CN CEO Robinson Calls UP-NS Merger 'Threat to Competition' at Barclays Conference as STB Deadline Looms

February 17, 2026 · by Fintool Agent

Canadian National Railway CEO Tracy Robinson delivered a pointed critique of the proposed Union Pacific-Norfolk Southern merger at Barclays' 43rd Annual Industrial Select Conference in Miami today, calling it a direct "threat to competition" just hours before the Surface Transportation Board's deadline for the applicants to respond to last month's rejection of their filing.

"If you imagine these two railroads coming together, and one railroad will have—I don't know what the number is—say, 50% of the nation's freight. No matter, it's not an end-to-end, there's areas on the two networks where you will, in effect, see a reduction in competition," Robinson told the conference. "It's difficult to imagine how bringing together those two railroads and having one railroad that large is going to reach that hurdle."

CN shares closed at $107.60, up 0.3% and trading near their 52-week high of $108.75.

STB Deadline Day Arrives

The timing of Robinson's comments is significant. The STB rejected Union Pacific and Norfolk Southern's 6,700-page merger application on January 16, finding it incomplete due to missing market share projections and contract schedules. The Board gave applicants until today, February 17, 2026, to indicate whether and when they plan to refile.

If UP and NS choose to refile, they must submit a complete revised application by June 22, 2026. The STB emphasized its rejection was procedural, not a judgment on the merger's merits.

Robinson said CN has done its homework on potential impacts: "If this is approved, I mean, we know there will be an impact to us. We've done our work. I think we'll have the smallest impact. We're a bit ring-fenced. We originate 85% of our volume, and we originate and terminate 65% of our volume. I think we're unique in the industry that way."

But she made clear CN won't sit idle: "There are certain areas on the continent where we would look for the ability to get into new markets, the ability to serve customers that we don't serve right now, and enhance that through the ability to increase competition. There's various mechanisms, so pricing, trackage rights, those kinds of things."

Building the 'Operating Leverage Engine'

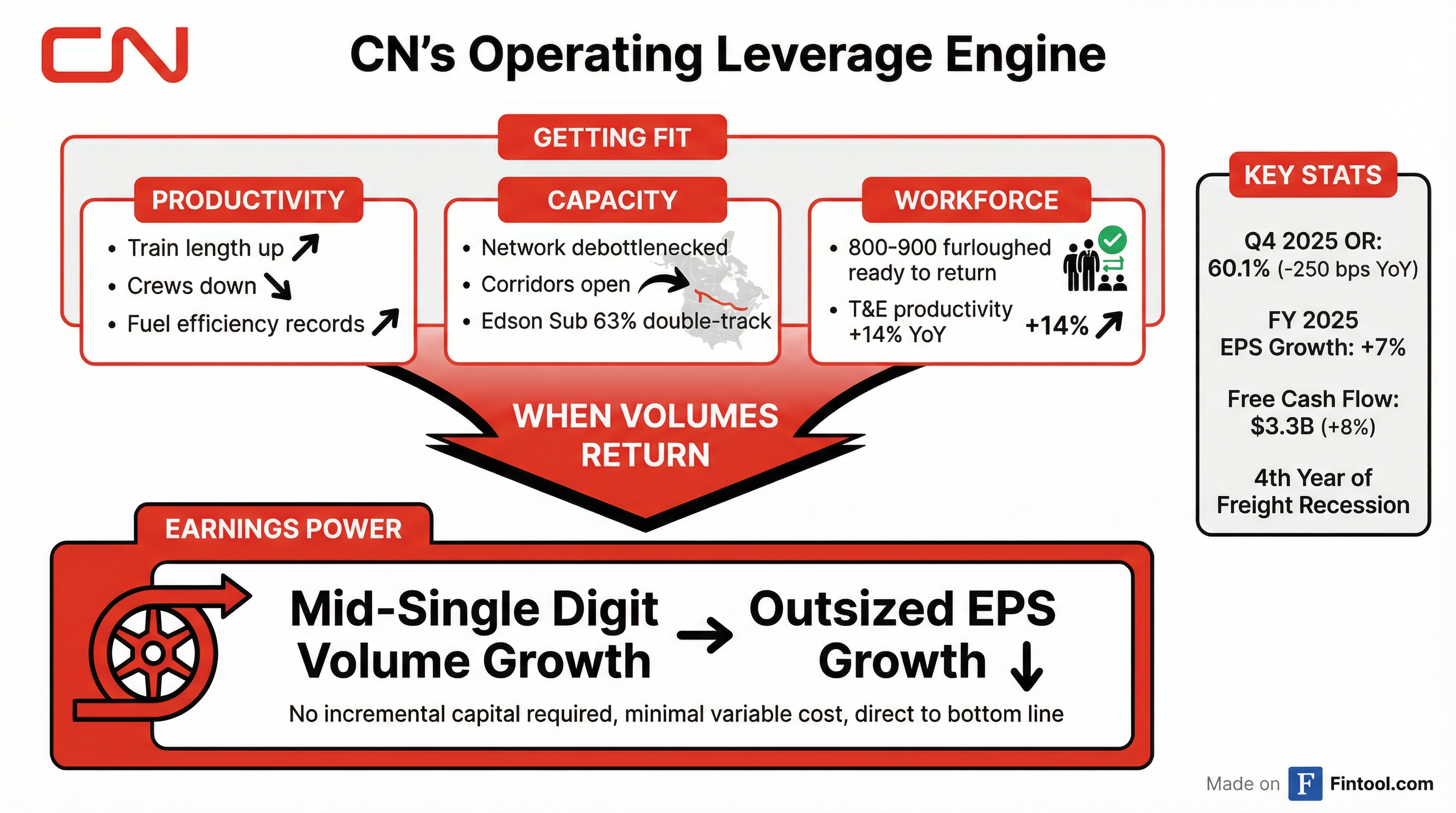

Beyond merger politics, Robinson used the conference to reinforce CN's strategy of "getting fit" during what she called an unprecedented "fourth year of a freight recession."

"At the beginning of every year, we all look at it and say, 'Perhaps by the end of this year, we'll be turning.' I can tell you, we're not counting on that, but we're ready for when it happens," she said.

CN delivered Q4 2025 adjusted EPS of C$2.08, up 14% year-over-year—the best in the industry—on just 4% RTM growth. The operating ratio improved 250 basis points to 60.1%, while full-year free cash flow reached C$3.3 billion.

| Metric | Q4 2024 | Q4 2025 | Change |

|---|---|---|---|

| Revenue (USD) | $3.03B | $3.26B | +7.5%* |

| Operating Ratio | 62.6% | 60.1% | -250 bps |

| Adjusted EPS (CAD) | C$1.82 | C$2.08 | +14% |

| Free Cash Flow (CAD) | C$3.1B | C$3.3B | +8% |

*Values retrieved from S&P Global

Robinson detailed the operational improvements driving results: "We are running faster with less dwell, fewer locomotives. Our locomotives are working harder. Our trains are longer and heavier than they were before."

The company now has 800-900 furloughed workers ready to return when volumes recover, and has completed major capital projects including debottlenecking the Edson Subdivision to 63% double-track capacity.

Tariff Uncertainty Clouds 2026 Outlook

CN shifted to "directional guidance" for 2026 given elevated macro uncertainty, particularly around the USMCA renegotiation.

"It's going to be a year of the reset or the renewal of the USMCA. So not a lot of clarity on where trade flows are going to end up this year," Robinson acknowledged.

2026 Guidance Framework:

- Volumes: Flat with 2025 (assumes current tariff levels persist)

- EPS growth: Slightly exceeding volume growth

- CapEx: C$2.8 billion (down C$500 million from 2025)

- Leverage: Temporarily increasing to 2.7x for buybacks, returning to 2.5x in 2027

Tariffs remain the elephant in the room. Robinson said they cost CN approximately C$350 million in 2025, primarily from 50% duties on steel, aluminum, and forest products imposed in mid-2025.

"When those tariffs got to 50%... At 25%, we were still moving volumes cross-border. When they hit 50%, we're not," she explained. "Aluminum has been going into more export markets. Aluminum is now moving again, even at a 50% tariff rate across the border."

The mix headwinds compound the volume challenge: forest products and metals are among CN's highest-margin businesses. "We backfilled it, but not always with the same level of margin business," Robinson noted.

The Bright Spots: Grain, Potash, and Domestic Intermodal

Not all segments are struggling. Robinson highlighted several growth areas:

Grain: "We hit records on moving grain in September through December of last year, almost records for the history of the company. We hit a, I think we're second from the history of the company in January, from a volume perspective on grain."

Potash: "We're being surprised a little bit on the upside of potash, which is good for us."

Domestic Intermodal: "Domestic intermodal continues to grow, and this is largely on the backs of some really good service. We continue to pick up share, and it has grown, I think, in every quarter through last year."

Prince Rupert: The Gemini service at Prince Rupert port "has been a very strong outcome for us, and we're expecting that to continue."

Looking ahead, Robinson pointed to CN's unique positioning on North America's natural resource base: "The growth in energy that's coming, whether it's in NGLs, whether it's in refined fuels, the growth in the mining sectors, the potash, the coal, the metallurgical coal, the frac sand. When it comes, we'll have considerable operating leverage."

Stock Lags Peers on Freight Recession Concerns

Despite the strong Q4 execution, CN shares have underperformed rail peers since the start of 2025:

Norfolk Southern's 34% gain largely reflects merger speculation, while CSX has benefited from its own operating improvements. CN's 5.6% return trails the group as investors weigh tariff uncertainty against the company's long-term leverage story.

| Railroad | Stock Price | Market Cap | YTD Return (2025) |

|---|---|---|---|

| Norfolk Southern | $314.94 | $70.7B | +34.2% |

| CSX Corp. | $40.87 | $49.3B | +27.1% |

| Union Pacific | $248.50 | $147.8B | +13.8% |

| Canadian National | $107.60 | $65.9B | +5.6% |

AI and the Future of Railroading

Robinson also offered insights on CN's AI initiatives, noting the technology's long history in railroad operations: "If you think about technology and AI in its various forms, we've been at this for a long time, largely on the operations side. So it's around how we run our trains, most particularly how we inspect the infrastructure and how we inspect the rolling stock."

But she sees much bigger changes ahead: "As I get more informed and educated on AI and the capabilities, this is amazing, and I do think that in the next five years, much of the work that each of us does will be very different. We're going to be able to use our human resources in a very different way."

What to Watch

Near-term catalysts:

- UP-NS response to STB today (February 17)

- USMCA review timeline with July as key milestone

- Q1 2026 expected to be "the toughest quarter" on comparisons

Medium-term catalysts:

- Potential aluminum tariff relief as U.S. inventories deplete

- Phase 2 Greater Toronto Area Fuel Terminal

- New fractionators and crude oil expansion projects

- CanExport facility ramp-up (grain, plastics exports)

Robinson's closing message to investors: "We are really focused on controlling what we can control... You're gonna see us do a bit of a reset this year, but we'll be talking to you next year as the volumes come back on considerable earnings leverage."

Related: