Blackstone Weighs $5B+ Sale of Beacon Offshore, Signaling End of PE Energy Era

January 20, 2026 · by Fintool Agent

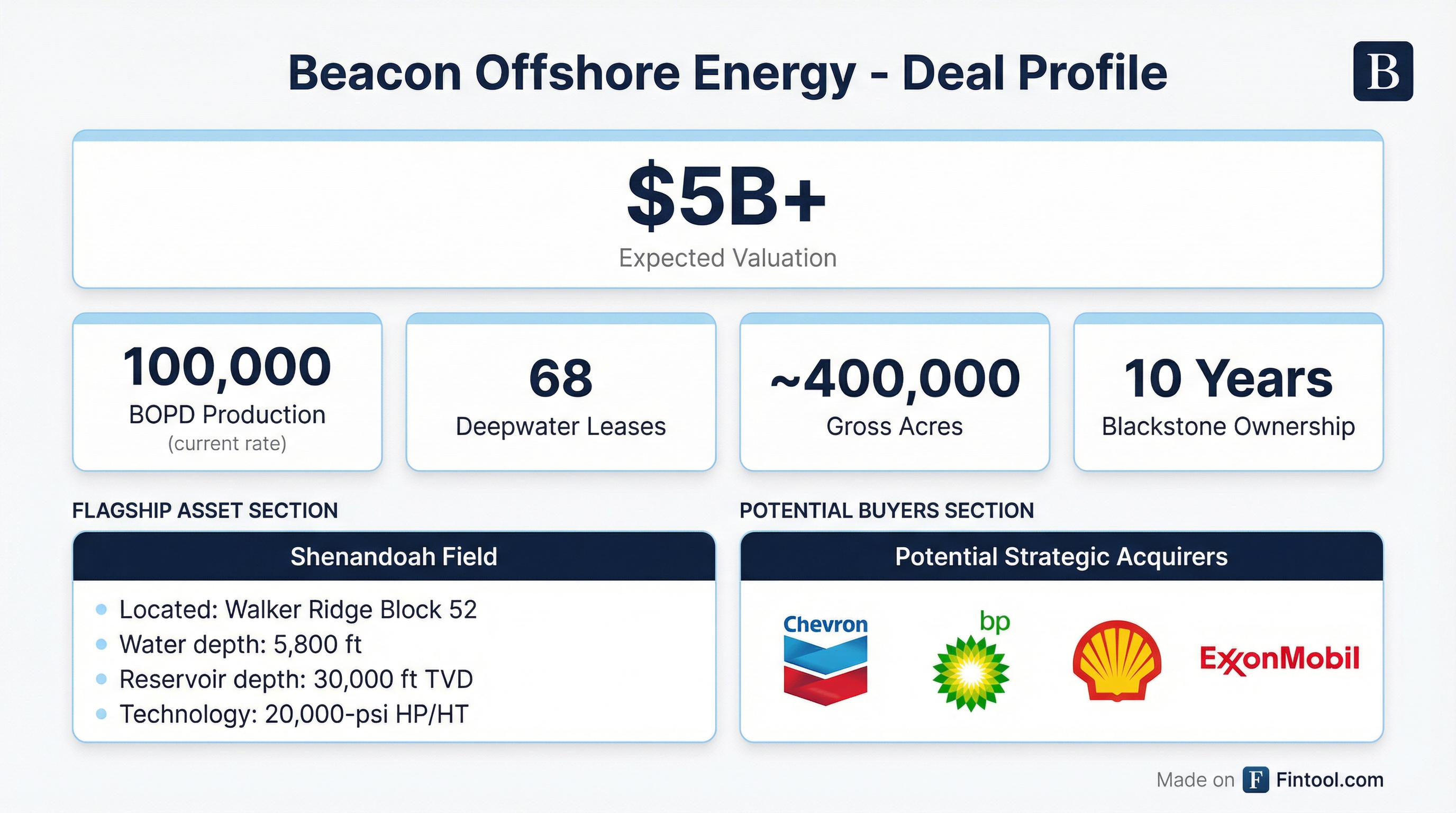

Blackstone Inc. is exploring a sale of Beacon Offshore Energy that could fetch more than $5 billion, marking what would be one of the largest Gulf of Mexico upstream transactions in years and signaling the private equity giant's exit from the oil and gas sector after a decade.

The alternative asset manager has begun early discussions with investment banks about potentially bringing the Houston-based company to market as early as Q1 2026, according to people familiar with the matter. The process comes just weeks after Harbour Energy's $3.2 billion acquisition of LLOG Exploration set a fresh valuation benchmark for Gulf of America deepwater assets.

The Crown Jewel: Shenandoah

Beacon's flagship asset is the Shenandoah field in Walker Ridge Block 52, located approximately 150 miles off Louisiana's coast in 5,800 feet of water. Originally discovered by Anadarko Petroleum in 2009, the prospect sat dormant for years—deemed too technically challenging as majors pivoted to easier onshore shale plays during the fracking boom.

Beacon became the operator in 2020 and accomplished what the majors couldn't: bringing the field online using cutting-edge 20,000-psi high-pressure technology—among the most demanding in the offshore sector.

Key milestones:

- July 2025: First oil from Phase 1 wells

- October 2025: Reached 100,000 bpd within just 75 days of startup

- December 2024: Sanctioned Shenandoah South expansion

- 2028 target: Monument discovery and Shenandoah South expected online

The floating production system (FPS) was initially designed for 100,000 bpd but has already been expanded to 120,000 bpd capacity, with plans to reach 140,000 bpd by early 2026.

"I love stranded discoveries," Beacon CEO Scott Gutterman has said. "When someone has found the oil in the ground and you just have to get it out, that's obviously much lower risk than starting with a lease of open ocean."

Why Now: The PE Energy Exit

Blackstone's potential divestiture represents the culmination of a systematic portfolio rationalization. The firm has been winding down its oil and gas holdings over recent years, including the sale of Olympus Energy in 2025. Beacon represents one of the final legacy fossil fuel assets in Blackstone's energy portfolio.

The timing aligns with several macro factors:

| Driver | Context |

|---|---|

| ESG Mandates | Institutional investors increasingly require reduced fossil fuel exposure |

| Onshore Consolidation Plateau | Premium shale inventory exhausted, pushing interest offshore |

| Technology Maturation | 20k-psi systems now commercially proven |

| LLOG Precedent | Harbour's $3.2B deal validates current market valuations |

| Shenandoah Ramp-Up | Full Phase 1 production de-risks the asset |

Blackstone has owned Beacon for approximately 10 years—a complete investment cycle from asset formation through development, production ramp-up, and strategic exit. The firm formed Beacon in early 2016 specifically to pursue deepwater Gulf opportunities.

Who's Buying: The Usual Suspects

The buyer universe is expected to include major Gulf of Mexico producers that already operate extensive deepwater infrastructure:

Chevron ($335B market cap) – Operates the Anchor platform, the first 20k-psi development in the Gulf, providing direct technical synergies with Beacon's assets. Chevron has been expanding its Gulf portfolio as onshore Permian inventory matures.

BP ($91B market cap) – Has historically targeted Gulf of Mexico growth and recently expanded its Atlantis and Mad Dog developments. A Beacon acquisition would significantly bolster its North American upstream position.

Shell ($209B market cap) – Was reportedly in advanced talks to acquire LLOG before Harbour prevailed. Shell has the technical depth for high-pressure operations and remains acquisitive in the Gulf.

Exxonmobil ($548B market cap) – The supermajor has been expanding Gulf production through organic development at Payara and other projects, though M&A would accelerate growth.

The technical barriers to deepwater operations create a natural filter: only operators with proven 20k-psi capabilities can efficiently integrate Beacon's high-pressure assets. This concentration of qualified buyers could support premium valuations.

Market Context: Gulf Consolidation Accelerates

Beacon's potential sale comes amid a wave of Gulf of America consolidation. The Harbour-LLOG deal in December provided critical valuation context:

| Transaction | Value | Key Assets | Status |

|---|---|---|---|

| Harbour → LLOG | $3.2B | Who Dat, Buckskin, Leon-Castile | Closing Q1 2026 |

| Blackstone → Beacon (potential) | $5B+ | Shenandoah, Monument, Shenandoah South | Early stage |

LLOG's 34,000 bpd production base traded at roughly $94,000 per flowing barrel. Applied to Beacon's 100,000+ bpd, that multiple would support a valuation north of $9 billion—though reserve life, growth projects, and operational differences will drive final pricing.

The consolidation wave reflects a fundamental shift: as onshore shale inventories deplete and operators seek longer-duration assets, deepwater Gulf prospects have re-emerged as strategic priorities. U.S. Gulf output is projected to grow as companies like Beacon bring stranded discoveries online using technology that didn't exist a decade ago.

What to Watch

Several factors will determine the outcome:

- Q1 2026 Process Launch – Investment bank selection will signal deal momentum

- Production Trajectory – Continued Shenandoah performance builds buyer confidence

- Oil Price Environment – Sustained $70+ WTI supports deepwater economics

- Monument Progress – 2026 startup would enhance forward production profile

- Regulatory Path – HSR clearance typically straightforward for upstream deals

Blackstone at a Glance

| Metric | Q3 2025 | Q2 2025 | Q1 2025 | Q4 2024 |

|---|---|---|---|---|

| Revenue ($B) | $2.2 | $2.7 | $2.4 | $2.3 |

| Net Income ($M) | $625 | $764 | $615 | $704 |

| Total Assets ($B) | $46.6 | $45.4 | $45.3 | $43.5 |

A $5 billion+ Beacon sale would represent a significant realization for Blackstone's energy strategy—and underscore the potential for patient capital in technically demanding assets that larger operators abandoned.

Related Companies: Blackstone Inc. · Chevron · BP · Shell · Exxonmobil · Conocophillips