BP Halts Buybacks for First Time Since 2020 as Oil Major Pivots to Balance Sheet Repair

February 10, 2026 · by Fintool Agent

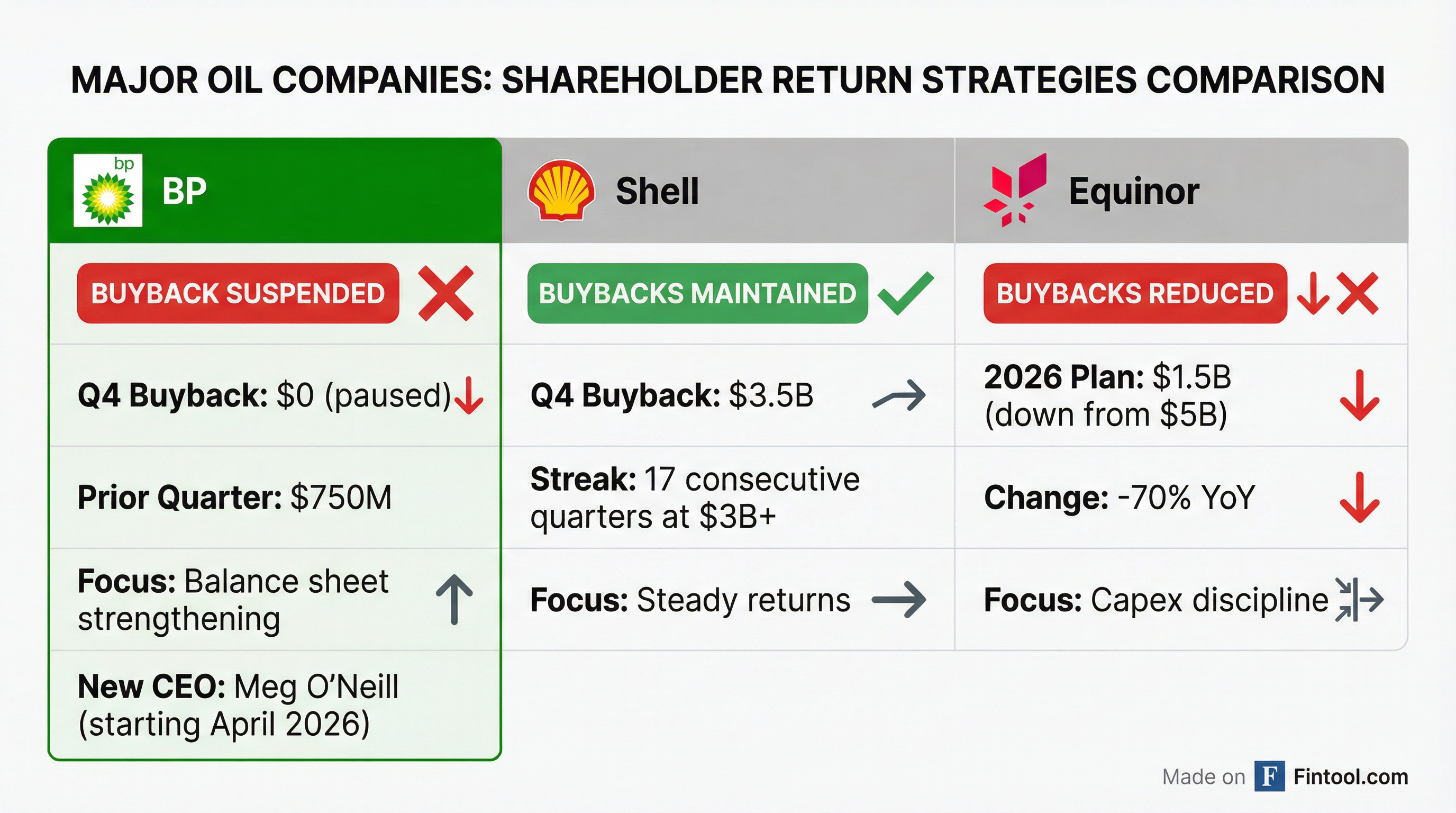

BP suspended its quarterly share buyback program on Tuesday for the first time since the pandemic-induced crisis of 2020, marking a decisive shift in capital allocation as the British oil major prioritizes balance sheet repair over shareholder returns.

The move comes alongside a $4 billion write-down on the company's renewables and biogas businesses and arrives just two months before new CEO Meg O'Neill—recruited from Australia's Woodside Energy—takes the helm in April.

BP shares fell as much as 5% in early trading, underperforming peers as investors digested the retreat from a buyback program that had become a fixture of the company's capital return framework.

The Numbers

BP posted Q4 2025 underlying replacement cost profit of $1.54 billion, matching analyst expectations, but full-year profit fell 17% to $7.49 billion as lower oil prices weighed on results.

| Metric | Q4 2025 | Q3 2025 | Q4 2024 |

|---|---|---|---|

| Underlying RCP ($B) | $1.54 | $1.16* | $1.20* |

| Operating Cash Flow ($B) | $7.6 | $6.1* | $6.8* |

| Organic CapEx ($B) | $3.5 | $3.2* | $4.2* |

| Net Debt ($B) | $22.2 | $39.8* | $27.1* |

| Buyback | $0 (suspended) | $750M | $1.5B |

*Values retrieved from S&P Global

CFO Kate Thomson framed the decision in stark terms: "The board has decided to suspend the share buyback and fully allocate excess cash to accelerate strengthening of our balance sheet as a priority. This creates a stronger and more resilient platform to invest with discipline into our distinctive deep hopper of oil and gas opportunities."

Perhaps most significantly, BP retired its long-standing guidance to return 30-40% of operating cash flow to shareholders through distributions.

Oil Majors Diverge on Shareholder Returns

BP's buyback suspension stands in stark contrast to peer strategies. Shell maintained its $3.5 billion quarterly buyback last week—marking its 17th consecutive quarter at $3 billion or more—while Equinor opted to reduce rather than eliminate buybacks, cutting its 2026 program to $1.5 billion from $5 billion in 2025.

The divergence reflects BP's weaker starting position. Net debt at year-end 2025 stood at $22.2 billion, still elevated despite an $800 million reduction from year-end 2024. By contrast, Shell has maintained more consistent leverage, giving it flexibility to sustain shareholder returns even as profits compress.

The $4 Billion Renewables Write-Down

The quarterly results included a painful reckoning with BP's energy transition investments. The company recognized approximately $4 billion in after-tax impairments, largely related to its biogas and renewables businesses.

Thomson characterized these as deliberate portfolio decisions: "These impairment charges are related largely to our transition businesses, including biogas and renewables, where we took the deliberate decision to manage our pace of growth and high grade our portfolio to maximize returns."

While the charges are non-cash, they reflect a broader strategic retreat from BP's once-ambitious low-carbon pivot. The company acknowledged the underlying reality: "While these are non-cash adjustments in our financial results, we recognize that every impairment reflects a prior capital outlay. We are committed to doing better for our shareholders on capital allocation."

Including the impairments, inventory losses, and other adjusting items, BP reported a Q4 IFRS loss of $3.4 billion.

Strategic Reset: $20 Billion Divestment Program Accelerates

BP's capital discipline extends beyond suspended buybacks. The company has now completed or announced more than $11 billion in divestments—more than halfway toward its $20 billion disposal target in just one year.

The centerpiece remains the Castrol sale announced in December, with approximately $6 billion in net proceeds expected to close in the second half of 2026 and be fully deployed toward debt reduction.

The company also raised its structural cost reduction target to $5.5-6.5 billion by 2027, up from $4-5 billion, reflecting the Castrol divestiture and broader efficiency initiatives.

| Divestment Program | Status |

|---|---|

| Total Target | $20B |

| Completed/Announced | >$11B |

| Castrol (pending) | $6B |

| 2025 Proceeds Received | $5.3B |

| 2026 Expected Proceeds | $9-10B |

New CEO Inherits a Work in Progress

Meg O'Neill, the Woodside Energy executive tapped to succeed Murray Auchincloss, inherits a company mid-transformation when she takes over in April.

The operational picture has stabilized: BP reported record-high upstream plant reliability, started up seven new major projects, and achieved a 90% reserves replacement ratio—up from around 50% on average in the prior two years.

The Bumerangue discovery offshore Brazil, BP's largest find in 25 years, holds an estimated 8 billion barrels of liquids in place, with appraisal drilling expected to begin by year-end.

But the financial challenge remains formidable. Return on average capital employed improved to 14% in 2025 from 12% in 2024 on a price-adjusted basis, but that still trails the returns Shell and Exxonmobil generate from their portfolios.

2026 Outlook: A Year of Two Halves

Management guided for a challenging first half of 2026:

- Production: Broadly flat on an underlying basis, with oil operations stable and gas/low-carbon energy declining

- CapEx: $13-13.5 billion, weighted to the first half

- Divestment proceeds: $9-10 billion expected, weighted to the second half

- Net debt: Expected to increase through H1 2026 before falling significantly in H2 as Castrol proceeds arrive

Thomson acknowledged the timing mismatch: "Reflecting the timing of these factors, and of course, subject to macro environment and prices, we expect net debt to firstly increase through the first half of 2026, before falling significantly in the second half."

What to Watch

Near-term catalysts:

- Meg O'Neill's April start and potential strategy refresh

- Castrol transaction closing (expected H2 2026)

- Q1 2026 results to confirm net debt trajectory

- Oil price trajectory—BP remains acutely sensitive to Brent movements

Longer-term questions:

- Will the buyback resume once leverage targets are hit?

- Does O'Neill pursue further portfolio rationalization?

- Can BP close the return gap with peers?

The last time BP suspended buybacks in 2020, oil was trading near $20 per barrel and the entire industry was in survival mode. This time, with Brent hovering around $75, the decision reflects something more fundamental: a company that overextended in the energy transition and is now scrambling to rebuild financial flexibility ahead of what management hopes will be a fresh start under new leadership.