Earnings summaries and quarterly performance for FLUSHING FINANCIAL.

Executive leadership at FLUSHING FINANCIAL.

John Buran

President and Chief Executive Officer

Astrid Burrowes

Executive Vice President, Chief Accounting Officer

Douglas McClintock

Senior Executive Vice President and General Counsel

Francis Korzekwinski

Senior Executive Vice President and Chief of Real Estate Lending

Maria Grasso

Senior Executive Vice President, Chief Operating Officer and Corporate Secretary

Michael Bingold

Senior Executive Vice President, Chief Retail and Client Development Officer

Susan Cullen

Senior Executive Vice President, Treasurer and Chief Financial Officer

Theresa Kelly

Executive Vice President, Business Banking

Thomas Buonaiuto

Senior Executive Vice President, Chief of Staff and Deposit Channel Executive

Board of directors at FLUSHING FINANCIAL.

Alfred DelliBovi

Chairman of the Board

Caren Yoh

Director

Donna O’Brien

Director

Douglas Manditch

Director

James Bennett

Director

John McCabe

Director

Louis Grassi

Director

Michael Azarian

Director

Sam Han

Director

Steven D’Iorio

Director

Research analysts who have asked questions during FLUSHING FINANCIAL earnings calls.

Mark Fitzgibbon

Piper Sandler & Co.

6 questions for FFIC

David Konrad

Keefe, Bruyette & Woods (KBW)

3 questions for FFIC

Sharon Gee

D.A. Davidson & Co.

3 questions for FFIC

Stephen Moss

Raymond James Financial, Inc.

3 questions for FFIC

Thomas Reid

Raymond James

3 questions for FFIC

Christopher O'Connell

Keefe, Bruyette, & Woods, Inc.

2 questions for FFIC

Manuel Navas

D.A. Davidson & Co.

2 questions for FFIC

Recent press releases and 8-K filings for FFIC.

- Halper Sadeh LLC is investigating Flushing Financial Corp. (NASDAQ: FFIC) for potential violations of federal securities laws and/or breaches of fiduciary duties to shareholders.

- The investigation concerns FFIC's proposed sale to OceanFirst Financial Corp..

- Under the terms of the sale, Flushing shareholders are expected to receive 0.85 of a share of OceanFirst common stock for each share of Flushing common stock.

- The law firm may seek increased consideration, additional disclosures, or other relief and benefits on behalf of shareholders.

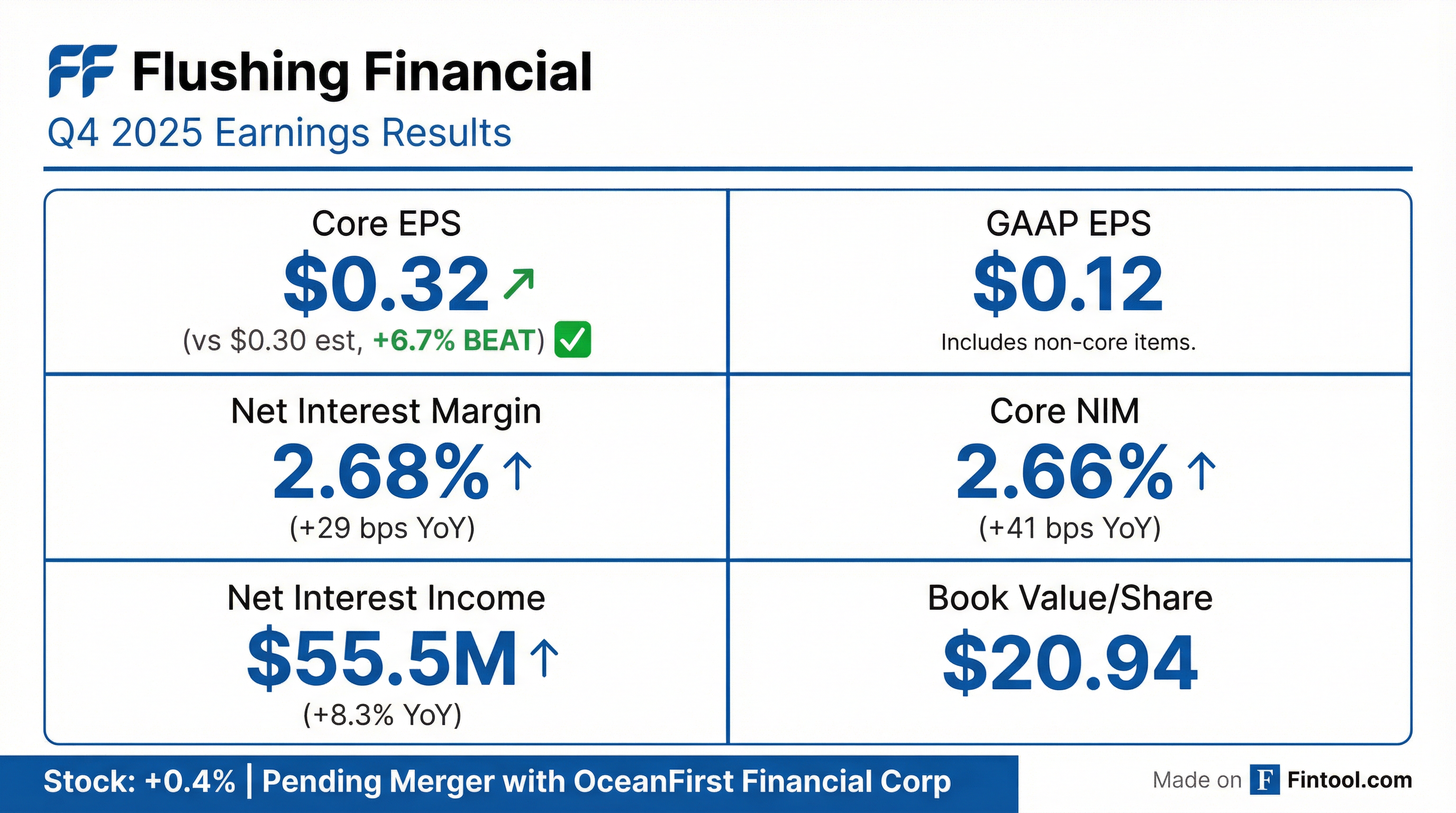

- Flushing Financial reported Q4 and full-year 2025 results, with GAAP EPS of $0.12 and Core EPS of $0.32, marking a significant turnaround from a ($1.64) GAAP EPS loss in the prior year.

- The company achieved net interest margin (NIM) expansion to 2.68% (Core NIM 2.66%), driven by a favorable deposit mix and lower funding costs.

- Despite NIM expansion, revenue of $58.81 million missed consensus by 4.87%, and the reported adjusted EPS of $0.32 was an -8.57% earnings surprise versus the Zacks Consensus of $0.35.

- Credit quality metrics showed Nonperforming Assets (NPAs) at 68 basis points of assets, a slight improvement, though criticized and classified loans rose to 126 basis points of gross loans.

- Management highlighted a $276 million loan pipeline and $3.9 billion of liquidity, anticipating benefits from the planned merger with OceanFirst Financial Corp..

- Flushing Financial Corporation reported 4Q25 GAAP EPS of $0.12 and Core EPS of $0.32, with the Net Interest Margin (NIM) expanding 4 basis points QoQ to 2.68% (GAAP) and 2.66% (Core).

- The company demonstrated strong balance sheet management, with average noninterest-bearing deposits increasing 12% year-over-year to 13% of total deposits, and the Tangible Common Equity ratio improving to 8.14% at December 31, 2025.

- CRE concentration declined to 465% at December 31, 2025, from 522% a year earlier, and the company maintains a loan pipeline of $276 million and liquidity of $3.9 billion.

- The company is undergoing a transformation due to the announced merger with OceanFirst Financial Corp., which also led to one-time charges in noninterest expenses and a canceled earnings conference call.

- Flushing Financial Corporation (the "Company") entered into an Agreement and Plan of Merger with OceanFirst Financial Corp. ("Parent") and Apollo Merger Sub Corp. on December 29, 2025, which will result in Parent being the surviving corporation.

- Following the corporate mergers, Flushing Bank, a wholly-owned subsidiary of the Company, will merge into OceanFirst Bank, National Association, a wholly-owned subsidiary of Parent.

- Concurrently with the merger closing, an investor will make an equity investment of $225,000,000 in Parent for shares of Parent Common Stock and Non-Voting Common Equivalent Stock.

- Effective April 1, 2026, all retiree health and welfare plans and obligations of the Company and Flushing Bank will terminate, with a one-time cash lump sum payment offered to eligible individuals.

- Flushing Financial Corp. (FFIC) and OceanFirst Financial Corp. (OCFC) have entered into a definitive all-stock merger agreement, valued at $579 million based on OCFC's closing stock price of $19.76 on December 26, 2025.

- Under the terms, Flushing stockholders will receive 0.85x of a share of OceanFirst common stock for each share of Flushing common stock.

- The combined company is expected to have approximately $23 billion in assets, $17 billion in total loans, and $18 billion in total deposits.

- The transaction includes a $225 million equity investment from Warburg Pincus and is projected to be 16% accretive to EPS and achieve a 13% Return on Average Tangible Common Equity (ROATCE) by 2027.

- The merger is anticipated to close in the second quarter of 2026, subject to regulatory and shareholder approvals.

- FFIC reported GAAP Net Interest Margin (NIM) of 2.64% and Core NIM of 2.62% in Q3 2025, both expanding by 10 basis points QoQ. Net Interest Income was $53.6 million in Q3 2025.

- Asset quality showed improvement, with Net charge-offs totaling 7 basis points in Q3 2025, down from 15 bps in Q2 2025. Non-performing assets (NPAs) to assets were 70 basis points at Q3 2025.

- Noninterest bearing deposits increased 7.2% QoQ and 5.7% YoY in Q3 2025. Total average deposits were $7,346 million.

- The company maintained strong capital and liquidity, with a Tangible Common Equity (TCE) ratio of 8.01% at September 30, 2025, up 101 basis points YoY. Undrawn lines and resources totaled $3.9 billion at quarter end.

- For the remainder of 2025, core noninterest expense is expected to increase 4.5%-5.5% from the 2024 base of $159.6 million, and the effective tax rate is projected to be 24.5%-26.5%.

- Flushing Financial Corporation (FFIC) reported strong Q3 2025 results, with GAAP earnings per share of $0.30 and core earnings per share of $0.35, marking a 55% year-over-year improvement in core earnings.

- The company achieved improved profitability, with GAAP net interest margin expanding to 2.64% and core net interest margin expanding to 2.62%, both increasing by 10 basis points quarter-over-quarter.

- Credit metrics remained robust, showing net charge-offs of 7 basis points and non-performing assets at 70 basis points of total assets as of Q3 2025.

- FFIC maintained a strong balance sheet, reporting a tangible common equity ratio of 8.01% and $3.9 billion in undrawn liquidity resources as of September 30, 2025.

- Future profitability is anticipated from loan repricing, with approximately $2 billion of loans scheduled to reprice at higher rates through 2027, expected to increase net interest income by $2 million in Q4 2025, $11 million in 2026, and $15 million in 2027.

- Flushing Financial Corporation reported GAAP diluted earnings per common share of $0.30 and Core EPS of $0.35 for the third quarter of 2025.

- The company's Net Interest Margin (NIM) expanded by 10 basis points quarter-over-quarter to 2.64% (GAAP) and 2.62% (Core) in Q3 2025.

- Average noninterest-bearing deposits increased 5.7% year-over-year and 2.1% quarter-over-quarter, comprising 12.2% of total average deposits in Q3 2025.

- The Tangible Common Equity to Tangible Assets ratio stood at 8.01% at September 30, 2025, marking a 101 basis-point improvement from a year ago.

- Credit quality metrics included Nonperforming Assets to assets at 0.70% and net charge-offs to average loans at 0.07% for Q3 2025, while the loan pipeline increased 91.0% quarter-over-quarter to $345.6 million.

- Both GAAP and Core Net Interest Margin (NIM) expanded by 10 basis points QoQ in Q3 2025, reaching 2.64% and 2.62% respectively.

- Flushing Financial Corp. maintained strong liquidity with $3.9 billion in undrawn lines and resources and reported a tangible common equity ratio of 8.01% as of September 30, 2025.

- Asset quality showed improvement with net charge-offs totaling 7 basis points in Q3 2025, down from 15 basis points in Q2 2025, and non-performing assets to assets at 70 basis points. The real estate loan portfolio has an average Loan-to-Value (LTV) of less than 35% and a weighted average Debt Coverage Ratio (DCR) of 1.7x for multifamily and investor commercial real estate loans.

- The company anticipates real estate loans to reprice approximately 147 basis points higher through 2027, with $175 million of loans scheduled to reprice upwards by 128 basis points in Q4 2025. Core noninterest expense for 2025 is projected to increase 4.5%-5.5% from the 2024 base of $159.6 million.

Quarterly earnings call transcripts for FLUSHING FINANCIAL.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more