Walmart Beats Q4 Estimates But Cautious Guidance Signals Consumer Jitters

February 19, 2026 · by Fintool Agent

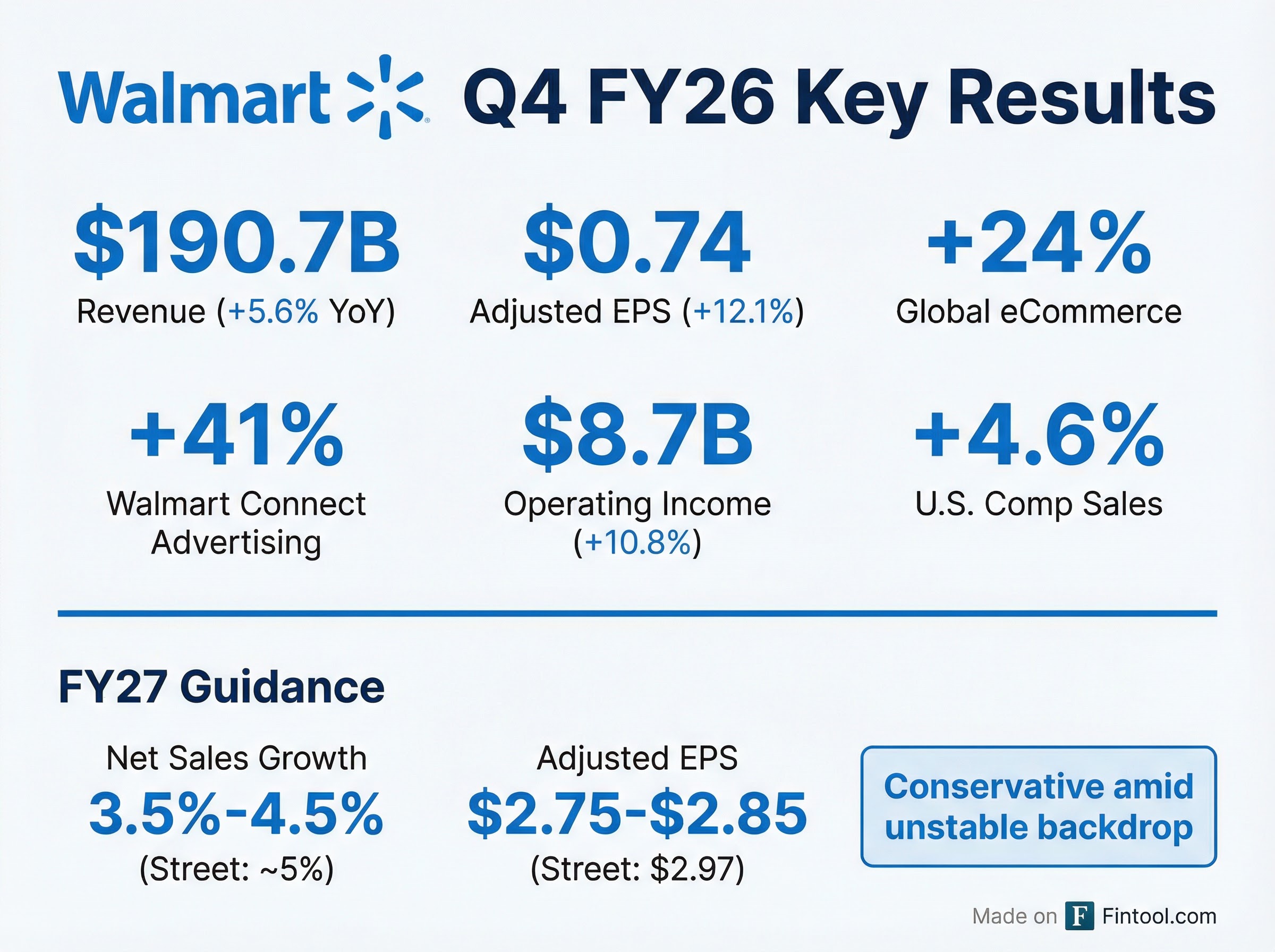

Walmart delivered a strong fourth quarter—adjusted EPS of $0.74 beating consensus by a penny and global eCommerce surging 24%—but the world's largest retailer sent shares tumbling with fiscal 2027 guidance that fell meaningfully short of Wall Street expectations.

The guidance miss, paired with management's description of the economic backdrop as "somewhat unstable," suggests the retail giant is bracing for a more challenging consumer environment even as its own execution remains strong.

The numbers:

| Metric | Q4 FY26 Result | YoY Change | vs. Consensus |

|---|---|---|---|

| Revenue | $190.7B | +5.6% | Beat |

| Adjusted EPS | $0.74 | +12.1% | Beat by $0.01 |

| Operating Income | $8.7B | +10.8% | — |

| U.S. Comp Sales | +4.6% | Flat YoY | — |

| Global eCommerce | +24% | — | — |

| Walmart Connect (Ad Revenue) | +41% | — | — |

FY27 Guidance: The Real Story

While Q4 delivered, fiscal 2027 guidance is where the market found reason for concern:

| Metric | FY27 Guidance | Street Consensus | Gap |

|---|---|---|---|

| Net Sales Growth (cc) | 3.5%–4.5% | 5.0% | 50-150 bps light |

| Adj. Operating Income Growth (cc) | 6.0%–8.0% | 11.3% | Significantly light |

| Adjusted EPS | $2.75–$2.85 | $2.97 | 4-8% below |

CFO John David Rainey acknowledged the conservative posture, noting the company has outperformed initial guidance in each of the past three years. "We want to maintain maximum flexibility as we sit here at this point in the year," he said.

The guidance also embeds a ~100 basis point headwind from Maximum Fair Pricing legislation on prescription drugs, which Walmart expects to impact the health and wellness business throughout the year.

Consumer Signals: Affluent Gains, Lower-Income Stress

New CEO John Furner's first earnings call offered a nuanced portrait of the American consumer. The majority of Walmart's market share gains continue to come from households earning more than $100,000—a trend that has persisted for several quarters.

"The customer is choiceful in their spending," Furner said. "For households earning below $50,000, we continue to see that wallets are stretched, and in some cases, people are managing spending paycheck to paycheck."

Despite the bifurcation, even lower-income consumers are increasingly prioritizing convenience nearly as much as price—a structural shift that plays directly into Walmart's omnichannel investments.

Management also flagged that the government shutdown earlier in the quarter temporarily impacted sales as benefit payments were delayed. The impact "recovered as the quarter went on" for Walmart U.S. but lingered somewhat at Sam's Club.

eCommerce: Now Profitable and Accelerating

Perhaps the brightest spot in the quarter: Walmart's digital business hit profitability milestones that management barely discusses anymore internally—because they're so far past break-even.

U.S. eCommerce highlights:

- Sales up 27% in Q4, with 23% digital mix (record high)

- Store-fulfilled delivery under 3 hours represented 35% of orders

- "Fast delivery" (under 3 hours) grew 60% year-over-year

- eCommerce now profitable in all four quarters with double-digit incremental margins

"We've reached a point where we don't even really talk about this internally anymore," CFO Rainey said of eCommerce profitability. "The momentum is only upward from here."

The shift has been rapid: eCommerce represented just 17.5% of sales two years ago versus 23% today—a 550 basis point expansion.

Advertising & Membership: The High-Margin Engines

Walmart's alternative profit pools continued their rapid ascent:

| Segment | Q4 Growth | Full Year Revenue |

|---|---|---|

| Global Advertising | +37% | $6.4B |

| Walmart Connect (U.S.) | +41% | — |

| Global Membership Fees | +15.1% | $4.3B+ |

Notably, advertising and membership fees now represent nearly one-third of Walmart's operating income—a structural transformation in the business model.

The VIZIO acquisition, which closed in December, contributed triple-digit advertising growth in Q4 as Walmart gains another channel to reach consumers via connected TV.

Walmart+ membership income grew double-digits in the U.S., with the recently launched One Pay Cash Rewards credit card driving incremental sign-ups.

Agentic Commerce: Sparky Drives Bigger Baskets

Walmart leaned heavily into AI and "agentic commerce" during the call—and the early metrics are compelling.

Sparky (Walmart's AI shopping assistant):

- Roughly half of app users have engaged with Sparky

- Customers using Sparky have 35% higher average order values

- Engagement and user adoption accelerated significantly from Q3 to Q4

"Sparky is essentially helping us evolve from traditional search to intent-driven commerce," said Dave Guggina, the new head of Walmart U.S. "Better discovery and higher conversion translates into bigger baskets and greater frequency."

CEO Furner positioned agentic AI as central to the omnichannel strategy: "When Sparky builds a basket, we execute it through fast delivery, pickup, or in-store, turning AI engagement into immediate physical outcomes."

Walmart also announced partnerships with Alphabet and OpenAI to expand AI capabilities globally.

Segment Performance

Walmart U.S.

The core business delivered 4.6% comp sales growth with strength across merchandise categories:

- Grocery: Mid-single-digit growth led by pantry and fresh; grocery inflation +0.6% (down ~70 bps sequentially)

- General Merchandise: Returned to low single-digit growth, led by fashion and auto care

- Health & Wellness: High single-digit growth despite ~200 bps headwind from Maximum Fair Pricing

Inventory management remained tight, up just 2.9%—roughly half the rate of sales growth. Management noted they may have "bought a bit light" in certain hot categories but prefer entering Q1 clean with momentum.

Walmart International

International delivered standout profit growth:

- Operating income up 36.0% reported, +26.5% in constant currency

- China eCommerce now exceeds 50% of total sales in that market

- Opened 128 new stores in Q4

The segment benefited from improved eCommerce economics and lapping prior-year strategic investments.

Sam's Club U.S.

- Comp sales +4.0% (excluding fuel), driven by transaction growth

- eCommerce +23%, now 19% of net sales

- Membership fee revenue +6.1%, with strength among Gen Z and Millennials

- Club-fulfilled express delivery sales up 80%

Capital Allocation: $30 Billion Buyback

The board authorized a new $30 billion share repurchase program—Walmart's largest ever—replacing the prior authorization.

Other capital highlights:

- Operating cash flow: $41.6B (+$5.1B YoY)

- Free cash flow: $14.9B (+18% YoY)

- Capital expenditures: ~3.5% of sales (peak spending on supply chain automation)

- Dividend increased to $0.99/share annually

Management noted capex is at "peak annual spending levels on supply chain automation and store remodels" and expects to see returns accelerate as these investments mature.

What to Watch

-

Consumer health through Q1: Management is monitoring tax refund timing and spending patterns closely. The guidance assumes refunds are higher this year but leaves uncertainty around how much gets saved vs. spent.

-

General merchandise recovery: Fashion has been a bright spot for multiple quarters with mid-single-digit growth. Continued momentum here would improve category mix and margins.

-

Agentic commerce adoption: If Sparky engagement continues to accelerate with 35%+ AOV uplift, the flywheel effect on eCommerce economics could be significant.

-

International margin expansion: With new leadership under Chris Nicholas (formerly of Sam's Club China), international is positioned to deploy U.S.-developed technology platforms globally.

-

Tariff uncertainty: Management flagged tariff and trade policies as material uncertainties in guidance. The company navigated a "bumpy tariff environment" in FY26 with a 300 bps headwind to operating income growth from claims and tariff-related costs.

The Bottom Line

Walmart's Q4 demonstrated that the company's omnichannel transformation is working—operating income growing at twice the rate of sales, eCommerce firmly profitable, and alternative profit streams nearing one-third of operating income. The 24% eCommerce growth and 41% Walmart Connect expansion show no signs of slowing.

But the cautious FY27 guide—particularly the EPS range of $2.75-$2.85 versus Street expectations of $2.97—reflects management's view that the consumer backdrop remains uncertain. The split continues: affluent households are driving share gains while lower-income consumers feel squeezed.

For investors, the tension is clear: Walmart is executing exceptionally well, but it's choosing to guide conservatively in an environment it describes as "somewhat unstable." History suggests the company will beat these numbers—it has for three consecutive years. The question is whether macro conditions cooperate.