Blue Owl Permanently Halts Redemptions, Raising Alarms About $1.8 Trillion Private Credit Market

February 19, 2026 · by Fintool Agent

Blue Owl Capital has permanently eliminated quarterly redemptions from one of its retail-focused private credit funds after selling $1.4 billion in assets—a move that sent shockwaves through alternative asset managers and prompted one of the industry's most respected voices to warn of echoes from the 2008 financial crisis.

Shares of Blue Owl plunged to their lowest level in two and a half years on Thursday, dragging down Apollo, Blackstone, KKR, Ares, and TPG as the industry confronted uncomfortable questions about what happens when investors in "semi-liquid" private credit funds want their money back.

The $1.4 Billion Fire Sale

Blue Owl said Wednesday it had agreed to sell $1.4 billion in direct lending investments across three funds to four North American pension and insurance investors, with the loans changing hands at 99.7% of par value.

The largest sale—$600 million representing roughly 34% of its $1.7 billion portfolio—came from Blue Owl Capital Corporation II (OBDC II), a semi-liquid private credit strategy aimed at U.S. retail investors.

Following the deal, Blue Owl announced that OBDC II would permanently end regular quarterly liquidity payments to investors. Instead, the business development company will pivot to periodic payouts funded by asset sales, earnings, repayments, and other strategic deals.

"We aren't halting redemptions," insisted Craig Packer, co-President of Blue Owl Capital, on an earnings call Thursday. "We've been tendering for 5% of the shares of this fund for eight years. Instead of resuming 5% a quarter, we are in fact accelerating redemptions. And we're going to return to this investor group 30% of their capital at book value in the next 45 days."

The "Canary in the Coal Mine" Question

The market's reaction was swift and severe. Former Pimco CEO Mohamed El-Erian posted to X asking the question on everyone's mind:

"Is this a 'canary-in-the-coalmine' moment, similar to August 2007?"

The reference was pointed: In August 2007, two Bear Stearns hedge funds that invested in subprime mortgages collapsed—a warning signal that preceded the 2008 financial crisis. The parallels El-Erian draws center on liquidity mismatches: funds that promised investors regular redemptions while holding illiquid assets that couldn't be easily sold.

Blue Owl's management pushed back, arguing the 99.7% par sale was validation of their marks. "There's skepticism about marks. There's skepticism about valuation. We've always been saying we feel really good about the quality of our portfolio and the quality of our marks, but just saying it in some ways doesn't seem to have done enough. So we're putting our money where our mouth is," Packer said.

Redemption Requests Spiked 200%

The move comes amid a surge in withdrawal requests across the industry. Investors in BDCs holding more than $1 billion asked to pull a total of more than $2.9 billion in the fourth quarter of 2025—up 200% from the prior period—according to Robert A. Stanger & Co., a boutique investment bank that tracks the industry.

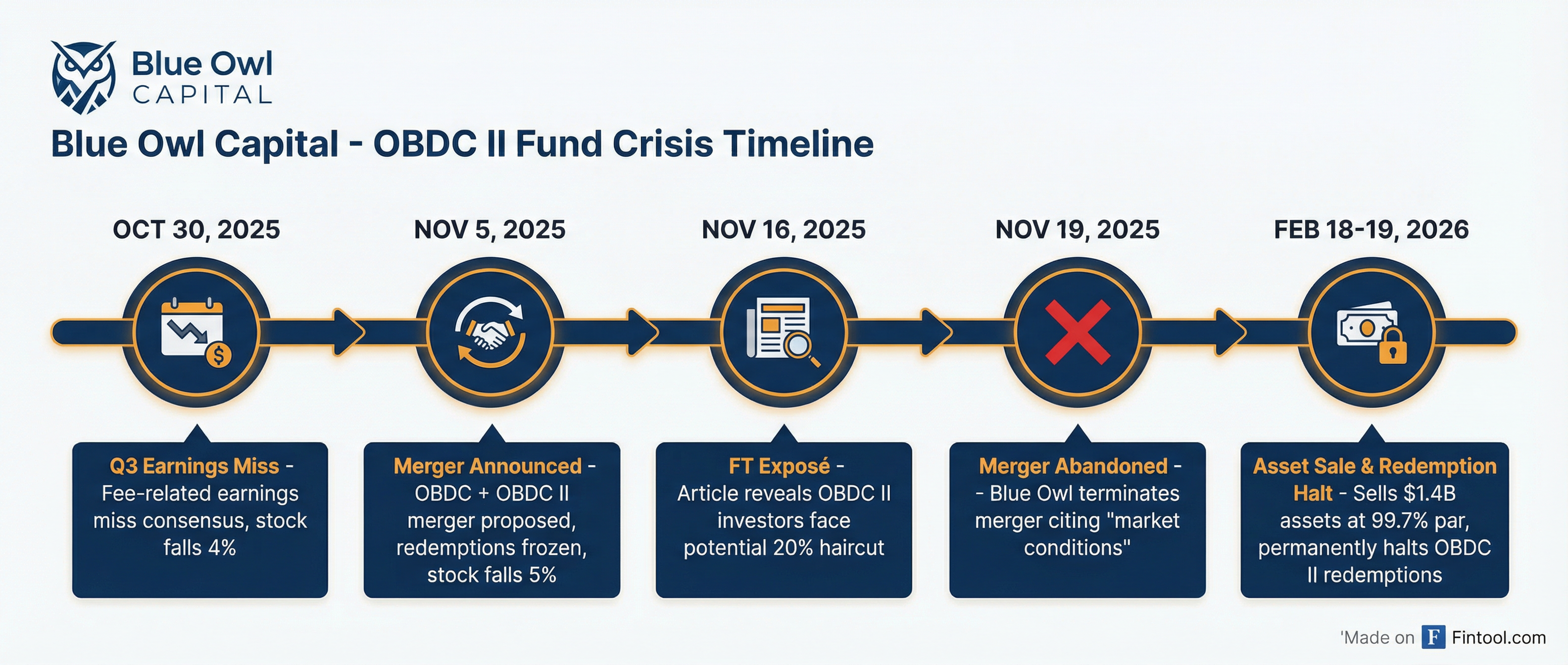

This latest episode follows a turbulent few months for Blue Owl:

| Date | Event | Stock Impact |

|---|---|---|

| Oct 30, 2025 | Q3 earnings miss; fee-related earnings of $376.2M below consensus | -4.2% |

| Nov 5, 2025 | OBDC/OBDC II merger announced; OBDC II redemptions frozen | -4.7% |

| Nov 16, 2025 | FT reveals OBDC II investors face potential 20% haircut | -5.8% |

| Nov 19, 2025 | Blue Owl terminates merger citing "current market conditions" | - |

| Feb 18-19, 2026 | $1.4B asset sale; permanent redemption halt announced | -24% YTD |

Contagion Across Private Equity

The selloff wasn't limited to Blue Owl. The news "rekindled fears in an industry that has attracted increasing scrutiny in recent months over valuations in the market and the quality of lending to firms with heavy debt loads and often little track record."

| Firm | Feb 19 Close | Daily Change | YTD Performance |

|---|---|---|---|

| Blue Owl (OWL) | $11.58 | - | -24.4% |

| TPG | $44.58 | -3.4% | -32.2% |

| Apollo | $118.34 | -3.4% | -19.3% |

| Blackstone | $125.76 | -2.6% | -20.8% |

| Ares | $129.85 | +0.3% | -21.9% |

| KKR | $101.64 | -1.0% | -21.1% |

Blue Owl closed 2025 with $307.4 billion in assets under management, up 22% from $251.1 billion at the end of 2024. Fee-paying AUM reached $187.7 billion, with direct lending accounting for $115 billion of total AUM. The firm generated $1.5 billion in fee-related earnings in 2025, up 19% year-over-year.

The Bigger Picture: Private Credit's Retail Push

The episode underscores growing tensions in the $1.8 trillion private credit market as firms that built their businesses on institutional capital increasingly target retail investors hungry for yield.

Semi-liquid funds like OBDC II were designed to bridge the gap—offering quarterly redemption windows while investing in loans that don't trade on exchanges. The model works when withdrawals stay manageable. It breaks down when too many investors want out at once.

"Funds that let investors redeem periodically can face pressure when too many people want their money back at once. Managers often keep some more easily sold assets to meet withdrawals. Selling directly originated loans, which typically don't trade often, is less common," Bloomberg noted.

What to Watch

Near-term: Blue Owl says it could return half of OBDC II investors' capital by year-end through distributions funded by repayments, earnings, and potential additional asset sales.

Industry contagion: Watch for similar moves at other BDCs if redemption pressure persists. The Stanger data showing 200% quarter-over-quarter spikes in withdrawal requests suggests the problem isn't isolated.

Regulatory scrutiny: Private credit's rapid growth into retail channels has already drawn attention from regulators concerned about liquidity mismatches and transparency. Blue Owl's episode may accelerate that focus.

Valuations: The 99.7% par sale validates Blue Owl's marks for now, but questions linger about whether all private credit portfolios would fare as well in a forced sale scenario.

Related

- Blue Owl Capital - Company Research

- Apollo Global Management - Company Research

- Blackstone - Company Research

- KKR & Co. - Company Research

- Ares Management - Company Research

- TPG Inc. - Company Research