Fortive CEO Defends Software Moats at Citi Conference: 'AI Is an Accelerant, Not a Disruptor'

February 17, 2026 · by Fintool Agent

Fortive CEO Olumide Soroye used his presentation at Citi's 2026 Global Industrial Tech and Mobility Conference to push back on concerns that AI could disrupt the company's software businesses, arguing that proprietary data, network effects, and regulatory moats make Fortive the "trusted partner" customers are turning to for AI deployment rather than a disruption target.

"We came into this journey with some advantages," Soroye told the audience, noting that Fortive established an AI center of excellence in 2017. "As exciting as Gen AI and Agentic AI has been, especially the last several months here, it wasn't a new initiative for us."

Shares of the industrial technology company closed at $56.81, down 0.2% on the day, valuing the post-spin company at approximately $18 billion. The stock has traded in a range of $45.50 to $62.79 over the past 52 weeks.

The Software Moat Thesis

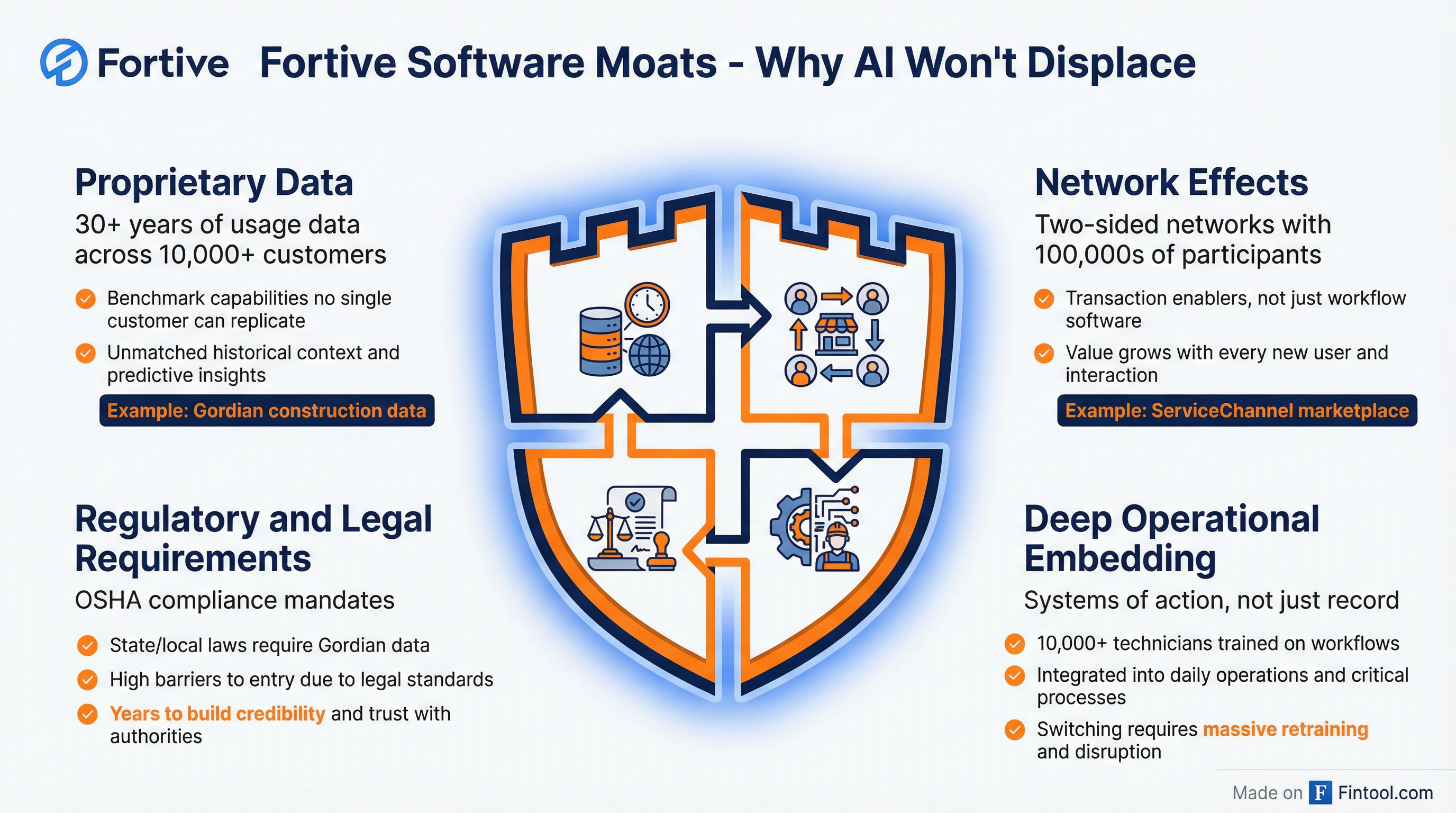

The AI defensibility question—increasingly common at industrial conferences as investors assess which software businesses face displacement risk—drew a detailed response from Soroye, who outlined four specific moats protecting Fortive's software portfolio:

1. Proprietary Data: "Not just do you have data, but do you have data that no single customer can get? Because you have it across 10,000 customers, and you have it over 30 years, and nobody else has the usage rights you have to that data."

2. Network Effects: Fortive's ServiceChannel business operates as a two-sided marketplace with "hundreds of thousands of participants in a transaction on one side... and equivalent number on the other side of a transaction. So it's a meeting place more than it is a workflow software platform."

3. Regulatory and Legal Requirements: At Gordian, the construction procurement data business, "it's written into the law in some state and local jurisdictions that you have to use the data," Soroye explained.

4. Deep Operational Embedding: "Even if you change it out, you have to go retrain 10,000 people for months for them to do their job."

AI as Accelerant: Internal and Customer-Facing

Rather than viewing AI as a threat, Soroye framed it as a competitive advantage multiplier. Fortive's AI center of excellence, originally focused on machine learning and data analytics, has been "infused into our Fortive Business System" and democratized across all operations.

Internal productivity gains:

- Customer operations teams using agentic AI tools for sales and support

- Product development teams seeing "significant increase in the output with the same resource base"

- G&A functions deployed across the AI capability stack

Customer-facing innovation:

- Fluke deploying AI copilots to help technicians use products more effectively

- Data center certification guidance systems for complex applications

- Every software company has "launched something and has a roadmap of additional AI use cases to come"

The 'New Fortive' Strategy: Two Quarters In

This was Soroye's opportunity to update investors on the Fortive Accelerated Strategy—the three-pillar framework unveiled when the company became "New Fortive" in July 2025 following its portfolio restructuring.

Results through Q4 2025:

| Metric | Q4 2025 | Full Year 2025 |

|---|---|---|

| Core Revenue Growth | 3.3% | 1.7% |

| Adjusted EBITDA Margin | 30% | 31.9% |

| Adjusted EPS | — | $2.71 (beat high end of guidance) |

| Share Repurchases (H2) | $265M | $1.3B |

"We're pleased to see the momentum in our first two quarters," Soroye said. "Our top 250 leaders were together last week, and the level of excitement and energy and alignment around the strategy is just incredible."

The CEO emphasized what he called a "say-do ratio" commitment: "We really want to make sure whatever we say we're gonna do, we deliver it or we do better."

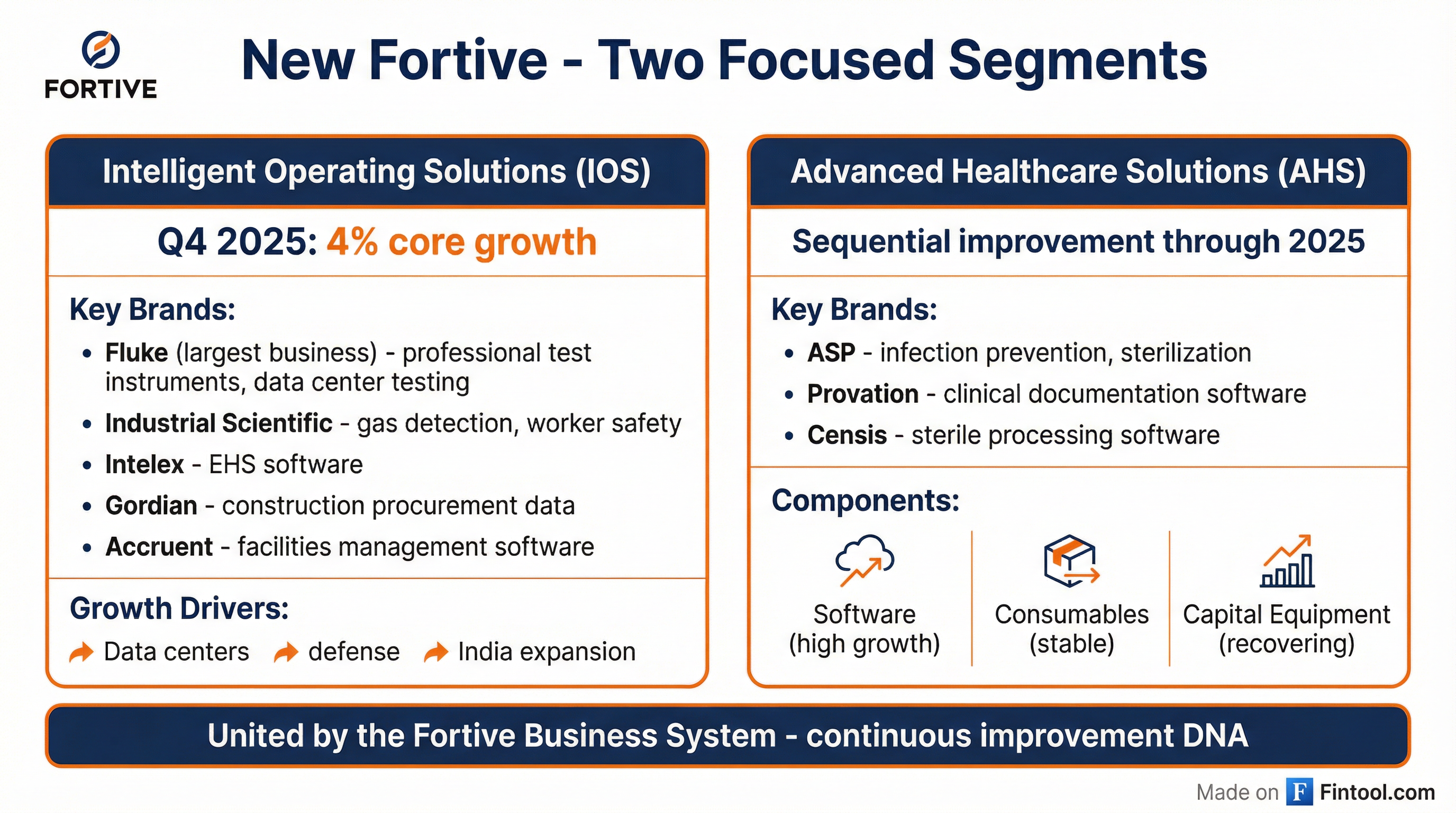

Segment Deep Dive: IOS Leads, AHS Stabilizing

Fortive's two segments showed diverging dynamics, with Intelligent Operating Solutions (IOS) accelerating while Advanced Healthcare Solutions (AHS) continued its recovery from capital spending headwinds.

Intelligent Operating Solutions (IOS)

Q4 2025 performance: 4% core growth, outperforming expectations

Fluke (largest business):

- Strong data center demand driving new product wins

- CertiFiber Max launched for high-density fiber testing with "fastest throughput in the industry"

- 15% of Fluke revenue now recurring (subscriptions, software, services)

Point-of-sale trends by region:

- North America: "Stayed really strong, as it was for all of 2025, and it's continued." Data center component increasing.

- EMEA: "Sequential improvement in Q4... not enough to call it a trend" but customers "getting a little bit less tentative"

- India: Double-digit growth across both segments in Q4

- China: "Steady" through H2 2025 and into 2026

Advanced Healthcare Solutions (AHS)

Structure breakdown:

- Software (Provation, Censis): "Highest customer loyalty, highest value" — AI use cases being deployed, strong growth

- Consumables & Services: "Very stable because it's really the flow of procedural volume"

- Capital Equipment: "Q2 2025 was kind of the tightest quarter... increasingly gotten better every quarter since then"

Data Center Tailwind: Beyond the Build-Out

Soroye offered a differentiated take on Fortive's data center opportunity, arguing that the company is positioned for the longer-duration operations and maintenance cycle rather than just the initial build-out:

"There's a lot of focus on the initial build-out stage of industrial capacity, including Data Center... But the more exciting part of this, from our point of view, is really the lifetime of operations and maintenance spend that needs to follow this initial build-out... Someone's got to worry about, 'How do I actually get the uptime and returns and performance from all of this capacity?' There's not enough technicians to manage them. There's not enough innovation in the professional instrumentation to drive them. That's where we really focus."

The company's newest product, CertiFiber Max, exemplifies this positioning—enabling faster certification of high-density fiber networks with sub-second testing throughput for hyperscaler data centers.

Capital Allocation: Buybacks Over Big M&A

CFO Mark Åkerström reinforced that Fortive will not pursue transformational M&A, instead focusing on bolt-on deals that meet "rigorous strategic and financial criteria."

Capital deployment priorities:

- Invest in organic growth

- Bolt-on M&A where risk-adjusted returns exceed alternatives

- Return capital through share repurchases

- Maintain modest growing dividend

"Transformational deals will continue to be off the table," Åkerström stated, while noting the company has "rebuilt the funnels" for M&A and closed two small transactions in H2 2025.

Free cash flow generation: The company generates approximately $1 billion annually, which Åkerström noted "is gonna grow and compound over time" with execution.

2026 Outlook: Conservative Start

Fortive guided to 2-3% organic growth for 2026—deliberately below its 3-4% two-year framework—with adjusted EPS of $2.90-$3.00 representing ~9% year-over-year growth at the midpoint.

Forward Estimates (Consensus):

| Period | Revenue | EPS |

|---|---|---|

| Q1 2026 | $1.04B | $0.64 |

| Q2 2026 | $1.06B | $0.69 |

| Q3 2026 | $1.06B | $0.72 |

| Q4 2026 | $1.15B | $0.91 |

| FY 2026 | $4.32B | $2.96 |

| FY 2027 | $4.48B | $3.18 |

Values from S&P Global

Soroye explained the conservative setup: "2026 will be faster than 2025, and 2027 will be faster than 2026. That's exactly where we are."

Early 2026 read: "January came out really solid for us, and we continue to see the trend, and that makes us feel really good about our setup for the year."

What to Watch

Near-term catalysts:

- February 18: Barclays 43rd Annual Industrial Select Conference (follow-up presentation)

- Q1 2026 earnings: Tracking of say-do ratio on organic growth acceleration

- Short-cycle recovery: PMI expansion in January—first after 11 months of contraction

Key metrics to monitor:

- Fluke recurring revenue mix (currently 15%, trending higher)

- Software ARR growth across IOS and AHS segments

- Capital equipment order trends in AHS

- India regional growth sustainability