Earnings summaries and quarterly performance for AbbVie.

Executive leadership at AbbVie.

Robert A. Michael

Chief Executive Officer

Azita Saleki-Gerhardt

Executive Vice President, Chief Operations Officer

Jeffrey R. Stewart

Executive Vice President, Chief Commercial Officer

Perry C. Siatis

Executive Vice President, General Counsel and Secretary

Scott T. Reents

Executive Vice President, Chief Financial Officer

Board of directors at AbbVie.

Brett J. Hart

Director

Edward J. Rapp

Director

Frederick H. Waddell

Director

Jennifer L. Davis

Director

Melody B. Meyer

Director

Rebecca B. Roberts

Director

Robert J. Alpern

Director

Roxanne S. Austin

Lead Independent Director

Susan E. Quaggin

Director

Thomas C. Freyman

Director

Thomas J. Falk

Director

William H.L. Burnside

Director

Research analysts who have asked questions during AbbVie earnings calls.

Mohit Bansal

Wells Fargo & Company

8 questions for ABBV

Steve Scala

Cowen

8 questions for ABBV

Terence Flynn

Morgan Stanley

8 questions for ABBV

Vamil Divan

Guggenheim Securities

8 questions for ABBV

David Risinger

Leerink Partners

7 questions for ABBV

Christopher Schott

JPMorgan Chase & Co.

6 questions for ABBV

Asad Haider

Goldman Sachs

5 questions for ABBV

Luisa Hector

Berenberg

5 questions for ABBV

Carter L. Gould

Barclays

3 questions for ABBV

Courtney Breen

AllianceBernstein

3 questions for ABBV

David Amsellem

Piper Sandler Companies

3 questions for ABBV

Geoffrey Meacham

Citi

3 questions for ABBV

Trung Huynh

UBS Group AG

3 questions for ABBV

Chris Schott

JPMorgan Chase & Company

2 questions for ABBV

Chris Shibutani

Goldman Sachs Group, Inc.

2 questions for ABBV

Geoff Meacham

Citigroup Inc.

2 questions for ABBV

James Shin

Analyst

2 questions for ABBV

Mark Hoffman

BMO Capital Markets

2 questions for ABBV

Matthew Phipps

William Blair

2 questions for ABBV

Michael Yee

Jefferies

2 questions for ABBV

Simon Baker

Rothschild & Co Redburn

2 questions for ABBV

Timothy Anderson

BofA Securities

2 questions for ABBV

Alexandria Hammond

Wolfe Research

1 question for ABBV

Christopher Raymond

Piper Sandler

1 question for ABBV

David Aslam

Piper Sandler

1 question for ABBV

Evan Seigerman

BMO Capital Markets

1 question for ABBV

Gary Nachman

Raymond James

1 question for ABBV

Jon Win

UBS

1 question for ABBV

Tim Anderson

Bank of America

1 question for ABBV

Recent press releases and 8-K filings for ABBV.

- AbbVie reported risankizumab SC induction met both co-primary endpoints with 55% vs 29.6% clinical remission and 44% vs 14.3% endoscopic response at week 12 (p<0.0001 vs placebo).

- Among patients with clinical response at week 12, 67% achieved clinical remission and 57% achieved endoscopic response at week 24.

- The study enrolled 289 adult patients, predominantly treatment-refractory (65% had failed advanced therapies).

- The safety profile during induction was consistent with known data, with no new safety risks observed.

- On February 24, 2026, AbbVie entered into an underwriting agreement to issue and sell seven series of senior notes totaling $8.0 billion aggregate principal amount due between 2028 and 2066.

- Notes will be priced at or near par, including floating-rate notes due 2028 at 100.000%, 3.775% notes due 2028 at 99.966%, 4.125% notes due 2031 at 99.972%, 4.400% notes due 2033 at 99.861%, 4.750% notes due 2036 at 99.911%, 5.550% notes due 2056 at 99.736% and 5.650% notes due 2066 at 99.714%.

- The offering is expected to close on March 4, 2026, with net proceeds of approximately $7.95 billion.

- AbbVie will use proceeds to repay outstanding borrowings under its $4.0 billion 364-day delayed draw term loan (May 2026 maturity; $2.0 billion currently drawn) and for general corporate purposes, including debt repayment.

- Slate Medicines closed a $130 million Series A financing co-led by RA Capital Management, Forbion, and Foresite Capital.

- Lead program SLTE-1009, licensed from DartsBio, is an anti-PACAP monoclonal antibody designed for subcutaneous preventive migraine dosing, with Phase 1 trials expected mid-2026.

- Slate added Andrew Levin (RA Capital), Tim Lohoff (Forbion), and Cindy Xiong (Foresite) to its Board of Directors as part of the financing.

- The round includes backing from RA Capital, Forbion, Foresite, and an undisclosed biotech investor.

- FDA approval of Calquence plus venetoclax for first-line CLL/SLL, marking the first all-oral, fixed-duration BTK inhibitor–based regimen in the US.

- The 14-month all-oral fixed-duration regimen offers greater flexibility compared with continuous therapies.

- In Phase III AMPLIFY, the 3-year PFS rate was 77% vs 67% for chemoimmunotherapy (HR 0.65; 95% CI, 0.49–0.87; p=0.0038); median PFS was not reached.

- An estimated 18,500 adults received first-line treatment for CLL in the US in 2024, underscoring potential market impact.

- Developed in collaboration with Genentech, the regimen is approved in multiple jurisdictions and is under further global regulatory review.

- The U.S. FDA approved the combination of VENCLEXTA and acalabrutinib as the first all-oral, fixed-duration regimen for previously untreated adult CLL patients.

- Approval is based on the Phase 3 AMPLIFY trial, which showed a 35% reduction in risk of disease progression or death versus chemoimmunotherapy (HR 0.65; p=0.0038), with median progression-free survival not reached versus 47.6 months.

- The regimen is administered over 14 fixed 28-day cycles, offering potential treatment-free intervals and expanding first-line CLL options.

- Safety findings were consistent with known profiles; tumor lysis syndrome incidence was 0.3%, and serious adverse events included COVID-19 (9%) and second primary malignancies (2.7%).

- AbbVie’s bispecific IL-1α/IL-1β inhibitor lutikizumab and RINVOQ in hidradenitis suppurativa are advancing in phase II, with both bio-experienced and biologic-naive cohorts enrolled and double-blind week 16 data expected by year-end.

- The company favors dual IL-1α/β targeting for potential clinical differentiation over IL-1β-only (O09) or OX40-TNF bispecific approaches, citing synergy in blocking key inflammatory pathways and immunogenicity concerns with anti-TNF bispecifics.

- In inflammatory bowel disease, AbbVie is testing combinations of SKYRIZI with a more potent α4β7 antagonist (382) and TL1A blocker (701), while subcutaneous SKYRIZI data and proof-of-concept for a novel TREM1 inhibitor are due later this year.

- A next-generation oral IL-23 program (via Nimble deal) aims to improve potency and extend half-life to match biologic-level efficacy and adherence.

- Early immunology pipeline includes a CD19 ADC (ABBV-319) with steroid payload for rapid B-cell depletion and durable remission, plus a non-payload antibody (ABBV-519) as a potential maintenance therapy.

- AbbVie's bispecific lutikizumab (IL-1α/β) and RINVOQ in hidradenitis suppurativa showed strong Phase II efficacy in TNF-experienced and biologic-naive cohorts; double-blind Week 16 data expected by year-end.

- In IBD, AbbVie is advancing SKYRIZI combination approaches: an α4β7 antagonist plus lutikizumab readout this year and TL1A-SKYRIZI studies starting later this year.

- The TREM1 program (myeloid receptor inhibitor) targets early proof-of-concept data late 2026/early 2027, aiming to improve deep remission in IBD with limited competition in the space.

- AbbVie’s next-gen oral IL-23 asset (via Nimble deal) is designed for higher potency and extended half-life to match biologic efficacy and support adherence.

- A novel 319 ADC targeting CD19 with a steroid payload is being developed for B-cell–driven autoimmunity (e.g., SLE, Sjögren’s), showing deep, durable depletion without systemic steroid effects.

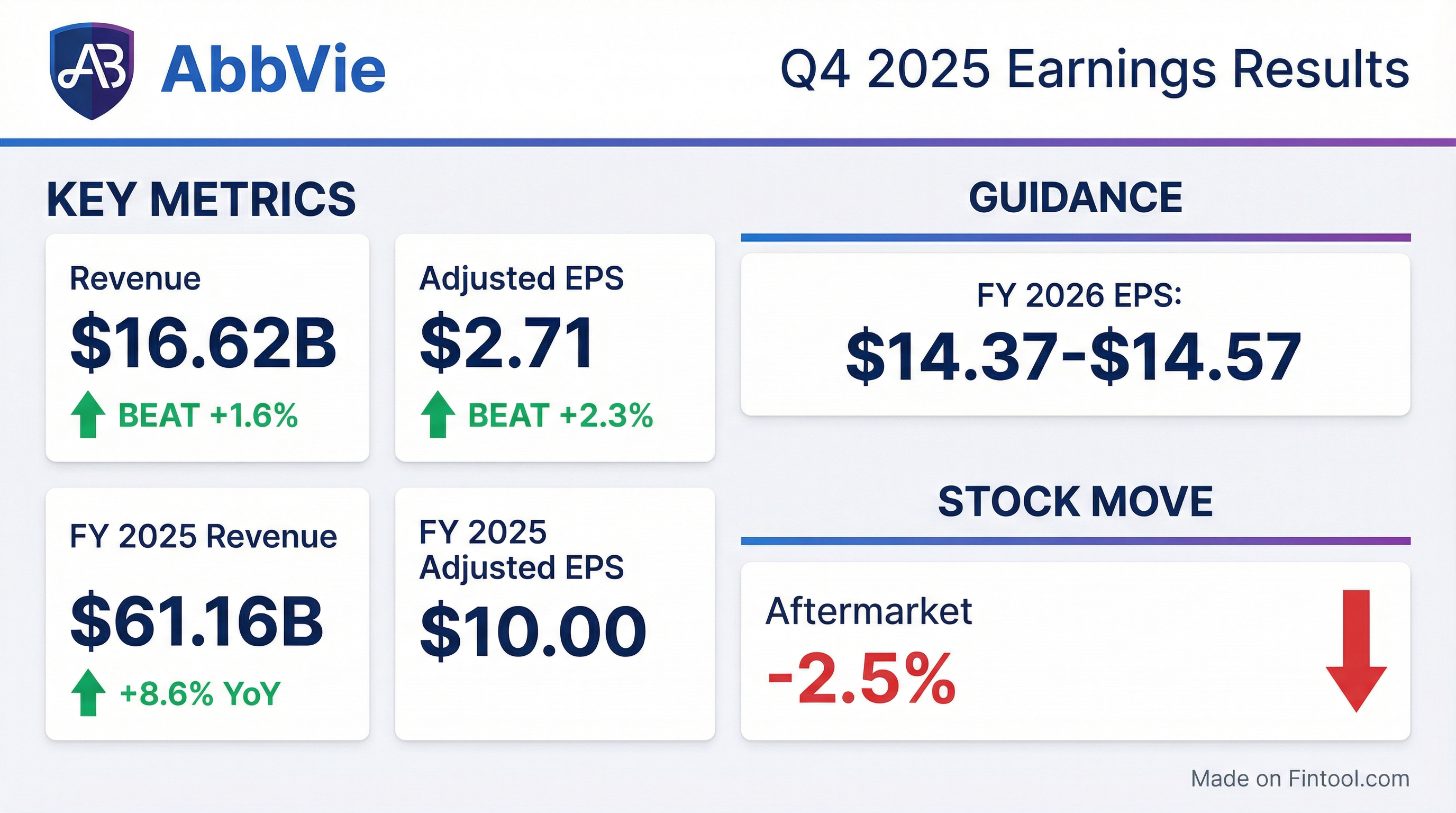

- AbbVie delivered full-year adjusted EPS of $10, beating its guidance midpoint by $0.54 (excluding IPR&D), and achieved record net revenues of $61.2 billion, up 8.6% and $2 billion above guidance despite Humira erosion.

- In Q4 2025, AbbVie reported total net revenues of $16.6 billion, up 10% YoY, and adjusted EPS of $2.71, $0.08 above guidance; the ex-Humira growth platform rose 14.5%, with an adjusted gross margin of 83.6%.

- For 2026, the company forecasts net revenues of ~$67 billion (+9.5%), adjusted EPS of $14.37–14.57, and expects immunology sales of $34.5 billion including Skyrizi at $21.5 billion and Rinvoq at $10.1 billion.

- Immunology performance in Q4 included $8.6 billion in total revenues, with Skyrizi at $5 billion (+31.9%) and Rinvoq at $2.4 billion (+28.6%).

- AbbVie delivered FY 2025 adjusted EPS of $10 and net revenues of $61.2 billion, up 8.6% yoy despite $16 billion of Humira erosion.

- In Q4 2025, AbbVie achieved adjusted EPS of $2.71 and net revenues of $16.6 billion (+10% yoy; ex-Humira platform +14.5%).

- For 2026, AbbVie guides net revenues of ~$67 billion (+9.5% yoy) and adjusted EPS of $14.37–$14.57.

- Immunology franchises delivered Q4 revenues of $8.6 billion, with Skyrizi at $5 billion (+31.9%) and Rinvoq at $2.4 billion (+28.6%); full-year combined revenue reached $25.9 billion (+ > $8 billion yoy).

- AbbVie advanced its pipeline with new approvals (Rinvoq for GCA, Emrelis, Epkinly), funded 90 clinical programs, and invested > $5 billion in business development in 2025.

- Record Q4 net revenues of $16.6 billion and adjusted EPS of $2.71, driving full-year net revenues of $61.2 billion and adjusted EPS of $10.00.

- Skyrizi and Rinvoq combined delivered $25.9 billion in 2025, with Q4 sales of $5 billion and $2.4 billion respectively, while Humira sales declined 26.1% to $1.2 billion in the quarter.

- For 2026, AbbVie guides ~$67 billion in revenues (9.5% growth) and adjusted EPS of $14.37–$14.57, including $34.5 billion in immunology and $12.5 billion in neuroscience sales.

- Continued pipeline investment with $5 billion in business development in 2025 and a three-year US pricing agreement, alongside projected $18.5 billion free cash flow for 2026 to support dividends and BD.

Fintool News

In-depth analysis and coverage of AbbVie.

AbbVie Doubles Down on U.S. Manufacturing with $380 Million API Investment

AbbVie Signs $100 Billion Deal With Trump, Clearing Path for Humira on TrumpRx

AbbVie Pays $650M to Join PD-1/VEGF Bispecific Race in JPM's First Big Deal

AbbVie Nears $20B+ Deal for Revolution Medicines, Capping Historic RAS Rally

Quarterly earnings call transcripts for AbbVie.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more