Earnings summaries and quarterly performance for Schneider National.

Executive leadership at Schneider National.

Mark B. Rourke

President and Chief Executive Officer

Darrell G. Campbell

Executive Vice President, Chief Financial Officer

James S. Filter

Executive Vice President, Group President, Transportation & Logistics

Robert M. Reich

Executive Vice President, Chief Administrative Officer

Shaleen Devgun

Executive Vice President, Chief Innovation and Technology Officer

Board of directors at Schneider National.

James L. Welch

Chairman of the Board

James R. Giertz

Director

John A. Swainson

Director

Julie K. Streich

Director

Jyoti Chopra

Director

Kathleen M. Zimmerman

Director

Mary P. DePrey

Director

Robert M. Knight, Jr.

Director

Robert W. Grubbs

Director

Research analysts who have asked questions during Schneider National earnings calls.

Ken Hoexter

BofA Securities

6 questions for SNDR

Brian Ossenbeck

JPMorgan Chase & Co.

5 questions for SNDR

Jonathan Chappell

Evercore ISI

5 questions for SNDR

Ravi Shanker

Morgan Stanley

5 questions for SNDR

Christian Wetherbee

Wells Fargo

4 questions for SNDR

Ariel Rosa

Citigroup

3 questions for SNDR

Daniel Imbro

Stephens Inc.

3 questions for SNDR

J. Bruce Chan

Stifel

3 questions for SNDR

Jordan Alliger

Goldman Sachs

3 questions for SNDR

Tom Wadewitz

UBS Group

3 questions for SNDR

Andrew Cox

Stifel

2 questions for SNDR

Bascome Majors

Susquehanna Financial Group

2 questions for SNDR

Chris Wetherbee

Wells Fargo & Company

2 questions for SNDR

David Hicks

Raymond James

2 questions for SNDR

Jason Seidl

TD Cowen

2 questions for SNDR

Scott Group

Wolfe Research

2 questions for SNDR

Thomas Wadewitz

UBS

2 questions for SNDR

Ari Rosa

Citigroup Inc.

1 question for SNDR

Dan Moore

B. Riley Securities

1 question for SNDR

Joe Enderlin

Stephens

1 question for SNDR

Ravi Shankar

Morgan Stanley

1 question for SNDR

Recent press releases and 8-K filings for SNDR.

- Schneider National provided an adjusted EPS outlook for 2026 of $0.70-$1.00, with the bottom end reflecting persistent Q4 2025 conditions and the high end requiring macro demand inflection.

- The company is observing a more constructive market environment with attractive spot pricing, particularly in the Midwestern and Northeastern geographies, driven by regulatory actions that are steadily reducing capacity.

- Management is focused on margin recovery and has a $40 million cost and productivity savings target for 2026, doubling the 2025 target.

- Schneider aims to return to long-term operating margin targets of 12%-16% for Truckload, 10%-14% for Intermodal, and 3%-5% for Logistics, expressing confidence in achieving these with a normal market cycle.

- The company's truckload business is 70% Dedicated and 30% Network, with a focus on asset productivity and earnings growth over just truck growth, particularly in Intermodal where earnings can grow 20%-25% without adding trailing equipment.

- Schneider National observes a more constructive market environment for pricing and commitments, with supply-demand equilibrium closer than expected due to regulatory actions causing capacity attrition, particularly in the for-hire space. Consumer demand has been steady and resilient, and addressed inventory levels could catalyze a replenishment cycle.

- The company's ongoing cost-out initiatives, which began before 2025, led to a 7% reduction in non-driver headcount in 2025 and focus on structural changes and third-party costs, aiming for leverage during growth.

- Schneider has reconstructed its truckload business to be 70% dedicated configuration and 30% network, aiming for more durable earnings streams. The company is also focused on technology investments, including AI, to lower its cost to serve and improve efficiency.

- Schneider emphasizes its multimodal capabilities, with $2.5 billion in truck, over $1 billion in intermodal, and $1 billion in logistics, allowing it to offer diverse solutions beyond traditional trucking.

- Schneider National projects 2026 adjusted EPS in the range of $0.70 to $1.00, with the lower end reflecting a conservative view based on conditions from the second half of 2025.

- The company aims for $40 million in cost and productivity savings for 2026, following a similar target in 2025, with most of these savings anticipated in the second half of the year.

- Current operating margins for truckload (3.8%), intermodal (6.7%), and logistics (0.8%) are below long-term targets of 12%-16%, 10%-14%, and 3%-5% respectively, with a strategic focus on margin recovery.

- Growth initiatives prioritize earnings growth over truck growth in dedicated, and intermodal is expected to achieve 20%-25% earnings growth without adding trailing equipment, with 2026 capital expenditures primarily for fleet replacement.

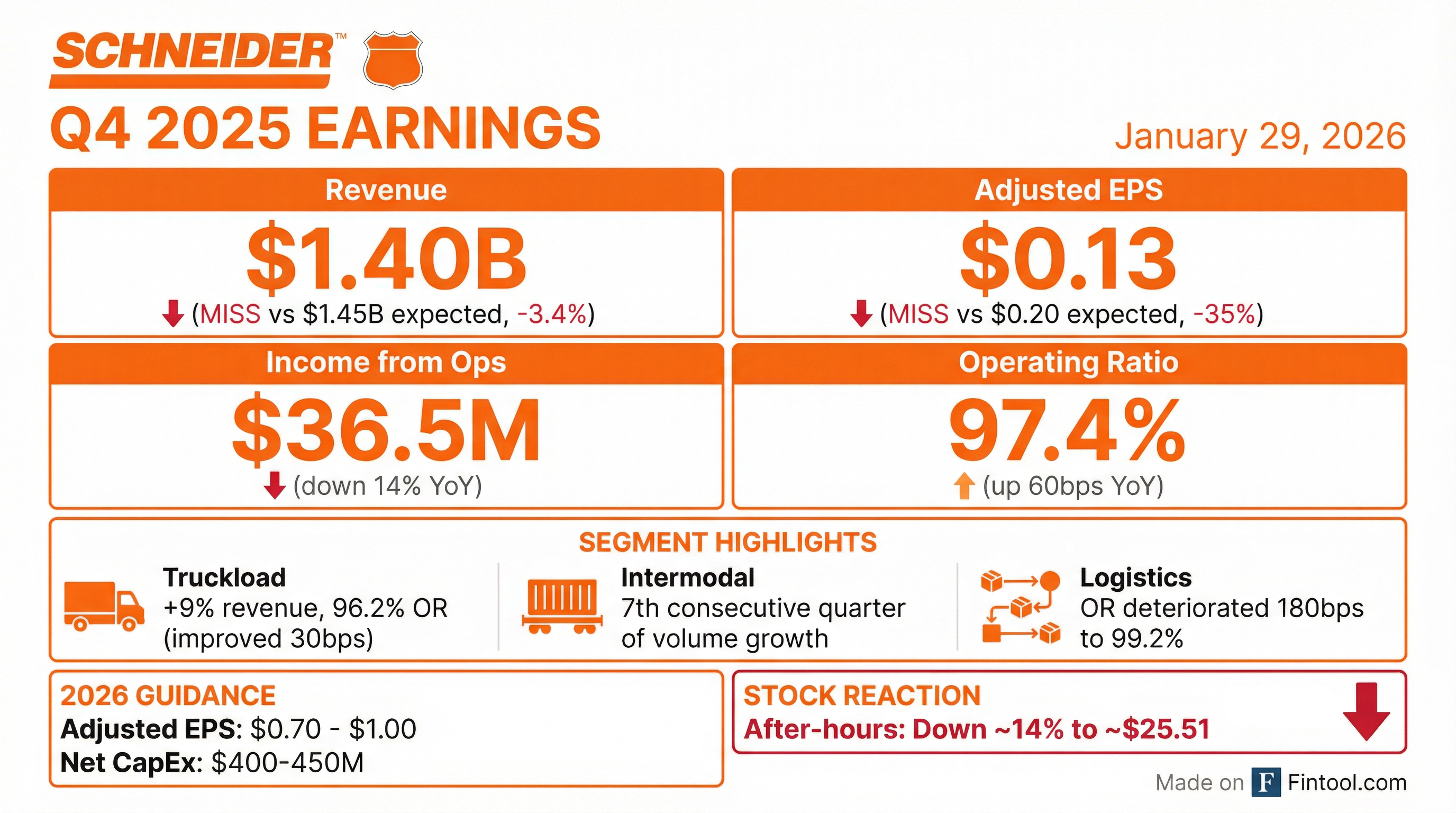

- Schneider National reported Q4 2025 Truckload revenue (excluding fuel surcharge) of $610 million, up 9% year-over-year, with operating income of $23 million, up 16%. Intermodal operating income increased 5% to $18 million, while Logistics income from operations decreased to $3 million. The company achieved its targeted $40 million in cost savings for 2025.

- For the full year 2026, the company issued adjusted earnings per share guidance of $0.70-$1.00. They anticipate an additional $40 million in cost savings for 2026 and project net CapEx between $400 million-$450 million, primarily for fleet replacement.

- As of December 31, 2025, net debt leverage improved to 0.3 times. The Board of Directors authorized a new $150 million stock repurchase program over the next three years.

- Q4 2025 was impacted by sluggish demand, unplanned auto production shutdowns, and elevated healthcare costs. Effective July 1, 2026, Mark Rourke will transition to Executive Chairman, and Jim Filter will become President and CEO.

- For Q4 2025, Schneider National reported revenues (excluding fuel surcharge) of $1.3 billion, a 4% increase year-over-year, with adjusted income from operations at $38 million (a 15% decline), and adjusted diluted earnings per share of $0.13.

- The company provided full-year 2026 adjusted EPS guidance of $0.70-$1 and expects net CapEx to be in the range of $400 million-$450 million. They also anticipate an additional $40 million in cost savings for 2026.

- Net debt leverage improved to 0.3x by the end of Q4 2025, and the Board authorized a new $150 million stock repurchase program over the next three years. Mark Rourke will transition to Executive Chairman, and Jim Filter will be appointed President and CEO, effective July 1, 2026.

- Schneider reported Q4 2025 revenues, excluding fuel surcharge, of $1.3 billion, an increase of 4% year-over-year, with adjusted income from operations at $38 million, a 15% decline, and adjusted diluted earnings per share of $0.13.

- The company achieved $40 million in cost savings in 2025 and expects to deliver an additional $40 million in cost savings in 2026.

- As of December 31, 2025, Schneider's net debt leverage was 0.3 times, and its Board of Directors authorized a new $150 million stock repurchase program over the next three years, effective January 26, 2026.

- Market conditions in Q4 2025 were more challenging than anticipated, with sluggish demand and unplanned auto production shutdowns, but the company expects capacity attrition to continue into 2026 due to regulatory actions.

- Schneider reported Q4 2025 operating revenues of $1,400 million and adjusted diluted earnings per share of $0.13, with adjusted income from operations declining 15% year-over-year.

- For full-year 2026, the company issued adjusted diluted earnings per share guidance of $0.70 to $1.00 and net capital expenditure guidance of $400 million to $450 million.

- In January 2026, Schneider announced a new $150 million, 3-year share repurchase program and declared a quarterly cash dividend of $0.10 per share, a 5% increase.

- The company achieved $40 million in cost savings in 2025 and identified an additional $40 million for 2026, maintaining a net debt leverage of 0.3x at quarter-end.

- Schneider National, Inc. reported operating revenues of $1.4 billion for the fourth quarter of 2025, an increase from $1.3 billion in the same period of 2024. However, income from operations decreased to $36.5 million from $42.4 million, and diluted earnings per share were $0.13, down from $0.18 in Q4 2024.

- The company provided full year 2026 Adjusted Diluted Earnings per Share guidance of $0.70 - $1.00 and Net Capital Expenditures guidance of $400 - $450 million.

- Management attributed the Q4 results falling short to softer than expected market conditions beginning in November, particularly for volume, and spiking third-party carrier capacity costs. The company is focusing on its cost savings program, Intermodal Fast Track service, Dedicated start-up activity, and Network earnings improvement efforts.

- In January 2026, the Board of Directors authorized a new $150.0 million stock repurchase program, replacing the existing one, and declared a $0.10 dividend payable in April 2026.

- Schneider National, Inc. reported operating revenues of $1.4 billion and diluted earnings per share of $0.13 for the fourth quarter of 2025, with full year 2025 operating revenues reaching $5,674.3 million and diluted earnings per share at $0.59.

- The company provided full year 2026 Adjusted Diluted Earnings per Share guidance of $0.70 - $1.00 and Net Capital Expenditures guidance of $400 - $450 million.

- Fourth quarter results were negatively impacted by softer than expected market conditions, a truncated peak season, spiking third-party carrier capacity costs, and unplanned auto production shutdowns.

- The Board of Directors authorized a new $150.0 million stock repurchase program in January 2026, replacing the existing program, and declared a $0.10 dividend payable in April 2026.

- Schneider National, Inc. (SNDR) declared a quarterly cash dividend of $0.10 per share on its Class A and Class B common stock, representing a 5% increase over the previous quarterly dividend of $0.095 per share.

- The dividend is payable to shareholders of record as of March 13, 2026, and is expected to be paid on April 8, 2026.

- The Board of Directors approved a new stock repurchase program, effective immediately, authorizing the acquisition of up to $150 million of the Company’s outstanding Class A and/or Class B common stock over the next three years.

- This new program supersedes and replaces a prior $150 million stock repurchase authorization, under which the Company repurchased 4.4 million shares for a total of $110.1 million.

Fintool News

In-depth analysis and coverage of Schneider National.

Quarterly earnings call transcripts for Schneider National.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more