Earnings summaries and quarterly performance for MONRO.

Executive leadership at MONRO.

Peter Fitzsimmons

President and Chief Executive Officer

Brian D’Ambrosia

Executive Vice President — Finance, Chief Financial Officer, Treasurer and Assistant Secretary

Cindy Donovan

Senior Vice President — Chief Information Officer

Maureen Mulholland

Executive Vice President — Chief Legal Officer and Secretary

Nicholas Hawryschuk

Senior Vice President — Operations

Board of directors at MONRO.

Research analysts who have asked questions during MONRO earnings calls.

Bret Jordan

Jefferies

6 questions for MNRO

David Lantz

Wells Fargo & Company

6 questions for MNRO

Brian Nagel

Oppenheimer & Co. Inc.

5 questions for MNRO

Thomas Wendler

Stephens Inc.

4 questions for MNRO

Tom Wendler

Stephens Inc.

2 questions for MNRO

John Healy

Northcoast Research

1 question for MNRO

Seth Basham

Wedbush Securities

1 question for MNRO

Recent press releases and 8-K filings for MNRO.

- Monro has achieved four consecutive quarters of comparable store sales growth and its first quarter of two-year stack growth, attributing this success to internal initiatives.

- The company completed the closure of 145 underperforming stores in Q1, generating over $20 million in divestiture proceeds, and maintains a strong balance sheet with $45 million in bank debt (0.5x-0.4x bank debt to EBITDA leverage) to support future M&A.

- Strategic initiatives driving performance include enhanced digital marketing efforts, the implementation of a machine learning pricing tool for tires, and improved store operations via the ConfiDrive Courtesy Inspection system, which now averages around six photos per inspection.

- The auto aftermarket benefits from durable long-term trends, such as an aging vehicle fleet (average age over 12-13 years) and increasing vehicle complexity, favoring the "do-it-for-me" segment.

- Monro observes a K-shaped consumer recovery and notes that significant demand destruction from gasoline prices typically requires levels of $5 per gallon.

- Monro, operating approximately 1,100 locations with 50% of its business in tires and tire services, is executing a platform stabilization strategy.

- The company is reinvesting $7 million in G&A reductions from store closures into digital marketing, increasing acquisition marketing spend by $6 million in Q3, and has scaled these efforts across over 900 stores.

- Strategic initiatives include leveraging a machine learning tool for tire pricing optimization, concentrating volume with fewer suppliers, and integrating artificial intelligence into call center operations and internal store management tools.

- Monro maintains a strong balance sheet with $45 million in bank debt and 0.5x to 0.4x bank debt to EBITDA leverage, providing "dry powder" for potential future unit growth and acquisitions.

- Monro completed the closure of 145 locations in Q1, with 82 stores fully divested and generating over $20 million in proceeds. This strategic move allowed the company to focus on growth initiatives and fund marketing efforts.

- The company has achieved four consecutive quarters of comparable store sales growth and maintains a strong balance sheet with 0.5x to 0.4x bank debt to EBITDA leverage, providing significant capital for future unit growth and M&A opportunities in new markets like Texas, Arizona, and Colorado.

- Monro is reinvesting savings from store closures into enhanced digital marketing, with Q3 marketing spend increasing by $6 million, largely offset by a $7 million reduction in G&A. The company is also leveraging machine learning for pricing optimization and artificial intelligence for call center operations and field teammate reporting to improve efficiency and customer experience.

- Despite a soft tire market since January, Monro believes it is taking market share in the tire category, though deferred maintenance is most pronounced in tires due to their higher price point.

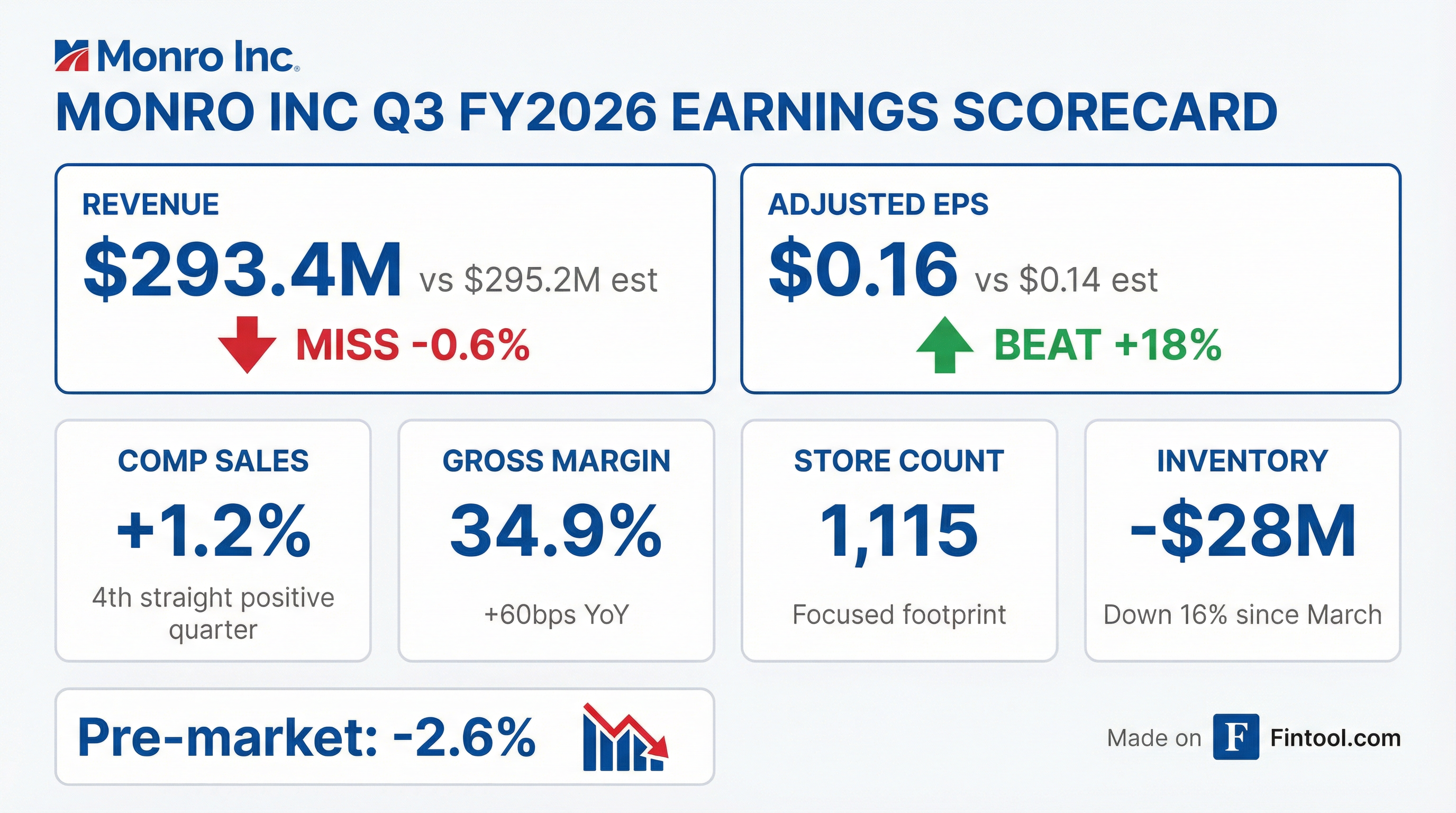

- Monro reported Q3 Fiscal 2026 sales of $293.4 million and adjusted diluted EPS of $0.16.

- The company achieved 1.2% comparable store sales growth in Q3 Fiscal 2026, marking its fourth consecutive quarter of positive comparable sales, and expanded its gross margin by 60 basis points year-over-year to 34.9%.

- Monro is executing a store optimization plan, having closed 145 underperforming stores and generated $22.8 million in cumulative proceeds from exiting leases and selling owned locations year-to-date in Fiscal 2026. This plan is expected to reduce total sales by approximately $45 million in Fiscal 2026.

- For Fiscal 2026, the company expects to deliver year-over-year comparable store sales growth, maintain gross margin consistent with Fiscal 2025, and anticipates CAPEX spend between $25 million and $35 million.

- As of December 2025, Monro reported ~$48 million in operating cash flow year-to-date Fiscal 2026, with ~$40 million in net bank debt and ~$425 million availability under its credit facility.

- Monro Inc. reported Q3 Fiscal 2026 sales of $293.4 million, a 4% decrease year-over-year, primarily due to the closure of 145 underperforming stores. However, comparable store sales from continuing locations increased by 1.2%, marking the fourth consecutive quarter of positive comps.

- The company achieved a 60 basis point expansion in gross margin year-over-year, reaching 34.9% in Q3 2026, driven by lower material and occupancy costs. Net income for the quarter was $11.1 million, with diluted earnings per share of $0.35.

- Monro generated $17.3 million in proceeds during Q3 2026 from exiting 32 leases and selling 20 owned locations as part of its real estate disposition plan, bringing the fiscal year-to-date total to $22.8 million.

- For the full fiscal year 2026, the company anticipates year-over-year comparable store sales growth and expects its gross margin to be consistent with fiscal 2025.

- Monro Inc. reported Q3 fiscal 2026 sales of $293.4 million, a 4% decrease primarily due to store closures, but achieved a 1.2% increase in comparable store sales from continuing locations.

- The company's gross margin expanded 60 basis points year-over-year to 34.9%, and diluted earnings per share (EPS) rose to $0.35 for the quarter.

- Monro generated $17.3 million in Q3 from the disposition of 32 leases and 20 owned locations, bringing fiscal year-to-date cumulative proceeds to $22.8 million from 57 leases and 25 locations.

- For fiscal 2026, the company continues to expect year-over-year comparable store sales growth and a full-year gross margin consistent with fiscal 2025.

- Monro reported Q3 Fiscal 2026 sales of $293.4 million and adjusted diluted EPS of $0.16.

- The company achieved 1.2% comparable store sales growth in Q3 FY26, marking its fourth consecutive quarter of positive comparable sales.

- Gross margin expanded 60 basis points year-over-year to 34.9% in Q3 FY26.

- Year-to-date fiscal 2026, Monro received $22.8 million in cumulative proceeds from exiting 57 leases and selling 25 owned locations, following the closure of 145 underperforming stores.

- For fiscal 2026, the company continues to expect year-over-year comparable store sales growth and anticipates the store optimization plan will reduce total sales by approximately $45 million.

- Monro Inc. reported Q3 Fiscal 2026 sales decreased 4% to $293.4 million, primarily due to the closure of 145 underperforming stores, but achieved a 1.2% increase in comparable store sales from continuing locations, marking its fourth consecutive quarter of positive comps.

- The company's gross margin expanded 60 basis points year-over-year to 34.9%, while net income rose to $11.1 million and diluted earnings per share reached $0.35.

- Monro continued its real estate disposition efforts, exiting 32 leases and selling 20 owned locations in Q3, generating $17.3 million in proceeds, contributing to fiscal year-to-date cumulative proceeds of $22.8 million.

- Inventory levels were reduced by over $7 million in Q3, resulting in an overall reduction of more than $28 million (16%) since the end of March.

- For the full fiscal year 2026, Monro anticipates year-over-year comparable store sales growth and a gross margin consistent with fiscal 2025.

- For the third quarter ended December 27, 2025, Monro, Inc. reported a 4.0% decrease in sales to $293.4 million, though comparable store sales increased 1.2%.

- Net income increased 143.1% to $11.1 million, and diluted earnings per share rose to $.35 for the third quarter of fiscal 2026.

- For the first nine months of fiscal 2026, sales decreased 1.9% to $883.3 million, while comparable store sales increased 2.6%.

- The company distributed a cash dividend of $.28 per share for the third quarter of fiscal 2026.

- Monro, Inc. is not providing fiscal 2026 financial guidance at this time.

- Monro, Inc. reported a 4.0% decrease in sales to $293.4 million for the third quarter of fiscal 2026, primarily due to the closure of 145 underperforming stores, partially offset by a 1.2% increase in comparable store sales.

- Diluted earnings per share for the third quarter of fiscal 2026 was $.35, while adjusted diluted earnings per share was $.16.

- Gross margin expanded 60 basis points year-over-year to 34.9% in the third quarter of fiscal 2026, mainly due to lower material and occupancy costs.

- The company distributed a cash dividend of $.28 per share for the third quarter of fiscal 2026.

Quarterly earnings call transcripts for MONRO.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more