Earnings summaries and quarterly performance for WEX.

Executive leadership at WEX.

Melissa Smith

Chief Executive Officer and President

Ann Drew

Chief Risk and Compliance Officer

Carlos Carriedo

Chief Operating Officer, Americas Payments & Mobility

Jagtar Narula

Chief Financial Officer

Jay Dearborn

Chief Operating Officer, International

Jennifer Kimball

Chief Accounting Officer

Karen Stroup

Chief Digital Officer

Robert Deshaies

Chief Operating Officer, Benefits

Sachin Dhawan

Chief Technology Officer

Sara Trickett

Chief Legal Officer, Interim Chief People Officer, and Corporate Secretary

Board of directors at WEX.

Aimee Cardwell

Director

Daniel Callahan

Director

David Foss

Director

Derrick Roman

Director

Jack VanWoerkom

Vice Chairman and Lead Director

James Groch

Director

James Neary

Director

Nancy Altobello

Director

Shikhar Ghosh

Director

Stephen Smith

Director

Susan Sobbott

Director

Research analysts who have asked questions during WEX earnings calls.

David Koning

Robert W. Baird & Co.

9 questions for WEX

Sanjay Sakhrani

Keefe, Bruyette & Woods (KBW)

9 questions for WEX

Mihir Bhatia

Bank of America

6 questions for WEX

Rayna Kumar

Oppenheimer & Co. Inc.

6 questions for WEX

Darrin Peller

Wolfe Research, LLC

5 questions for WEX

Ramsey El-Assal

Barclays

5 questions for WEX

Andrew Jeffrey

William Blair & Company

4 questions for WEX

Nate Svensson

Deutsche Bank

4 questions for WEX

Trevor Williams

Jefferies LLC

4 questions for WEX

Andrew Bauch

Wells Fargo & Company

3 questions for WEX

Dan Dolev

Mizuho Financial Group

2 questions for WEX

Michael Infante

Morgan Stanley

2 questions for WEX

Michael Rosenthal

Morgan Stanley

2 questions for WEX

Nate Sanson

Deutsche Bank

2 questions for WEX

Nik Cremo

UBS Group AG

2 questions for WEX

Nikolai Cremo

UBS

2 questions for WEX

Shray Gurtata

Barclays

2 questions for WEX

Tien-tsin Huang

JPMorgan Chase & Co.

2 questions for WEX

Christopher Svensson

Deutsche Bank AG

1 question for WEX

Daniel Krebs

Wolfe Research

1 question for WEX

John Davis

Raymond James Financial

1 question for WEX

Recent press releases and 8-K filings for WEX.

- WEX provided 2026 guidance of $2.7 billion - $2.76 billion in revenue and $17.25 - $17.85 in EPS, representing a midpoint of 5% revenue growth and 13% EPS growth (excluding macro factors).

- The company is heavily investing in AI, which led to a 50% increase in product innovation velocity in 2025 and currently sees 40% of its code written by AI.

- WEX generated $638 million in cash flow in 2025 and has returned $2 billion to shareholders since 2022, including $790 million last year, with a current focus on delevering to below 3% leverage.

- Growth is expected from the Mobility segment (50% of business), with BP rolling onto its platform in 2026, and the Benefits segment (targeting 5%-7% top-line growth) driven by AI-enabled products and account expansion.

- WEX reported $2.66 billion in revenue and $16.10 in adjusted net income per diluted share for the full year 2025.

- For the full year 2026, WEX projects revenue between $2,700 million and $2,760 million and adjusted net income per diluted share between $17.25 and $17.85.

- In 2025, WEX allocated $790.0 million to share repurchases and ended the year with a leverage ratio of 3.1x, within its target range of 2.5-3.5x.

- The company targets long-term organic revenue growth of 5-10% and adjusted earnings per share growth of 10-15%.

- WEX provided 2026 guidance on February 5th, projecting revenue between $2.7 billion and $2.76 billion and EPS between $17.25 and $17.85. The midpoint of this guidance, excluding macro factors, implies 5% revenue growth and 13% EPS growth.

- The company is heavily investing in Artificial Intelligence (AI), which led to a 50% increase in product innovation velocity in 2025 with 400 fewer product and technology staff. Currently, 40% of WEX's code is written by AI, enhancing product development, risk management, and operational efficiency.

- WEX generated $638 million in cash flow in 2025 and has returned $2 billion to shareholders since 2022, including $790 million in 2025 through share buybacks. The company is focused on deleveraging to below 3% from its current 3.1x leverage ratio before considering other capital uses.

- The Mobility segment (approximately 50% of the business) is expected to see 1%-3% organic growth in 2026, driven by the integration of BP onto its platform and increased customer acquisition efforts. The Benefits segment targets 5%-7% top-line growth, fueled by new product offerings and increasing account balances.

- WEX operates across three key markets: mobility (approximately 50% of its business), benefits, and corporate payments (approximately 20% of its business), focusing on payment intelligence and workflow solutions to simplify business operations.

- For 2026, WEX provided guidance of $2.7 billion-$2.76 billion in revenue and $17.25-$17.85 in EPS, which at the midpoint, implies 5% revenue growth and 13% EPS growth when excluding fuel prices, FX, and interest rates. The company views 2025 as an investment year and 2026 as a scaling year.

- WEX has made substantial investments in artificial intelligence (AI), with 40% of its code currently written by AI and a 50% increase in product innovation velocity in 2025 with over 400 fewer product and technology personnel, aiming for enhanced customer experience and lower operational costs.

- The company generated $638 million in cash flow in 2025 and has returned $2 billion to shareholders since 2022, including $790 million last year. WEX is focused on delevering from its current 3.1 times leverage to below 3%, with share buybacks expected to continue through 2026.

- Segment growth is driven by factors such as the BP partnership coming online in the second half of 2026 and increased customer acquisition in mobility, compelling product roadmaps and account growth in benefits, and continued spend volume growth in corporate payments, which grew 15% last quarter.

- Private-equity firm Thoma Bravo is moving to acquire WWEX Group and combine it with its shipping-software portfolio company Auctane.

- The combined business is expected to become one of the largest logistics and shipping-technology platforms, with media reports valuing the new company at up to $12 billion and placing WWEX's valuation at roughly $5 billion.

- WWEX reported approximately $5 billion in systemwide revenue in 2025, serves over 130,000 customers, and moves over 70 million shipments annually.

- The transaction is planned to close in the second quarter of 2026, subject to regulatory approvals, with existing WWEX investors retaining a significant minority stake.

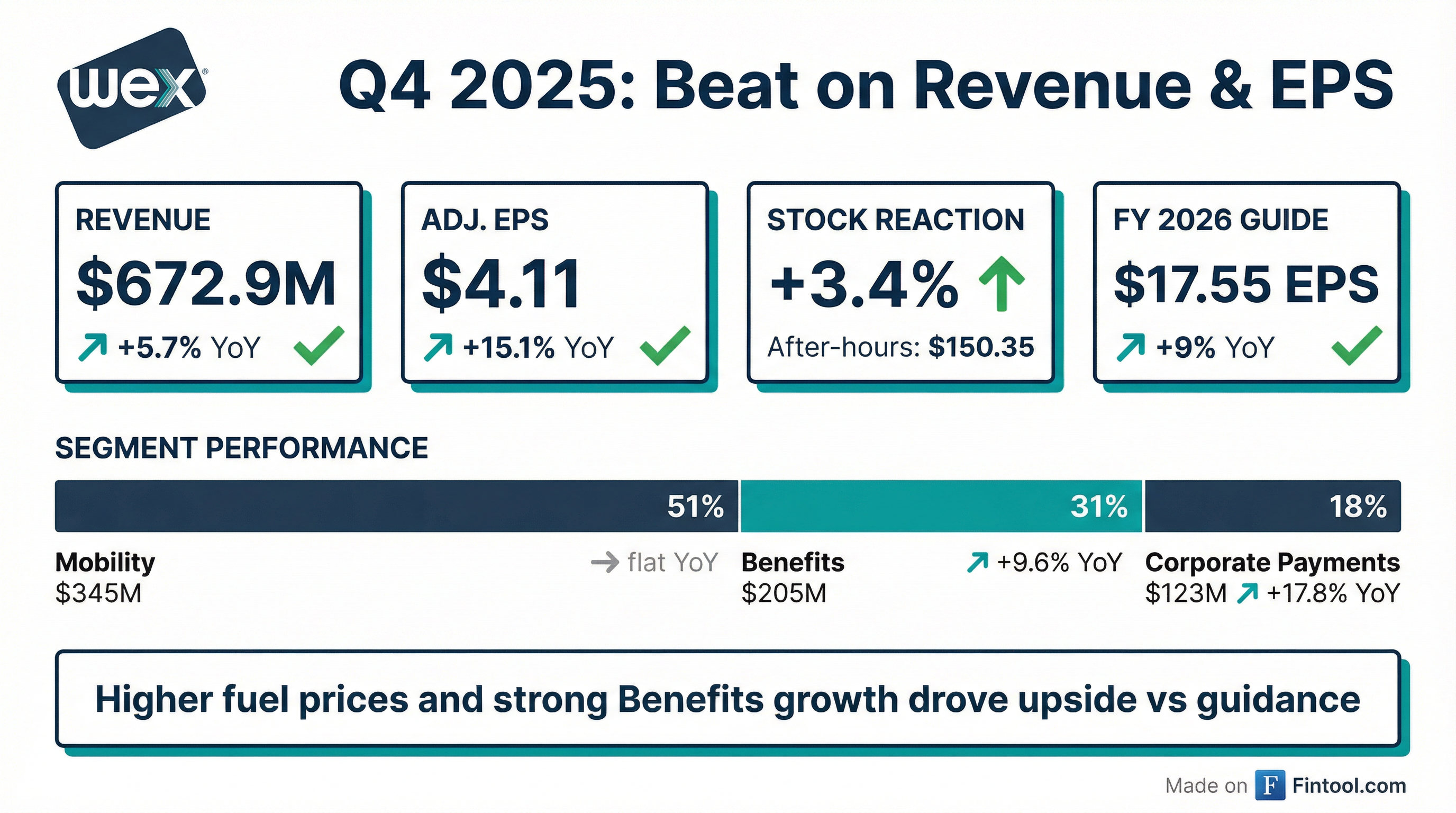

- WEX reported Q4 2025 revenue of $672.9 million, an increase of 5.7% year-over-year, and adjusted net income per diluted share of $4.11, up 15.1% year-over-year. For the full year 2025, revenue reached a record $2.66 billion, and adjusted net income per share was $16.10.

- The company provided Q1 2026 revenue guidance of $650 million-$670 million and adjusted EPS guidance of $3.80-$4.00. For full year 2026, WEX expects revenue between $2.70 billion and $2.76 billion and adjusted EPS between $17.25 and $17.85.

- WEX is transitioning from an investment phase to a scaling phase in 2026, with operating leverage expected to drive meaningful margin expansion over the medium term, supported by $50 million in cost savings actions.

- The company generated $638 million in adjusted free cash flow in 2025 and plans to prioritize debt reduction, aiming for a leverage ratio below 3x by Q2 or Q3 2026.

- WEX reported Q4 2025 total revenue of $672.9 million, an increase of 5.7% year-over-year.

- GAAP net income per diluted share for Q4 2025 rose 50.6% to $2.41, while adjusted net income per diluted share increased 15.1% to $4.11.

- Performance was driven by higher fuel prices and strong growth in the Benefits segment, with revenue up 9.6% to $204.9 million, and the Corporate Payments segment, which saw revenue increase 17.8% to $122.9 million.

- The company maintained a healthy financial position with $1.25 billion in available liquidity and a leverage ratio of 3.1x as of December 31, 2025.

- WEX issued Q1 2026 guidance for net revenue between $650 million and $670 million, and adjusted net income per diluted share between $3.80 and $4.00.

- WEX delivered strong Q4 2025 results with revenue of $672.9 million, an increase of 5.7% year-over-year, and adjusted net income per diluted share of $4.11, up 15.1% year-over-year. For the full year 2025, the company achieved record revenue of $2.66 billion and adjusted net income per share of $16.10.

- The company provided 2026 guidance, projecting full-year revenue between $2.70 billion and $2.76 billion and adjusted EPS between $17.25 and $17.85 per diluted share. This represents a midpoint revenue growth of 5% and EPS growth of 13%, excluding the impact of fuel prices, FX rates, and interest rates.

- WEX is transitioning from an investment phase to a scaling phase in 2026, anticipating operating leverage and meaningful margin expansion over the medium term, supported by $50 million in cost savings actions. However, the adjusted operating income margin is expected to be flat with 2025 due to a negative impact from lower fuel prices.

- The company continues to prioritize debt reduction, ending Q4 2025 with a leverage ratio of 3.1 times and expecting to achieve a ratio below 3 times in Q2 or Q3 2026. WEX also plans to continue share buybacks given its current trading multiple.

- WEX reported Q4 2025 revenue of $672.9 million, a 5.7% increase year-over-year, and Adjusted Net Income per diluted share of $4.11, up 15.1%. For the full year 2025, revenue reached $2.66 billion and Adjusted Net Income per share was $16.10.

- For Q1 2026, WEX expects revenue between $650-$670 million and adjusted net income EPS between $3.80-$4.00. The full year 2026 guidance projects revenue of $2.70-$2.76 billion and adjusted net income EPS of $17.25-$17.85.

- The company generated $638 million in adjusted free cash flow in 2025 and reduced its leverage ratio to 3.1 times by Q4 2025, with a goal to be below 3 times by Q2 or Q3 2026.

- WEX plans to shift from an investment to a scaling phase in 2026, with operating leverage driving meaningful margin expansion over the medium term, and has embedded $50 million of cost savings actions in its 2026 guidance.

- David Foss will assume the role of Vice Chair and Lead Independent Director effective at the 2026 annual meeting, as part of a multi-year board refreshment plan.

- WEX reported Q4 2025 revenue of $672.9 million, an increase of 5.7% compared to the prior year, and full year 2025 revenue of $2.66 billion, up 1.2%.

- For Q4 2025, GAAP net income was $2.41 per diluted share (up 50.6%) and adjusted net income was $4.11 per diluted share (up 15.1%), while full year 2025 adjusted net income per diluted share increased 5.4% to $16.10.

- The company provided Q1 2026 net revenue guidance of $650 million to $670 million and full year 2026 net revenue guidance of $2,700 million to $2,760 million.

- Q1 2026 adjusted net income per diluted share is projected to be between $3.80 and $4.00, with full year 2026 adjusted net income per diluted share expected to range from $17.25 to $17.85.

Quarterly earnings call transcripts for WEX.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more