Earnings summaries and quarterly performance for CORNING INC /NY.

Executive leadership at CORNING INC /NY.

Wendell Weeks

Chairman, President and Chief Executive Officer

Edward Schlesinger

Executive Vice President and Chief Financial Officer

Hal Nelson

Executive Vice President and Chief Operating Officer

John Zhang

Executive Vice President and Chief Corporate Development Officer

Lewis Steverson

Vice Chairman, Executive Vice President and Chief Legal and Administrative Officer

Board of directors at CORNING INC /NY.

Ami Badani

Director

Daniel Huttenlocher

Director

Kevin Martin

Director

Leslie Brun

Director

Pamela Craig

Director

Robert Cummings Jr.

Director

Roger Ferguson Jr.

Director

Stephanie Burns

Lead Independent Director

Thomas French

Director

Research analysts who have asked questions during CORNING INC /NY earnings calls.

Asiya Merchant

Citigroup Global Markets Inc.

8 questions for GLW

John Ezekiel Roberts

Mizuho Securities

8 questions for GLW

Wamsi Mohan

Bank of America Merrill Lynch

8 questions for GLW

George Notter

Jefferies

7 questions for GLW

Steven Fox

Fox Research

6 questions for GLW

Mehdi Hosseini

Susquehanna Financial Group

4 questions for GLW

Meta Marshall

Morgan Stanley

4 questions for GLW

Samik Chatterjee

JPMorgan Chase & Co.

4 questions for GLW

Joshua Spector

UBS

3 questions for GLW

James Cannon

UBS Securities

2 questions for GLW

Joe Cardoso

JPMorgan Chase & Co.

2 questions for GLW

Josh Spector

UBS Group

2 questions for GLW

Matthew Niknam

Deutsche Bank

2 questions for GLW

Tim Long

Barclays

2 questions for GLW

Timothy Long

Barclays

2 questions for GLW

Martin Yang

Oppenheimer & Co. Inc.

1 question for GLW

Recent press releases and 8-K filings for GLW.

- Visa has reallocated R&D from core payments infrastructure to enriching the network’s edges, organizing 1,000+ dev squads into agile, client-focused teams that leverage generative AI to prototype concepts in days instead of months.

- Consumers are increasingly shopping across social commerce, gaming, and emerging agentic channels, yet Visa’s transaction volume growth metric remains “rock-solid,” reflecting stable user engagement even amid evolving behaviors.

- Over the past decade, average transaction size fell by 20% while transaction count tripled; Visa expects agentic commerce to further boost transaction density by automating and unbundling purchases via software agents.

- To support client-agent-server payment flows, Visa introduced the open Trusted Agent Protocol for agent identity and token provisioning, already backed by Cloudflare, Akamai, Mastercard, AmEx, and integrated into Stripe’s agentic commerce offerings.

- Visa’s stablecoin settlement run rate rose from $2.5 billion in August 2025 to $4.6 billion by Q1 FY26, with 130+ stablecoin-linked card programs across 40 countries and plans to expand its Bridge partnership to 100 countries by year-end.

- CFO Ed Schlesinger highlighted the success of the Springboard plan, noting 40% sales growth, ~90% earnings growth, an operating margin rise from 16% to 20%, and ROIC in the mid-teens; he raised the 2028 sales target by $3 billion to about $24 billion, aiming to nearly double company size over five years.

- Optical communications remains the primary investment focus, with long-term agreements (e.g., Meta) de-risking capacity expansion; scale-out demand is strong and Co-Packaged Optics scale-up is expected to inflect around 2028, with early CPO deployments ahead of that.

- Solar segment progress includes expanded polysilicon capacity via majority Hemlock stake, a new wafer plant ramping over coming quarters, and module production from the acquired business—on track to exceed $2.5 billion in sales by 2028.

- Specialty Materials saw a Gorilla Glass agreement with Apple to supply 100% of its U.S.-made glass from Kentucky, ensuring deeper collaboration on future device innovations and sustaining segment profitability.

- Capital allocation philosophy prioritizes organic, high-return opportunities—especially optics—while maintaining an investment-grade balance sheet, targeting free cash flow conversion of incremental growth, a dividend payout near 50%, and opportunistic share buybacks.

- Visa has shifted R&D from its core payments infrastructure to enriching edge-of-network services, supporting 1,000+ development squads and using AI tools to reduce prototype cycles from months to days.

- Consumer engagement remains strong, with transaction volume growth stable, average ticket size down 20% over 10 years and transaction counts tripling, reflecting higher transaction density.

- The company launched the Trusted Agent Protocol—an open standard for agent identification and tokenized payments—backed by Cloudflare, Akamai, Mastercard, American Express and now adopted by Stripe via Visa Intelligent Commerce.

- Value-added services revenue rose 28% YoY to $3.2 billion in Q1 FY2026, representing ~30% of total revenue, driven by under-penetrated issuer, acceptance, risk and analytics offerings.

- Stablecoin settlement run-rate grew from $2.5 billion (Aug 2025) to $4.6 billion (Q1 FY2026), with card-linked stablecoin programs in 40 countries and plans to expand to 100 via partners like Bridge and Stripe.

- Springboard growth plan upgraded: sales run-rate target raised by $3 billion to $11 billion through 2028, aiming for a ~$24 billion company and nearly doubling size over five years; operating margin improved from ~16% to 20% and ROIC to mid-teens.

- Expanding optical communications via long-term agreements (e.g., Meta LTA) to secure fiber volume and de-risk capital, with focus on scale-out data-center connectivity and preparation for scale-up/co-packaged optics by 2028 .

- Accelerating solar business: majority ownership of Hemlock polysilicon ramping capacity; newly commissioned wafer and module plants targeting >$2.5 billion in sales by 2028, with facilities reaching full efficiency over the next quarters.

- Capital allocation prioritizes high-ROIC organic investments—especially in optics—while maintaining an investment-grade balance sheet, a ~50% dividend payout ratio, and opportunistic share buybacks to sustain financial flexibility.

- Visa has shifted a greater share of R&D spend from core infrastructure to edge services, forming 1,000+ dev squads and leveraging AI to prototype new products in days rather than months.

- The company introduced the Visa Trusted Agent Protocol, an open standard for agent identity and tokenized payments in agentic commerce, backed by Cloudflare, Akamai, Mastercard, and American Express.

- Visa offers 130+ stablecoin-linked card programs across 40 countries, enabling consumers to use stablecoins via familiar card rails and planning to expand its partnership with Bridge to 100 countries by year-end.

- Stablecoin settlement volume on Visa’s network rose from an annualized $2.5 billion in August 2025 to $4.6 billion by the end of Q1 2026, driven by new regions, client onboarding, and increased usage.

- Executives expect agentic commerce to boost transaction density (average ticket size down 20% over 10 years, transactions tripled) and accelerate B2B payment growth (10% in Q1 2026), citing partnerships like Ramp for frictionless business-to-business payments.

- Corning has upgraded its Springboard growth plan, adding $3 billion to its 2028 sales outlook to reach approximately $24 billion, after having grown sales 40% and earnings 90% since the plan’s 2024 launch, and has achieved a 20% operating margin.

- The company is securing long-term optical communications agreements—most notably with Meta—and is investing to capture robust scale-out data center demand and prepare for future co-packaged optics deployments.

- Capital allocation prioritizes organic investments in fiber, cable, and connectivity capacity with a target >20% ROIC, backed by over $1 billion in annual R&D spend and a strong investment-grade balance sheet.

- In solar, Corning has ramped up polysilicon and wafer production, acquired a module business, and is on track for >$2.5 billion in solar sales by 2028 as facilities reach full efficiency.

- The specialty materials segment was bolstered by a U.S. manufacturing agreement with Apple to supply 100% of its Gorilla Glass from Kentucky, deepening their technology collaboration.

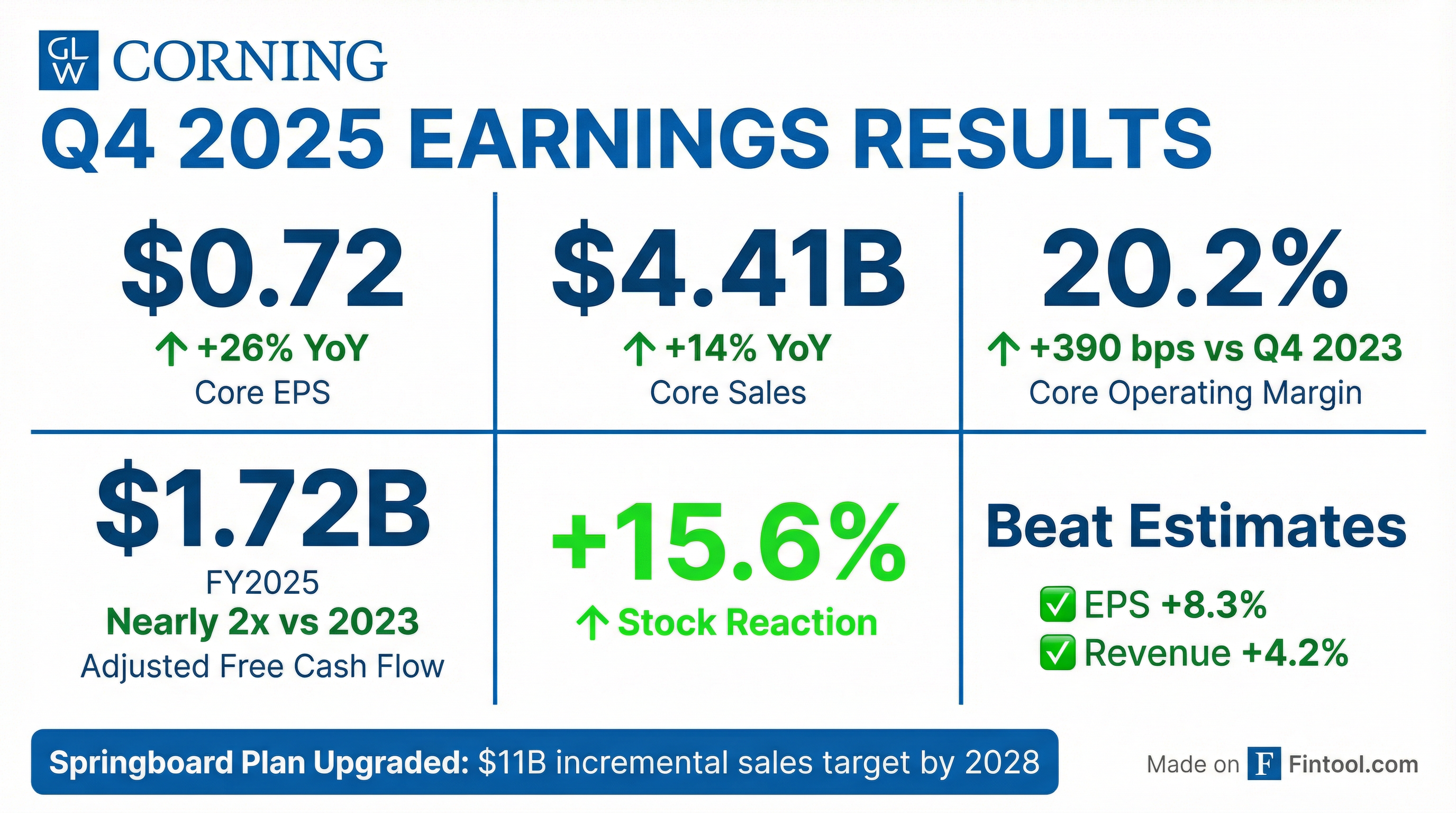

- Corning delivered Q4 sales of $4.41 billion (+14% YoY) and EPS of $0.72 (+26% YoY), with operating margin expanding 170 bps to 20.2% and ROIC rising to 14.2%.

- Full-year 2025 sales rose 13% to $16.4 billion, EPS grew 29% to $2.52, operating margin expanded 180 bps to 19.3%, and free cash flow nearly doubled to $1.72 billion.

- The company upgraded its Springboard plan, targeting $6.5 billion of incremental annualized sales by end-2026 (vs. $6 billion prior) and $11 billion by end-2028, with a high-confidence 2026 target of $5.75 billion.

- Q1 2026 guidance assumes ~15% sales growth to $4.2–4.3 billion, ~26% EPS growth to $0.66–0.70, and full-year capex of ~$1.7 billion, while continuing share buybacks.

- Announced a multi-year, up to $6 billion agreement with Meta for GenAI data-center fiber and connectivity, reinforcing domestic capacity expansions in North Carolina.

- Corning delivered 14% sales growth to $4.41 billion and 26% EPS growth to $0.72 in Q4; operating margin expanded 170 bps to 20.2% and ROIC rose to 14.2%.

- For full-year 2025, the company achieved double-digit sales growth, with EPS growing twice as fast as sales and free cash flow nearly doubling to $1.72 billion.

- 2026 guidance includes Q1 sales growth of ~15% to $4.2 billion–$4.3 billion, Q1 EPS of $0.66–$0.70, and full-year capex of about $1.7 billion; free cash flow is expected to increase.

- Springboard plan upgraded: internal incremental annualized sales targets raised to $6.5 billion by end-2026 (from $6 billion) and $11 billion by end-2028 (from $8 billion); high-confidence 2026 plan now $5.75 billion (from $4 billion).

- Capital allocation priorities include maintaining ≥20% operating margin, investing in organic growth with customer-shared funding, and returning excess cash via share buybacks (cumulative ~800 million shares repurchased), resumed in Q2 2024.

- Q4 2025 revenue grew 14% to $4.4 B, EPS rose 26% to $0.72, operating margin expanded to 20.2%, and free cash flow was $732 M; full-year sales were $16.4 B (+13%), EPS $2.52 (+29%), operating margin 19.3%, FCF $1.7 B

- Upgraded Springboard plan to add $11 B in incremental annualized sales by end-2028 (from $8 B) and $6.5 B by end-2026 (from $6 B); high-confidence 2026 target raised to $5.75 B (from $4 B)

- Q1 2026 guidance: expected ~15% sales growth to $4.2–4.3 B and ~26% EPS growth to $0.66–0.70, including a $0.03–0.05 drag from the solar ramp

- Capital allocation: plan for $1.7 B capital expenditures, maintain dividend, and focus excess cash on share buybacks—800 M shares repurchased over last decade, continuous buybacks since Q2 2024

- Optical Communications segment: Q4 sales $1.7 B (+24%), FY $6.3 B (+35%), driven by Gen AI product adoption; enterprise business +61% and hyperscale growth even stronger

- Upgraded Springboard plan alongside Q4 core sales of $4.41 billion and adjusted EPS of $0.72, both beating estimates

- Q4 core net income rose 26% to $624 million; GAAP net income was $540 million (EPS $0.62); gross margin 38.1%, operating margin 20.2%

- Transformation gains: core operating margin expanded 390 bps to 20.2%, core ROIC rose 540 bps to 14.2%, and adjusted free cash flow nearly doubled to $1.72 billion for 2025

- Provided Q1 2026 guidance of adjusted EPS $0.66–$0.70 and core sales $4.2–$4.3 billion, near consensus

Fintool News

In-depth analysis and coverage of CORNING INC /NY.

Quarterly earnings call transcripts for CORNING INC /NY.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more