 16% year-over-year growth.

What to Watch

1. Can Amazon monetize the infrastructure? The $200 billion bet only pays off if AWS can translate capacity into proportional revenue growth. Any signs of slowing cloud demand or pricing pressure will intensify scrutiny.

2. Custom chip adoption rates. If Trainium and Graviton continue their triple-digit growth, Amazon's cost structure improves significantly. But memory shortages and competition from Nvidia's ecosystem remain risks.

3. Free cash flow recovery. Bulls will want to see operating cash flow grow faster than capex by 2027, restoring the company's ability to return capital to shareholders.

4. Project Kuiper execution. The satellite business is absorbing billions with revenue contribution still minimal. Timeline slippage would compound investor concerns.

5. Memory chip supply. The company explicitly flagged memory chip volatility as a risk factor. Extended shortages could delay infrastructure buildouts or squeeze margins.

Related Companies: Amazon | Alphabet | Microsoft | Meta | Nvidia