Earnings summaries and quarterly performance for W.W. GRAINGER.

Executive leadership at W.W. GRAINGER.

Board of directors at W.W. GRAINGER.

Beatriz Perez

Director

Christopher Klein

Director

Cindy Miller

Director

E. Scott Santi

Lead Independent Director

George Davis

Director

Katherine Jaspon

Director

Lucas Watson

Director

Neil Novich

Director

Rodney Adkins

Director

Steven White

Director

Susan Slavik Williams

Director

Research analysts who have asked questions during W.W. GRAINGER earnings calls.

David Manthey

Robert W. Baird & Co. Incorporated

7 questions for GWW

Ryan Merkel

William Blair & Company

7 questions for GWW

Christopher Glynn

Oppenheimer & Co. Inc.

6 questions for GWW

Christopher Snyder

Morgan Stanley

6 questions for GWW

Jacob Levinson

Melius Research

6 questions for GWW

Patrick Baumann

JPMorgan Chase & Co.

5 questions for GWW

Sabrina Abrams

Bank of America

5 questions for GWW

Deane Dray

RBC Capital Markets

4 questions for GWW

Tommy Moll

Stephens Inc.

4 questions for GWW

Christopher Dankert

Loop Capital Markets

3 questions for GWW

Kenneth Newman

KeyBanc Capital Markets

3 questions for GWW

Thomas Moll

Stephens Inc.

3 questions for GWW

Chris Dankert

Loop Capital

2 questions for GWW

Connor Lynagh

Bernstein

2 questions for GWW

Guy Hardwick

Freedom Capital Markets

2 questions for GWW

Stephen Volkmann

Jefferies

2 questions for GWW

Jake Levinson

Melius Research LLC

1 question for GWW

Katie Fleischer

KeyBanc Capital Markets

1 question for GWW

Ryan Cooke

William Blair & Company

1 question for GWW

Recent press releases and 8-K filings for GWW.

- Grainger operates two go-to-market models: High-Touch for large, complex customers (80% of revenue) and Endless Assortment (20%) via Zoro.com and Monotaro.com, both underpinned by AI/ML and a robust supply chain to drive share gains.

- 2026 guidance: revenue of $18.7–$19.1 billion, daily organic constant currency sales growth of 6.5–9%, operating margin expansion of 40–90 bps, and EPS of $42.25–44.75 (10% growth at midpoint).

- Strong capital allocation: pre-tax adjusted ROIC of 39% in 2025, 54 consecutive years of dividend increases, active share repurchases, and investments in technology and supply chain capacity.

- Investing in AI and data: proprietary product/customer information systems feeding five strategic growth engines, with Gen AI applications in pricing, customer service, and fulfillment to enhance productivity and customer experience.

- Grainger operates two complementary go-to-market models: High-Touch, which serves larger, complex customers and drives 80% of revenue, and Endless Assortment, serving small to mid-sized businesses online (Zoro.com and Monotaro.com) for the remaining 20% of revenue.

- For fiscal 2026, Grainger expects revenue of $18.7 – $19.1 billion, daily organic constant-currency sales growth of 6.5% – 9%, operating margin expansion of 40–90 bps, and EPS of $42.25 – $44.75 (10% growth at midpoint).

- The company is heavily investing in AI/ML capabilities—including proprietary models for product breadth, marketing ROI, pricing, and customer service—to drive revenue growth, efficiency gains, and enhanced customer experience across both segments.

- Grainger’s balanced capital allocation delivered a pre-tax adjusted ROIC above 39% in 2025, marking its 54th consecutive year of dividend increases alongside high-return share repurchases.

- High-Touch model (80% of sales) serves large, complex B2B customers, while Endless Assortment (20%) online platforms Zoro.com and Monotaro.com target smaller businesses.

- 2026 guidance: revenue of $18.7–$19.1 billion, daily organic constant currency sales growth of 6.5–9%, operating margin expansion of 40–90 bps, and EPS of $42.25–$44.75 (+10% at midpoint).

- Capital return strength: pre-tax adjusted ROIC over 39% in 2025, 54th consecutive year of dividend increases, and ongoing share repurchases.

- Strategic investments: leveraging proprietary data, AI/ML models, and supply chain automation to expand assortment, improve efficiency, and enhance customer service.

- Grainger delivered 4.5% reported sales growth (4.9% daily organic constant currency) to $17.9 billion in 2025, with 15% operating margin, $39.48 adjusted EPS, $2 billion operating cash flow, and $1.5 billion returned to shareholders.

- In Q4 2025, total daily sales grew 4.5% reported (4.6% organic), gross margin was 39.5%, operating margin declined 70 bps, and diluted EPS was $9.44. High-Touch Solutions sales rose 2.2% (42.3% gross margin; 15.8% operating margin), while Endless Assortment grew 14.3% (15.7% organic) with operating margin up 200 bps to 10.6%.

- For 2026, Grainger expects revenue of $18.7–$19.1 billion, daily organic constant currency growth of 6.5–9%, High-Touch Solutions growth of 5–7.5%, Endless Assortment growth of 12.5–15%, and total operating margin of 15.4–15.9%.

- Capital allocation plans include $2.1–$2.3 billion in operating cash flow, $550–$650 million in CapEx, ~$1 billion in share repurchases, and a high-single to low-double digit dividend increase.

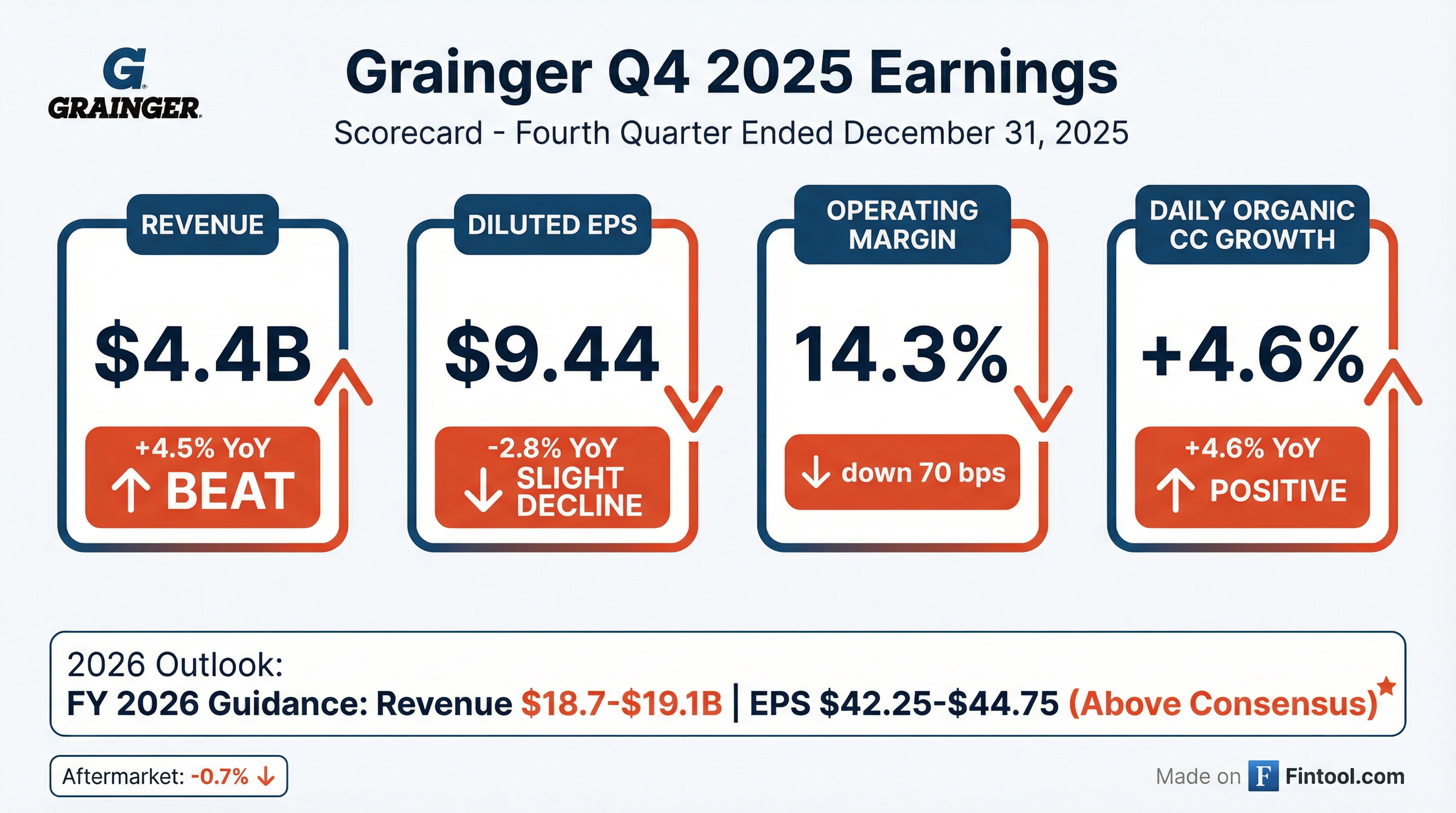

- Grainger reported Q4 2025 sales of $4.425 billion, a 4.5% increase year-over-year, with daily sales up to 69.1 (4.5% growth).

- Q4 operating margin declined to 14.3% (down 70 bps), gross profit margin was 39.5%, SG&A at 25.2% of sales, delivering diluted EPS of $9.44, down 2.8%.

- Full-year 2025 sales grew 4.5% (4.9% in daily, organic constant currency), operating margin held at 15.0%, ROIC at 39.1%, operating cash flow was $2.0 billion, returning $1.5 billion to shareholders.

- 2026 guidance includes net sales of $18.7–19.1 billion, daily organic constant currency growth of 6.5–9.0%, operating margin of 15.4–15.9%, and operating cash flow of $2.125–2.325 billion.

- For full year 2025, Grainger delivered 4.5% sales growth to $17.9 billion, 15% operating margin, $39.48 adjusted EPS, 39.1% ROIC, and generated $2 billion operating cash flow, returning $1.5 billion to shareholders.

- In Q4 2025, daily organic constant currency sales rose 4.6% (normalized to ~6.5%), with $9.44 diluted EPS; High-Touch Solutions grew 2.1% organic (42.3% gross margin) while Endless Assortment grew 15.7% organic with segment margin of 10.6%.

- 2026 guidance targets $18.7–$19.1 billion revenue (6.5–9.0% organic growth), 15.4–15.9% operating margin, and $42.25–$44.75 EPS, supported by $550–650 million CapEx and ~$1 billion of share repurchases.

- Continued strategic investments include net 85,000 SKU additions in merchandising, adding 110 new sellers, expanding KeepStock services, and advancing AI/ML capabilities across channels, alongside supply chain capacity expansions in the U.S. and Japan.

- Full-year 2025 sales reached $17.9 B, up 4.5% reported (4.9% daily organic constant currency); operating margin was 15%, EPS $39.48, and operating cash flow was $2 B, returning $1.5 B to shareholders.

- In Q4 2025, daily sales grew 4.5% (4.6% organic constant currency) and EPS was $9.44, down 2.8% year-over-year.

- High-Touch Solutions Q4 sales rose 2.1% organic constant currency with operating margin at 15.8% (down 120 bp), while Endless Assortment sales grew 15.7% organic constant currency and margin improved 200 bp to 10.6%.

- For 2026, Grainger forecasts revenue of $18.7 B–$19.1 B (6.5%–9% daily organic constant currency growth), operating margin of 15.4%–15.9%, and EPS of $42.25–$44.75.

- Delivered Q4 2025 sales of $4.4 billion, up 4.5% (4.6% daily, organic constant currency) and FY 2025 sales of $17.9 billion, up 4.5% (4.9% daily, organic constant currency)

- Reported Q4 diluted EPS of $9.44, down 2.8%; FY 2025 EPS of $35.40 (reported, down 8.6%) and $39.48 (adjusted, up 1.3%)

- Generated $2.0 billion in full-year operating cash flow and returned $1.5 billion to shareholders through dividends and share repurchases

- Issued 2026 guidance of $18.7–$19.1 billion in net sales, 6.5%–9.0% daily organic constant currency sales growth, $42.25–$44.75 diluted EPS, and $2.125–$2.325 billion in operating cash flow

- Net sales of $4.4 billion in Q4, up 4.5% (4.6% daily organic constant currency); full year sales of $17.9 billion, up 4.5% (4.9% daily organic constant currency).

- Operating margin of 14.3% in Q4, down 70 bps; diluted EPS of $9.44, down 2.8%. For FY, margin was 13.9% (15.0% adjusted) and EPS was $35.40 (adjusted $39.48).

- Generated $2.0 billion of operating cash flow and $1.3 billion of free cash flow in 2025; $1.5 billion returned to shareholders through dividends and share repurchases.

- 2026 guidance: net sales growth of 4.2%–6.7% (6.5%–9.0% daily organic constant currency), gross margin of 39.2%–39.5%, operating margin of 15.4%–15.9%, and EPS of $42.25–$44.75.

- Delivered $4.657 billion in sales, up 6.1% year-over-year, with diluted EPS of $10.21, up 3.4% versus Q3 2024.

- Generated operating cash flow of $597 million and returned $399 million to shareholders through dividends and share repurchases.

- High-Touch Solutions sales grew 3.4% to $3.635 billion, while Endless Assortment sales rose 18.2% to $935 million, with respective margin pressures and gains.

- Narrowed FY 2025 guidance to sales of $17.8 – 18.0 billion (+3.9% – 4.7%), gross margin of 38.9% – 39.1%, and adjusted EPS of $39.00 – 39.75.

- Tariff-related LIFO headwind of 0.8% – 0.9% on gross margin (~$140 – 160 million) expected to normalize by mid-2026, stabilizing run-rate at ~39%.

Quarterly earnings call transcripts for W.W. GRAINGER.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more