Earnings summaries and quarterly performance for Celanese.

Executive leadership at Celanese.

Scott Richardson

Chief Executive Officer and President

Ashley Duffie

Senior Vice President, General Counsel and Corporate Secretary

Chuck Kyrish

Senior Vice President and Chief Financial Officer

Mark Murray

Senior Vice President, Acetyls

Todd Elliott

Senior Vice President, Engineered Materials

Board of directors at Celanese.

Bruce Chinn

Director

Christopher Kuehn

Director

David Hoffmeister

Director

Deborah Kissire

Director

Edward Galante

Independent Chair of the Board

Ganesh Moorthy

Director

Jay Ihlenfeld

Director

Kathryn Hill

Director

Kim Rucker

Director

Michael Koenig

Director

Scott Sutton

Director

Timothy Go

Director

Research analysts who have asked questions during Celanese earnings calls.

Aleksey Yefremov

KeyBanc Capital Markets

10 questions for CE

Ghansham Panjabi

Robert W. Baird & Co.

10 questions for CE

Hassan Ahmed

Alembic Global Advisors

10 questions for CE

Jeffrey Zekauskas

JPMorgan Chase & Co.

10 questions for CE

John Ezekiel Roberts

Mizuho Securities

10 questions for CE

Patrick Cunningham

Citigroup

10 questions for CE

Salvator Tiano

Bank of America

10 questions for CE

David Begleiter

Deutsche Bank

9 questions for CE

Arun Viswanathan

RBC Capital Markets

8 questions for CE

Michael Sison

Wells Fargo

8 questions for CE

Vincent Andrews

Morgan Stanley

8 questions for CE

Frank Mitsch

Fermium Research

7 questions for CE

Kevin McCarthy

Vertical Research Partners

7 questions for CE

Joshua Spector

UBS

5 questions for CE

Matthew Blair

Tudor, Pickering, Holt & Co.

5 questions for CE

Josh Spector

UBS Group

4 questions for CE

Aziza Gazieva

Fermium Research

2 questions for CE

Laurence Alexander

Jefferies

2 questions for CE

Mike Sison

Wells Fargo

2 questions for CE

Turner Hendricks

Morgan Stanley

2 questions for CE

Adam

RBC Capital Markets

1 question for CE

Adam Samuelson

The Goldman Sachs Group, Inc.

1 question for CE

Aziza Osinaike

Fermium Research

1 question for CE

James Cannon

UBS Securities

1 question for CE

John McNulty

BMO Capital Markets

1 question for CE

Kevin Estecon

Jefferies

1 question for CE

Kevin Estok

Jefferies

1 question for CE

Michael Leithead

Barclays

1 question for CE

Recent press releases and 8-K filings for CE.

- Free cash flow targeted at $650–$750 million for 2026, with management prioritizing cash generation amid demand uncertainty.

- $1 billion divestiture plan by end-2027 (≈50% completed); another non-core asset sale expected in 2026, focusing on joint ventures.

- Lanaken plant closure to deliver $20–$25 million annual cost savings, including $5–$10 million benefit in 2026.

- Expect $1–$2 EPS uplift in 2026 through Engineered Materials volume growth and Acetyl Chain optimizations; Q2 earnings likely flat to Q1 and second-half weighted.

- Electronics markets are a bright spot, while automotive is mixed (softness in China EV credits); moderate seasonal recovery in coatings and auto expected into Q1.

- Focus on cash: 2026 free cash flow is targeted at $650 million–$750 million, driven by $100 million of additional inventory reductions, $50 million lower interest expense, $50 million–$60 million lower cash taxes and reduced cost-program outlays.

- Divestiture plan: targeting $1 billion of asset sales by end-2027 (approximately half secured), with another transaction expected in 2026 to support debt reduction.

- Engineered Materials: saw sequential volume/mix improvements led by electronics and stable U.S./European auto; growth levers include AI/data-center build-outs, automotive hybrids and medical applications.

- Acetyl Chain challenges: 2025 Adjusted EBIT declined by ~$400 million due to volume and price weakness; the Lanaken plant closure will yield $20 million–$25 million in annual cost savings (with $5 million–$10 million in 2026), and Chinese margins have stabilized with mid-year normalization expected.

- EPS outlook: management targets a $1–$2 per-share uplift in 2026 versus 2025, noting that a 1% volume gain equates to $15 million–$20 million in Acetyl Chain or $20 million–$25 million in Engineered Materials annually, and anticipates H2 weighting due to turnarounds.

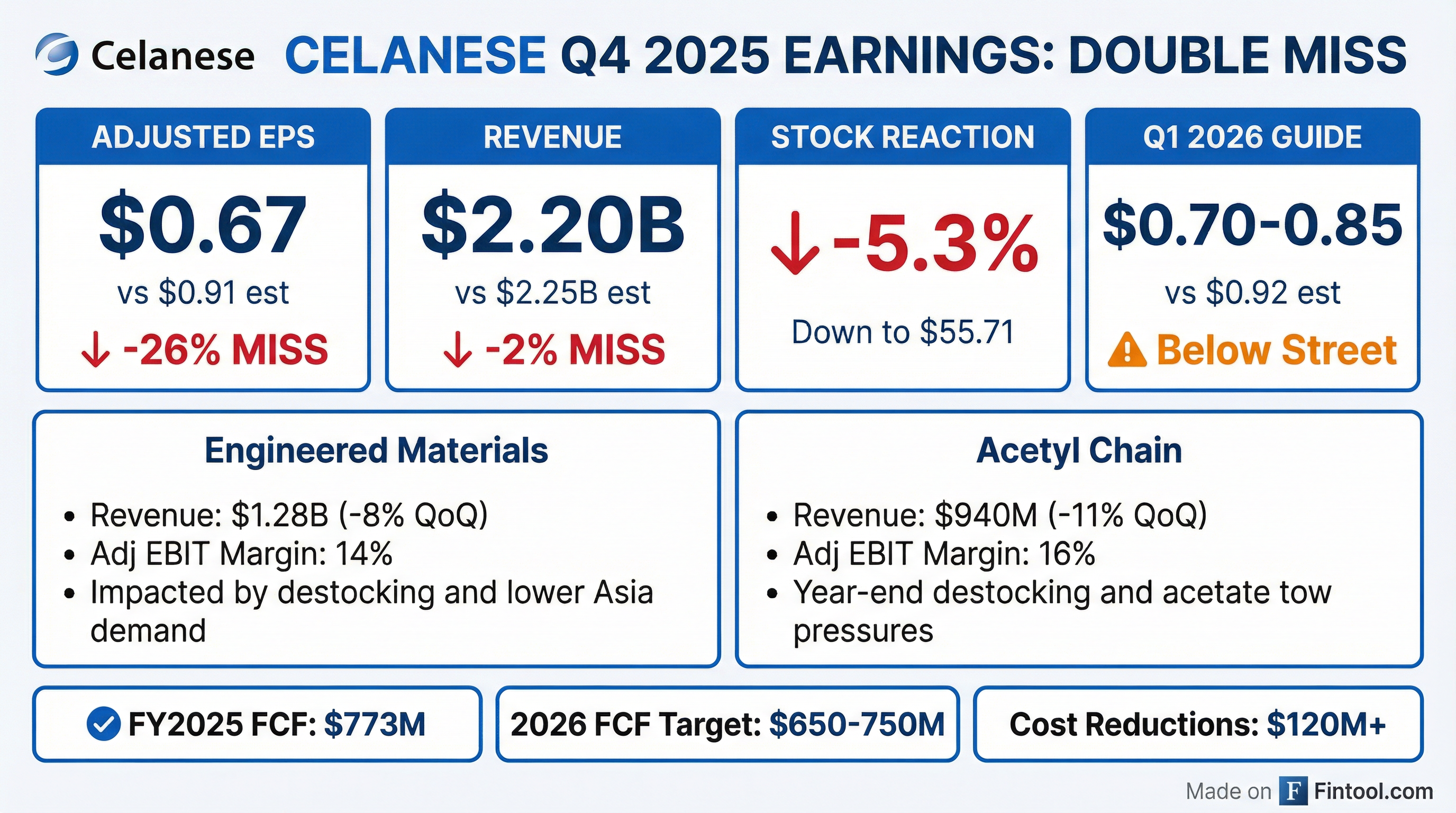

- Q4 2025 results: adjusted EPS of $0.67, free cash flow of $160 M, Engineered Materials EBIT of $183 M and Acetyl Chain EBIT of $146 M.

- FY2025 free cash flow of $773 M, surpassing targets; FY2026 FCF guidance of $650–$750 M.

- Q1 2026 outlook: adjusted EPS of $0.70–$0.85, Adjusted EBIT guidance of $210–$230 M (Engineered Materials: $110–$125 M).

- Deleveraging: completed Micromax divestiture and debt refinancing, generating ~$2.6 B (2023–2025) and reducing net debt by ~$2.0 B.

- Cost savings: achieved >$120 M in 2025; targeting $50–$70 M incremental savings in 2026.

- Management targets $650 million–$750 million free cash flow for 2026 and plans $1 billion of divestitures by the end of 2027 to reduce leverage, with confidence in achieving this even under low‐demand scenarios.

- Closure of the Lanaken acetate tow plant will deliver $20 million–$25 million in annual cost savings, with $5 million–$10 million realized in 2026.

- Demand in Engineered Materials is led by electronics, with automotive mixed—soft in China, stable in Europe, and a potential tailwind from ICE/hybrid focus in the U.S.—and a moderate seasonal uptick in coatings and U.S. EM volumes expected in Q1.

- Contract pricing is largely unchanged, spot volumes remain pressured by overcapacity, Western Hemisphere acetyl margins are more resilient, and Chinese acetyl spreads have stabilized at low levels after recent capacity-driven troughs.

- Celanese delivered Q4 2025 adjusted EPS of $0.67 and free cash flow of $160 million, driving FY 2025 adjusted EPS of $3.98 and free cash flow of $773 million, up over 50% year-over-year.

- Full-year operating EBITDA was $1.9 billion, with margins above 20% in both Engineered Materials and the Acetyl Chain.

- The company refinanced approximately $4 billion of debt, reducing 2026–27 maturities from $4.8 billion to $2.1 billion, and completed the Micromax® divestiture, generating $492 million in cash proceeds.

- For 2026, Celanese targets $650–$750 million of free cash flow and expects Q1 2026 adjusted EPS of $0.70–$0.85, with segment EBIT guidance of $210–$230 million for Engineered Materials and $110–$125 million for the Acetyl Chain.

- Full-year 2025 net sales of $9.5 billion, U.S. GAAP diluted loss per share of $10.44 and adjusted EPS of $3.98; operating EBITDA of $1.9 billion and free cash flow of $773 million

- Q4 2025 net sales of $2.2 billion, U.S. GAAP diluted EPS of $0.23 and adjusted EPS of $0.67; operating EBITDA of $435 million and free cash flow of $160 million

- Results affected by lower demand in automotive, paints, coatings and construction; achieved over $120 million in cost reductions and completed the Micromax divestiture

- Outlook for Q1 2026 adjusted EPS of $0.70–$0.85 and full-year 2026 free cash flow target of $650–$750 million

- FY 2025 U.S. GAAP EPS: $10.44 loss, adjusted EPS $3.98 on net sales of $9.5 billion (down ~7% yoy)

- Q4 2025: adjusted EPS $0.67, revenue $2.2 billion, operating profit $93 million (adjusted EBIT $251 million)

- Year-end leverage of 5.7×, supported by a $500 million Micromax divestiture to accelerate deleveraging

- FY 2025 operating cash flow $1.1 billion, free cash flow $773 million; Q1 2026 adjusted EPS guidance $0.70–$0.85, 2026 FCF target $650–$750 million

- Celanese is raising prices for acetic acid, Vinyl Acetate Monomer (VAM) and related derivatives in the Western Hemisphere, effective immediately or as contracts allow.

- Price hikes include $50/MT for acetic acid and esters, $60/MT for acetic anhydride, and $100/MT for VAM in the USA/Canada and Mexico/South America, with equivalent increases of €50–€100/MT in EMEA.

- Adjustments apply to both base products and their downstream derivatives, with customer-specific notifications for derivative pricing.

- Celanese completed the sale of its Micromax® business to Element Solutions Inc for $500 million in cash.

- Proceeds will be used to support the company’s deleverage efforts.

- CEO Scott Richardson said the transaction is value-accretive, strengthens the balance sheet and advances priorities of cash generation and deleveraging.

- Celanese is a Fortune 500 specialty materials and chemical company with over 11,000 employees and 2024 net sales of $10.3 billion.

- Global orthopedic biomaterials market projected to grow from USD 16.95 billion in 2025 to USD 24.86 billion by 2030 at a CAGR of 8.0%

- Growth driven by aging population, demand for patient-specific and bioactive implants, and shift toward minimally invasive procedures

- Metallic biomaterials held the largest share in 2024, led by load-bearing applications such as hip and knee arthroplasty and spinal instrumentation

- Asia Pacific is the fastest-growing region, supported by local manufacturing expansion and government initiatives to enhance surgical capacity

- Celanese is positioned as the star performer, leveraging its medical-grade polymers for spinal, trauma, and joint-replacement applications

Quarterly earnings call transcripts for Celanese.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more